As participants and observers in transactions, the pending acquisition of Spirit Airlines, Inc. (NYSE: SAVE) by JetBlue Airways Corporation (NASDAQGS: JBLU) offers a lot of fodder for us to comment on. In this post, we look at the fairness opinions delivered by Morgan Stanley and Barclays to the Spirit board before approving the deal and then ask a key transaction-related question.

On July 28, 2022, Spirit agreed to be acquired by JetBlue for cash consideration of $33.50 per share, or $3.8 billion. Inclusive of net debt, the transaction at announcement had an enterprise value of $7.6 billion. Deal multiples included 25.5x analysts’ consensus EPS for the next 12 months and 12.3x NTM EBITDA.

The deal value excluding ticking payments that could push the total consideration to $34.15 per share, represented a 38% premium to Spirit’s closing price on July 27 of $24.30 per share; however, the announcement was not a surprise because Spirit had been in play since February 5 when the company agreed to be acquired by Frontier Group Holding, Inc. (NASDAQGS: ULCC) for 1.93 Frontier shares and $2.13 per share of cash, which was then valued at $25.83 per share.

JetBlue subsequently made an unsolicited cash offer on March 29 (disclosed on April 5) of $33.00 per share that was rejected on May 2. JetBlue then commenced a $30.00 per share tender on May 16, noting the price was less than the $33.00 per share offer because of the board’s “unwillingness to negotiate in good faith with us.”

Ultimately, the Frontier deal was terminated on July 27, and Spirit then entered into an agreement with JetBlue that provided for the following:

The proxy statement dated September 12 enumerated the reasons the Spirit board approved the merger agreement, including the fairness opinions that opined the consideration to be received by shareholders was fair from a financial point of view to the shareholders. Interestingly, both banks were retained by Spirit in late 2019 to assist in a review of strategic options that was interrupted by COVID.

A fairness opinion provides an analysis of the financial aspects of a proposed transaction from the point of view of one or more parties to the transaction, usually expressing an opinion about the consideration though sometimes the transaction itself. Ideally, the opinion is provided by an independent advisor that does not stand to receive a success fee, especially when the transaction is a close call or involves real or perceived conflicts. In the case of the JetBlue-Spirit transaction, both Spirit advisors will receive much larger contingent fees if the transaction is consummated compared to the fixed fee fairness opinions.[1]

Let’s look at a high-level comparison of each bank’s analysis, some of which were explicitly included in the fairness analyses and some of which were presented for reference only. (A link to the proxy statement can be found here.)

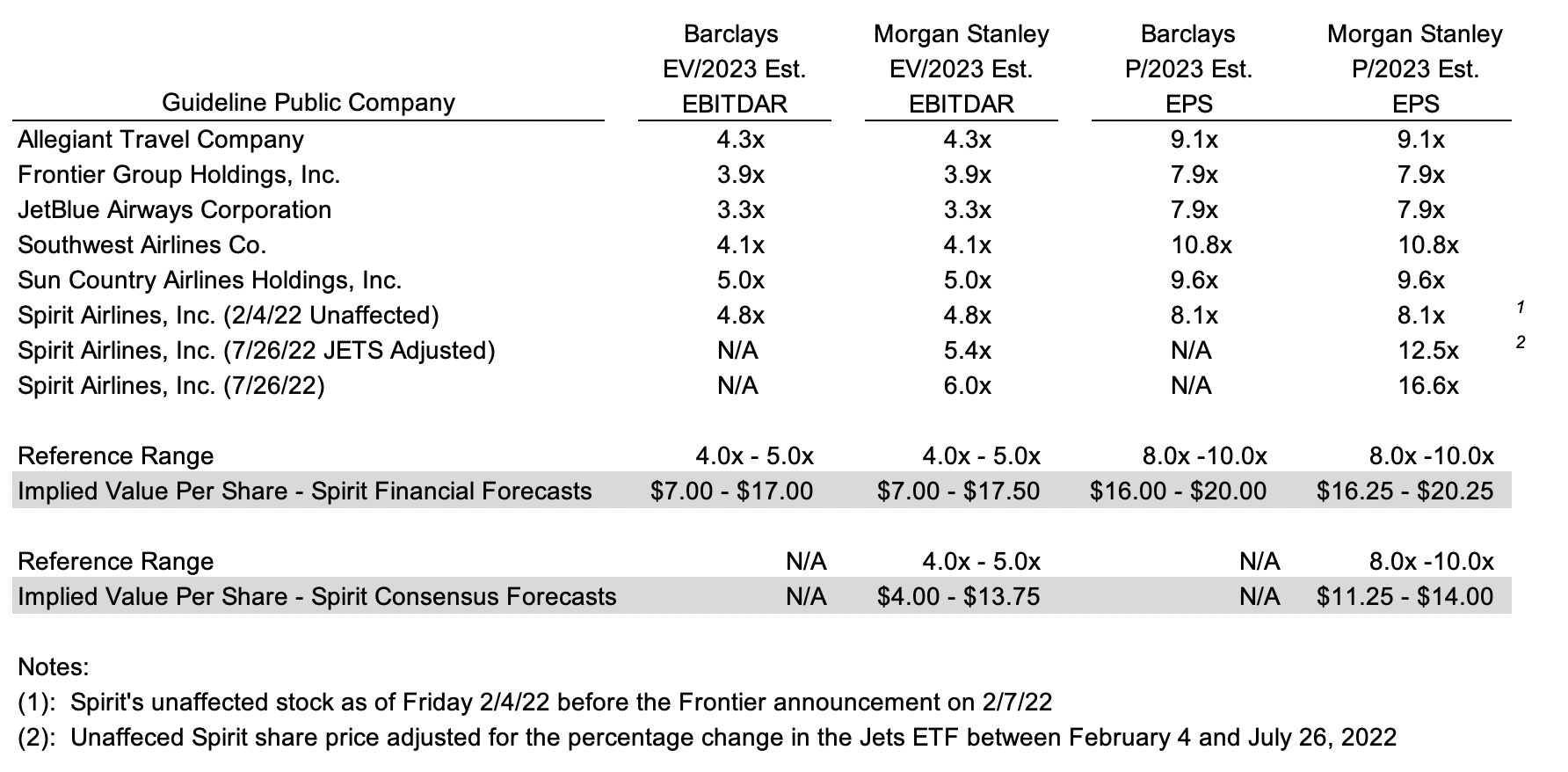

Barclays and Morgan Stanley reviewed and compared specific financial and operating data relating to Spirit with selected GPCs deemed comparable to Spirit. The following table compares the selected GPCs, the then-current multiples, the relevant multiple range, and indicated range of value for Spirit as calculated by each bank.

Click here to expand the image above

Both banks relied upon management’s forecast for net income and EBITDAR; however, Morgan Stanley also considered the Street’s consensus forecast for 2023. Spirit is included in the comp group to develop the applicable multiples with both banks relying upon pricing in early February immediately before the Frontier deal was announced; however, Morgan Stanley included alternate multiples based upon Spirit’s price as of July 26 and as of July 26 based upon the change in the industry ETF (JETS) from February 4. Nonetheless, the indicated values each developed based upon management’s forecast were the same.

The opinions did not include guideline transactions, presumably because there is limited M&A data involving U.S. carriers. The most recent significant acquisitions include Northwest Airlines and Continental Airlines in 2008, AirTran Holdings in 2010, and Virgin America in 2016. Nonetheless, we find it odd that a GT analysis was not addressed in the proxy.

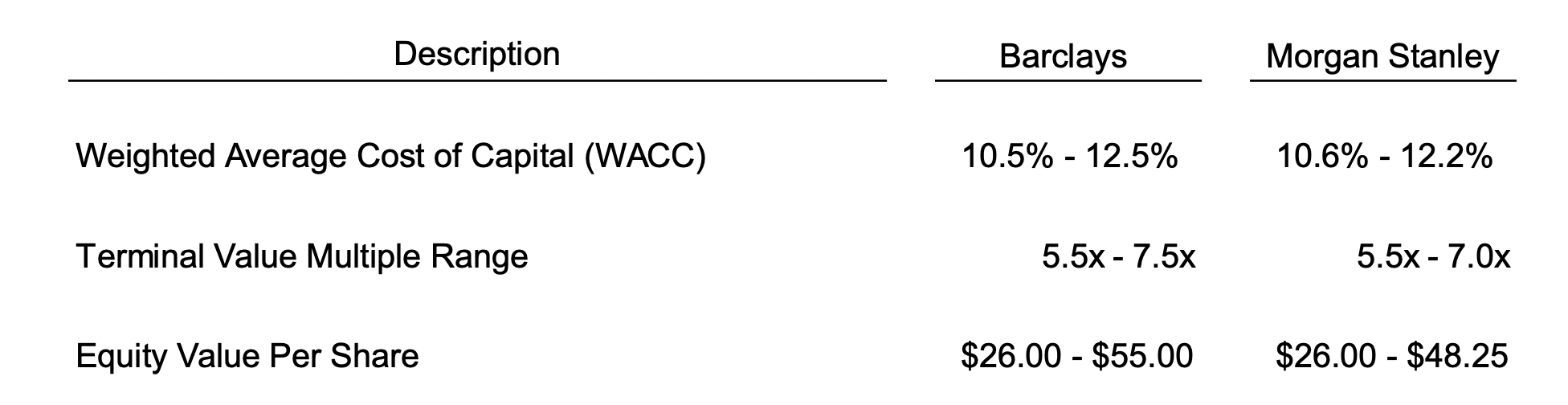

Both banks included a DCF analysis, a valuation method that is standard in virtually all valuation analyses. The gist of the analysis reflects the discounting of unlevered cash flows over a discrete period (2H22-2026) and the projected debt-free value of the company at the end of the projection period to present values based upon the weighted average cost of capital. Net debt is then subtracted to derive the indicated equity value.

Morgan Stanley but not Barclays derived indicated ranges of value per share by discounting management’s forecasted 2025 EBITDAR and EPS to present values based upon a 12.9% equity discount rate. If Spirit paid common dividends, the present value of the dividends through 2025 presumably would have been included, too. The analysis is similar to the DCF method except that cash flows are viewed from the perspective of what is received by shareholders compared to enterprise-level cash flows in the DCF analysis. Morgan Stanley derived a range of $24 to $43 per share based upon 5.0x to 6.5x EBITDAR and $39 to $47 per share based upon 9.0x to 11.0x forecasted 2025 EPS.

Both banks reviewed the 52-week trading history for Spirit for the period ended July 26, 2022 ($16-$29 per share) and in the case of Morgan Stanley for the 52 week period ended February 4, 2022 ($20-$40 per share). Although seemingly an important consideration for the fairness analyses, neither bank’s proxy write-up discussed the deal price premium relative to Spirit’s recent trading on a stand-alone basis or compared to M&A involving publicly traded midcap companies. The proxy did note that the board considered the premium in approving the merger agreement, however.

Both banks reviewed sell-side analysts’ one-year price targets ($24-$36 per share). Morgan Stanley discounted the price targets to a present value range of $21 to $32 per share using a discount rate of 12.9%, though the analysis was presented only for reference.

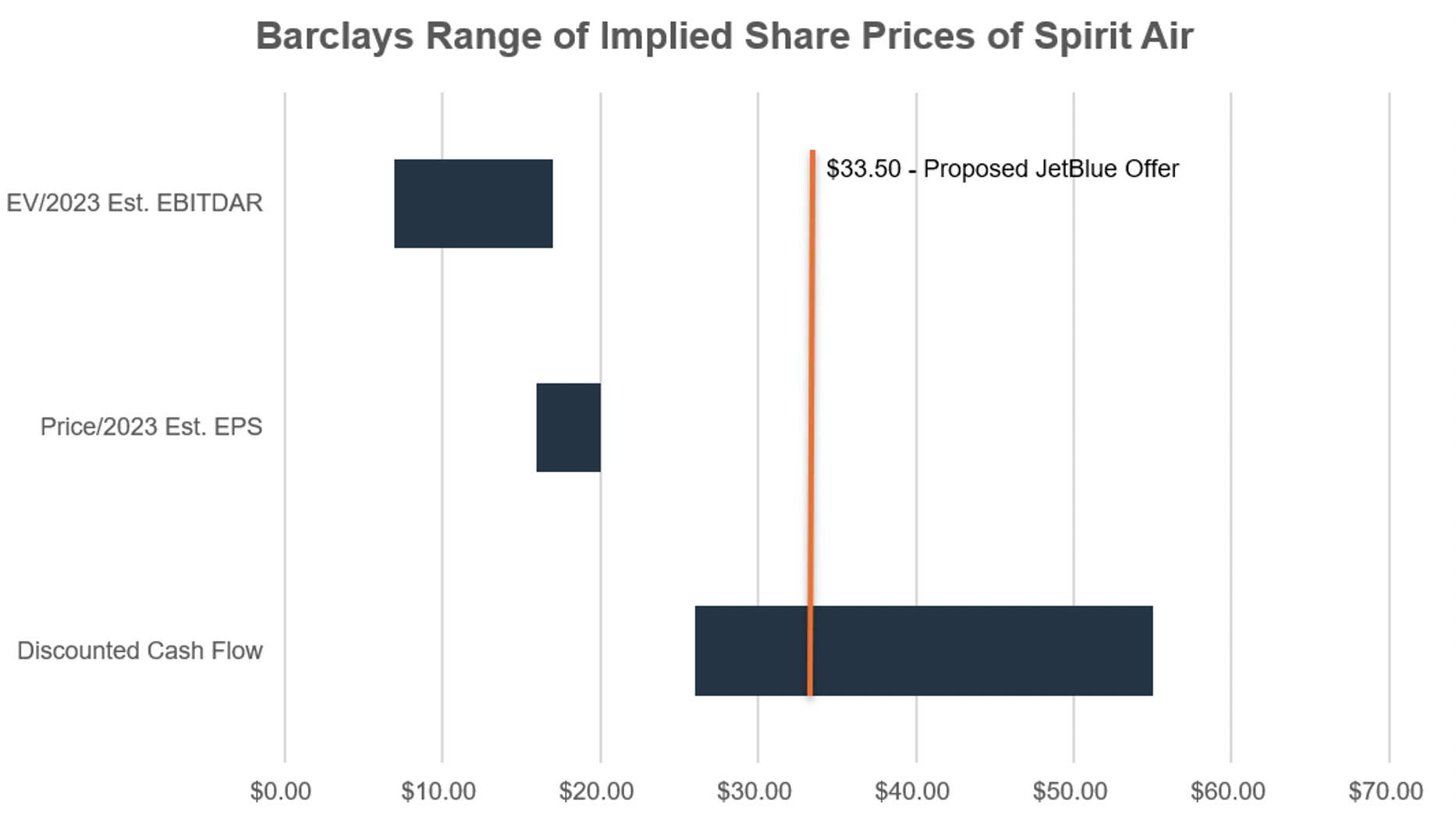

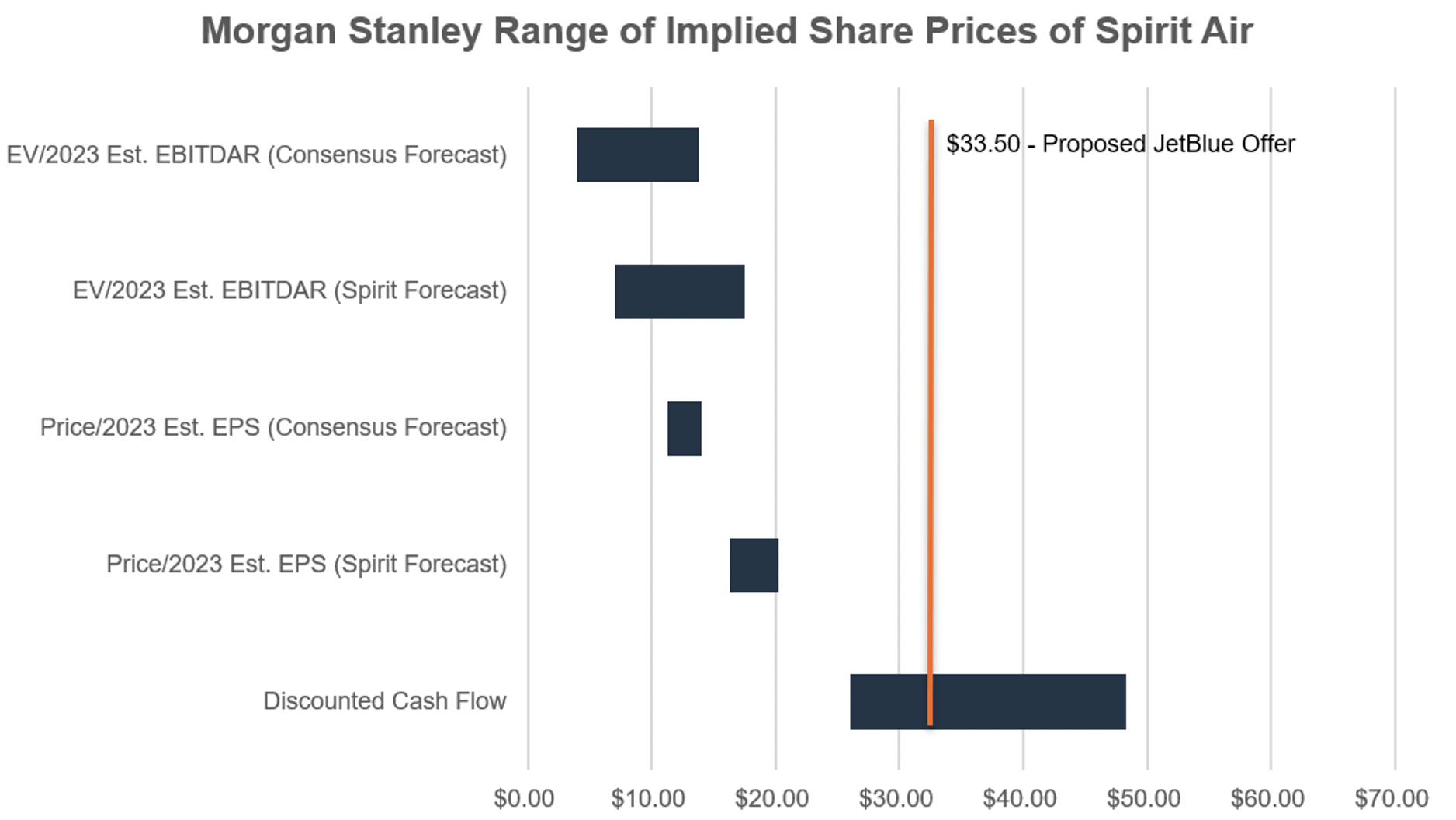

Both banks opined that, from a financial point of view, the consideration to be received by the stockholders of Spirit in the proposed transaction is fair to such stockholders. As can be seen in the graph below, the $33.50 share price falls within the range of values determined by both banks and decidedly above trading-based indications of value vs management’s forecast as reflected in the DCF valuations.

Given the price and terms of the JetBlue deal, rendering the fairness opinions appears to have been a straightforward exercise; however, one deal point a board must always consider is the ability of a buyer to close. This begs the question: Can JetBlue close the deal?

The market’s answer to the question is “no” given the deep discount Spirit trades to the acquisition price net of the approval payment. The deep discount reflects the growing likelihood that the U.S. Department of Justice will sue to block the deal because it would eliminate another low-cost carrier and position JetBlue-Spirit as the USA’s fifth-largest airline behind American Airlines, Delta Air Lines, Southwest Airlines, and United Airlines.

Among the factors the board considered that weighed against approving the deal was the risk that regulators would block the deal. These concerns were voiced by Frontier and some investors when JetBlue made its unsolicited offer nearly a year ago, but the board approved the transaction nonetheless, perhaps figuring JetBlue offered downside payments and that Frontier would still be an option if Washington nixed the JetBlue transaction.

And for what it is worth, the terminated Frontier deal would be valued around $23 per share, with its shares trading near $11 per share as of February 21.

Click here to expand the image above

Timothy R. Lee, ASA is the firm’s Managing Director of Corporate Valuation services and is a member of the firm’s board of directors. He provides litigation support services in cases involving economic damages, business valuation, dissenting shareholder rights, marital dissolution, and tax matters. Tim also provides valuation and corporate advisory services for purposes including mergers and acquisitions, employee stock ownership plans, profit sharing plans, trust & estate planning and compliance matters, corporate planning, and reorganizations.

Timothy Lee: As a “late” starter in financial services, I sought a path that would leverage years of practical experience gained from real world selling and managing in my teens and 20s. Business valuation has exposed me to a great diversity of business models and allowed me to learn from the successes and challenges of our clients.

Over the years, the core valuation discipline bridged into a multi-line financial advisory practice that places me in a position to assist clients facing both difficult and opportunistic events in the lifecycle of business ownership. For me, the bet on valuation and the fortitude of nearly 30 years of financial and industry breadth has placed me and my Mercer Capital colleagues in the enviable position of offering services with uncompromising credibility and with broad ranging experience well beyond a pure-play valuation shop.

Timothy Lee: Mercer Capital offers services across three broadly defined groupings: 1) valuation for tax, financial reporting, and other compliance and corporate finance purposes, 2) dispute resolution services ranging from unmatched buy-sell functionality to expert witness services for corporate and personal litigation matters, and 3) buy- and sell-side transaction advisory services primarily covering the middle-market M&A space and including large business concerns in numerous financial and non-financial industry verticals.

My personal practice has become more focused on the diverse needs of larger private companies whose regular needs require all three service buckets in real time and where reconciling these needs is essential for ownership success and strategic execution. Organizationally and personally, we are focused on the forest of client needs, which over time have become more business and industry centered while maintaining our legacy leadership in business valuation services.

Timothy Lee: Mercer Capital has worked diligently to parlay Chris Mercer’s longstanding success in significant litigation matters into a diverse dispute resolution practice with growing depth regarding industry coverage, legal setting, and dispute scenario. Today, we have several litigation-focused senior professionals who handle everything from business-heavy marital dissolution to corporate damages and fair value matters across the country.

Like most senior professionals at Mercer Capital, my litigation involvements are generally allied to certain industries and/or are related to certain dispute scenarios. For me, industry depth is broad ranging and particularly deep in numerous areas: construction contracting, trades, and building materials; food & beverage ranging from multi-unit franchise models to alcoholic beverage distribution; equipment dealership industries including earth-moving, agricultural, and material handling networks; manufacturing industries in metal fabrication and processing; vertically integrated agricultural concerns; real estate, hospitality, and hotels; specialty chemicals; professional practices; warehousing and merchant wholesale distribution models; transportation and logistics. I also have significant experience assisting clients in buy-sell design and dispute matters offering a functional path toward collaborative resolution.

Timothy Lee: Valuation perspective and financial market comprehension are lacking among a great many business owners, boards, and management teams. Relegating valuations to critical (often stressful) events as opposed to maintaining a programmatic discipline is very much like the saying: failing to prepare is preparing to fail. Self-serving as it may sound, I see basic business valuation as an elemental and regular need of business owners.

Businesses have employees dedicated to daily cash management, inventory control, and capital investment; but owners and boards rarely seek the all-important measurement of business value. Harsh as it sounds – that is preparation to fail and an abdication of wealth accountability. Understanding business value and how it changes in response to industry, market, and organic forces is what we help business owners understand. That is the essence of the service we provide.

Timothy Lee: Well, if I am limited to just one thing, I’d have to say the excitement is one of living up to the incredible trust and responsibility of informing clients with meaningful and actionable financial information. The derivatives (now I’m cheating) of that one thing are the countless benefits I get from interacting with clients and colleagues to do meaningful work.

We recall discussions in early 2022 with clients regarding their outlook for 2022 – three 25 basis point Fed rate increases, a “more normal” operating environment following the pandemic afflicted 2020 and 2021, and stable credit quality. The latter of those three items held true, but 2022 was anything but normal. Instead of three 25 basis point rate increases, the Fed delivered seven totaling 425 basis points. The bull market was routed for both equities and, most exceptionally, bonds.

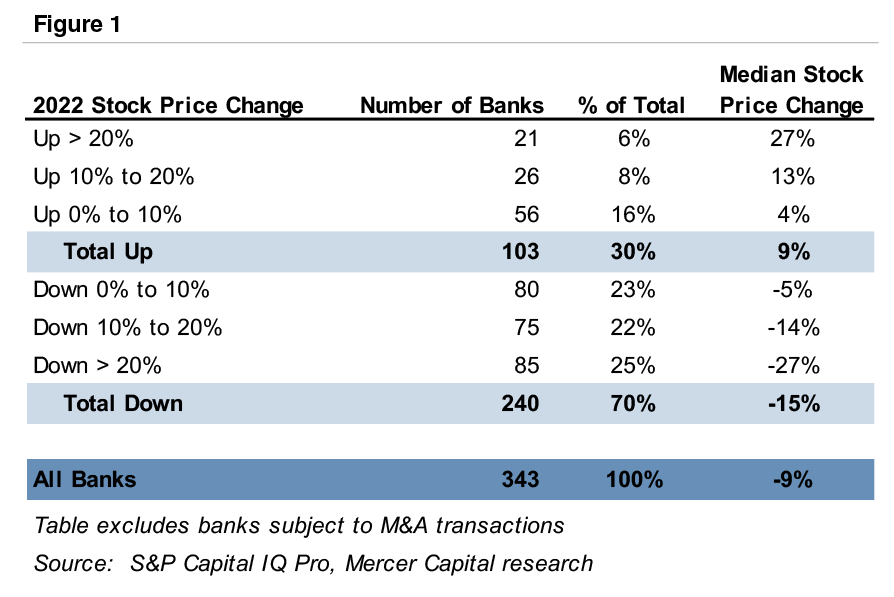

Given this backdrop, publicly-traded banks did comparatively well. The median stock price change among the 343 banks and thrifts traded on the NASDAQ and NYSE was negative 9% in 2022, relative to negative 19% for the S&P 500 and negative 33% for the NASDAQ. Further, there was more dispersion in performance during 2022.

In 2020, only 13% of publicly-traded banks reported a rising stock price during the year, whereas in 2021 only 5% of banks reported a falling stock price from year-end 2020 to 2021. That is, banks generally moved in tandem—down in 2020 and up in 2021. While not evenly balanced, 30% of banks reported a positive year-over-year stock price change in 2022 (see Figure 1). We believe this positive performance for quite a few banks in 2022 was masked by the downbeat market sentiment and warrants further investigation.

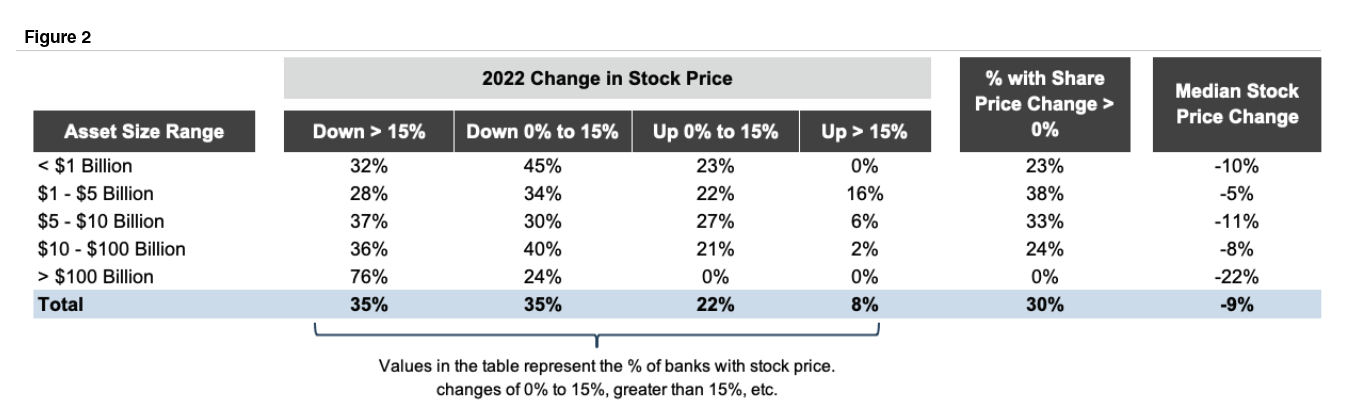

Figure 2 distinguishes shares price changes in 2022 by asset size range. The largest banks, with assets exceeding $100 billion, performed the worst in 2022, with no banks reporting share price appreciation and a median stock price decline of 22%. Smaller banks performed better, led by banks with assets between $1 and $5 billion. This stratum reported a median share price decline of only 5%, with 38% of the banks experiencing positive share price appreciation in 2022.

Click here to expand the image above

While market performance remains a function of the market’s ever evolving view of a particular bank’s earning power, growth outlook, and risk attributes, we explore in this article some of the factors influencing the better and weaker performing banks in 2022.

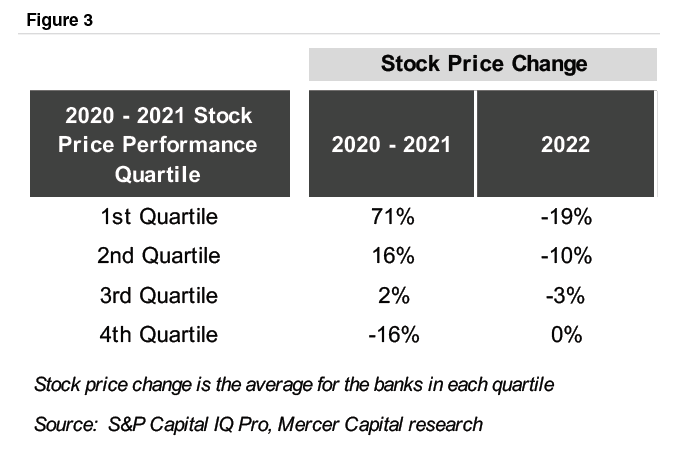

One of the best predictors of share price appreciation in 2022 was, in fact, performance from year-end 2019 to year-end 2021. As indicated in Figure 3, banks with the strongest price appreciation during 2020 and 2021 performed the worst in 2022, while those banks that most lagged the market in 2020 and 2021 outperformed in 2022.

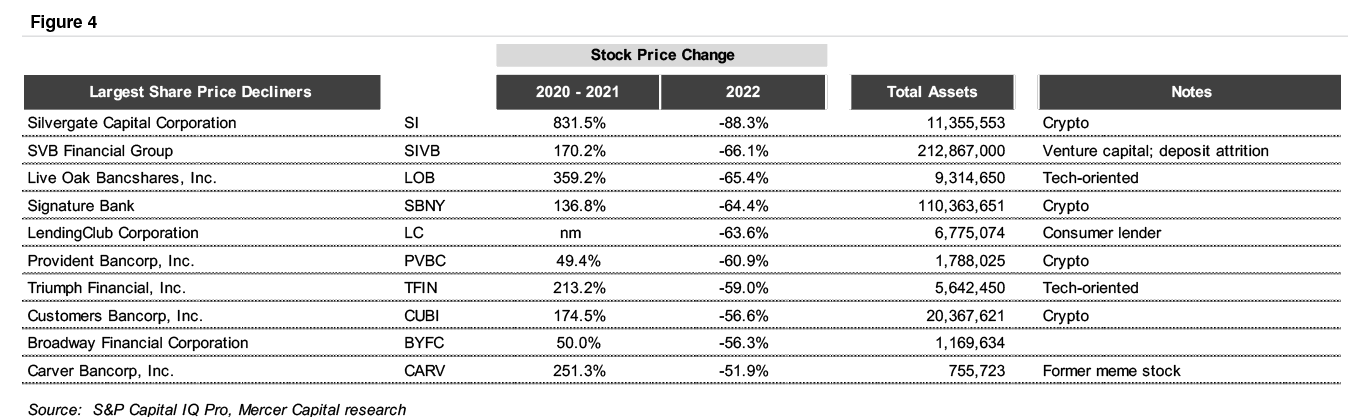

Some of the market leaders in 2020 and 2021 crashed out of favor in 2022, such as those embracing crypto or positioning themselves as technology leaders rather than stodgy, traditional banks. Figure 4 presents the ten banks with the largest negative returns in 2022.

Click here to expand the image above

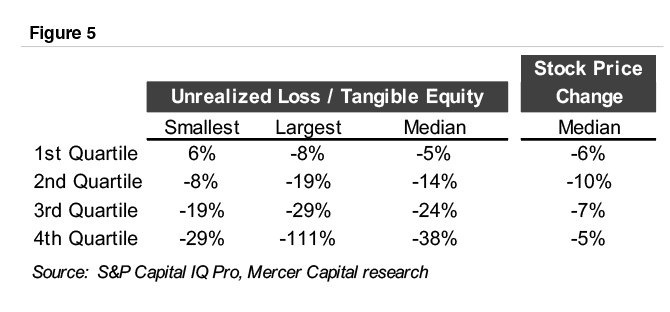

The most common question we received over the last twelve months was, “what is the effect of the unrealized securities portfolio loss on share value?” While there are possibly extenuating circumstances for some banks (see, e.g., Silvergate Capital Corp. in Figure 4), our general guidance is that the market emphasizes forward-looking earning power, not the magnitude of the unrealized loss.

Figure 5 correlates stock performance in 2022 with the magnitude of the unrealized securities portfolio loss.1 For example, banks in the first quartile had a median unrealized loss of 5% of equity.2 These banks experienced a median stock price change of negative 6%. Meanwhile, banks with the largest unrealized losses—ranging from 29% to 111% of tangible equity—reported a median stock price change of negative 5%. A more robust statistical analysis indicates a similar result; that is, virtually no relationship between the size of a bank’s unrealized securities portfolio loss and market performance in 2022.

Our view is that the unrealized loss on securities should be evaluated in the context of the entire balance sheet. We would be more concerned, from a valuation standpoint, when a large unrealized loss is coupled with a heavier exposure to fixed rate loans, particularly if the bank is facing pressure on deposit rates.

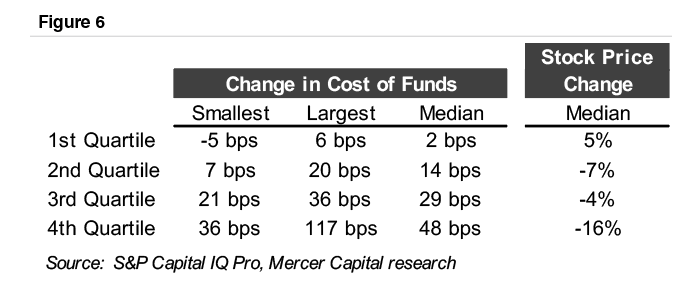

As we found out in 2022, some core deposits are more core than others. One of the strongest determinants of stock price performance in 2022 was the change in the cost of funds. We evaluated the change in the cost of funds from the first through the third quarters of 2022.3 As indicated in Figure 6, banks in the first quartile reported a median increase in the cost of funds of two basis points, whereas banks in the fourth quartile reported a median increase of 48 basis points. Further, banks in the first quartile reported a median stock price change of positive 5% in 2022, versus negative 16% for the fourth quartile banks.

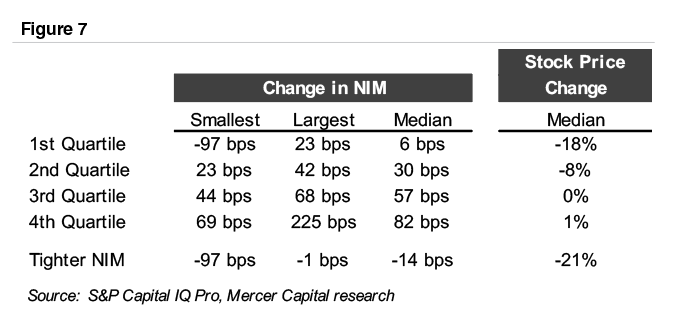

An analysis of net interest margin expansion between the first and third quarters of 2022 shows a similar result. Banks in the first quartile reported a median change in NIM of six basis points and a stock price change of negative 18%, while banks in the quartile with the most NIM expansion—82 basis points for the median fourth quartile bank—eked out a 1% positive share price appreciation.

The preceding analysis masks the market’s concern for banks with tightening NIMs, however. Among the 205 banks in our analysis, eighteen reported NIM compression between the first and third quarters of 2022. These banks underperformed, with sixteen of the eighteen reporting lower stock prices in 2022 and a median stock price decline of 21%. This indicates the market’s sensitivity to NIM compression, which will be an issue for more banks in 2023 as rising deposit rates bite.

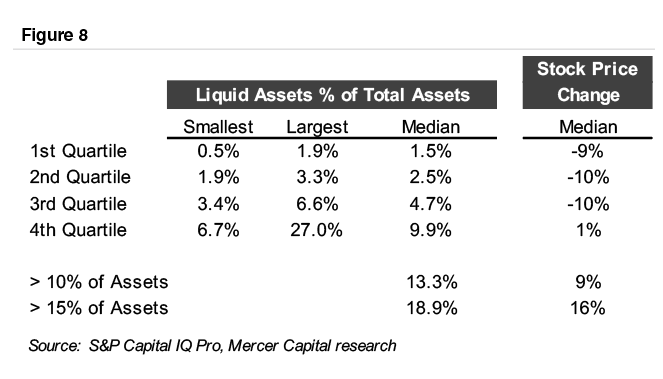

From publicly-available disclosures, it is difficult to discern the sensitivity of a bank’s assets, including both loans and securities, to rising rates. In the recent zero rate environment, pressure existed to invest in anything but short-term liquid assets. Therefore, we evaluated whether balance sheet composition could explain market performance in 2022. We could find no discernable relationship between loan/deposit ratios and market performance in 2022. However, while the evidence is somewhat weak, banks with the largest exposures to short-term liquid assets performed better in 2022.4

Figure 8 shows short-term liquid assets as a percentage of total assets. Most banks operate with short-term liquid assets in a relatively tight range (under 5% of total assets); thus, limited correlation is evident between exposure to short-term liquid assets and performance. However, a more positive relationship begins to emerge in the tail of the distribution. Banks in the fourth quartile reported liquid assets of 9.9% and a positive 1% stock price change. Narrowing the fourth quartile banks to those with liquid assets exceeding 10% or 15% of total assets results in stronger share price changes of positive 9% and 16%, respectively.

As in 2022, no doubt some newfound concerns will emerge in 2023 to drive bank stock performance. We suspect that funding cost pressure will remain an overarching concern in 2023, with true core deposits proving their value in a way not evident for years. Loan repricing will be interesting to watch. With many Prime, LIBOR, and SOFR-based floating rate loans having already repriced, further expansion in asset yields will depend on the contractual repricing periods for existing adjustable rate loans and, for newly originated loans, the “rate beta” between origination rates and broad market rates. After a long period of near nil credit losses, it would not be surprising to see some upward pressure on credit losses, although this seems likely to remain episodic in 2023. Some banks with heavier exposure to consumer loans underperformed in 2022, and it will be interesting to watch if weaknesses emerge in any segments of banks’ commercial loan portfolios in 2023.

This piece is designed to assist family law attorneys and their clients better understand tax returns because knowing how to navigate tax returns can be very useful in divorce proceedings. The information contained in tax returns can provide support for marital assets and liabilities, sources of income and potential further analyses. Reviewing multiple years of tax returns and accompanying supplemental schedules may provide helpful information on trends and/or changes and could indicate the need for potential forensic investigations.

This information originally appeared in Mercer Capital’s Family Law Valuation and Forensics Insights newsletter, a monthly publication distributed by email as well as located on our website. While we do not provide tax advice, Mercer Capital is a national business valuation and advisory firm and we provide expertise in the areas of financial, valuation, and forensic services.

To download the complimentary PDF, click “Add to Cart” or you can click here.

To celebrate a new year and everything that comes with new beginnings, the Mercer Capital Litigation Support Services Team has decided to start the year with a blog emphasizing the importance of the beginning of a family law engagement, defining the assignment.

In an engagement that requires a business valuation, the first step that attorneys and valuation experts should take is to define the assignment. This process involves the following:

While defining the assignment, the Standard of Value is another important consideration. Some simple questions that can help determine the standard of value include: Will the business continue to operate as a going concern or is a liquidation value more appropriate? Is “fair market value” or “fair value” required by the letter of the law for that specific engagement?

There are four standards of value that should be considered when defining a valuation assignment:

Each of these four business valuation standards may result in a different number to represent the value of the business, depending on the circumstances. Selecting the appropriate Standard of Value is crucial, and an experienced business valuation professional should be well-versed in selecting the standard of value that is most appropriate for the subject business interest being valued.

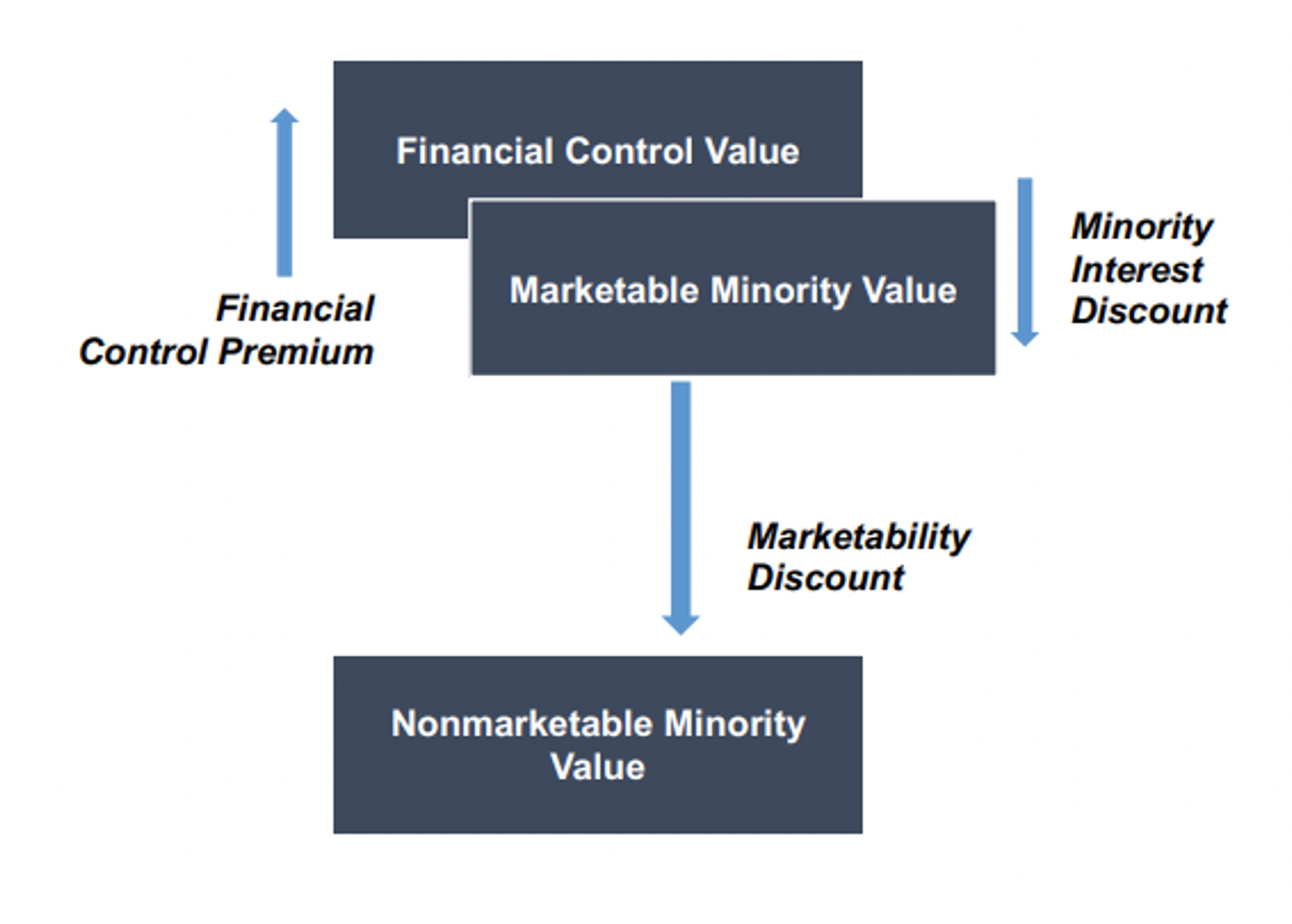

Business appraisers also refer to different kinds of values for businesses and business interests in terms of “levels of value.” As we noted in the Standards of Value section of this blog, the Fair Market Value standard of value opens the door for valuation discounts or premiums to be applied, which means that business appraisers may need to determine the appropriate Level of Value. See the chart below for the different Levels of Value that can be assigned to a valuation assignment:

To provide some examples, if the subject interest in a valuation assignment is a non-controlling minority investor, then the Nonmarketable Minority Value would likely be most appropriate. If the subject interest is a controlling owner, then the Financial Control Value could be considered. An experienced valuation expert should be able to help determine the appropriate level of value for an engagement and should also be able to quantify any Minority Interest Discount or Discount for Lack of Marketability that is deemed necessary in that engagement. Check out this blog post by Mercer Capital for a more in-depth look at the Levels of Value.

Defining the assignment in a valuation engagement can seem like a tall task but asking the right questions and having the right discussions with the right valuation expert at the beginning of an engagement can assist the process. You can think of the assignment definition process as building a road map for the valuation. Mercer Capital has extensive experience with a variety of valuation matters, including industry-expertise and complex scopes.

At this time last year, we thought bank M&A would be described as a second year of “gaining altitude” after 2020 was spent on the tarmac following the short, but deep recession in the spring of 2020. Our one caveat was that bank stocks would have to avoid a bear market following a strong performance in 2021 because bear markets are not conducive to bank M&A.

The caveat was correct. Bear markets developed in both bank stocks and fixed income that included the most deeply inverted U.S. Treasury curve since the early 1980s. Among the data points:

The outlook for deal making in 2023 is challenged by significant interest rate marks (i.e., unrealized losses in fixed-rate assets), credit marks given a potential recession, soft real estate values, and the bear market for bank stocks that has depressed public market multiples. For larger deals, an additional headwind is the significant amount of time required to obtain regulatory approval.

However, core deposits are more attractive for acquirers than in a typical year given rising loan-to-deposit ratios, the high cost of wholesale borrowings and an inability to sell bonds to generate liquidity given sizable unrealized losses. A rebound in bank stocks and even a modest rally in the bond market that lessens interest rate marks could be the catalysts for an acceleration of activity in 2023 provided any recession is shallow.

As of December 28, 2022, there have been 167 announced bank and thrift deals compared to 216 in 2021 and 117 in 2020. During the halcyon pre-COVID years, about 270 transactions were announced each year during 2017-2019.

As a percentage of charters, acquisition activity in 2022 accounted for 3.5% of the number of banks and thrifts as of January 1. Since 1990, the range is about 2% to 4%, although during 2014 to 2019 the number of banks absorbed each year exceeded 4% and topped 5% in 2019. As of September 30, there were 4,746 bank and thrift charters compared to 4,839 as of year-end 2021 and about 18,000 charters in 1985 when a ruling from the U.S. Supreme Court paved the way for national consolidation.

Also notable was the lack of many large deals. Toronto-Dominion’s (NYSE: TD) pending $13.7 billion cash acquisition of First Horizon (NYSE: FHN) represents 61% of the $23 billion of announced acquisitions this year compared to $78 billion in 2021 when divestitures of U.S. operations by MUFG and BNP and several larger transactions inflated the aggregate value.

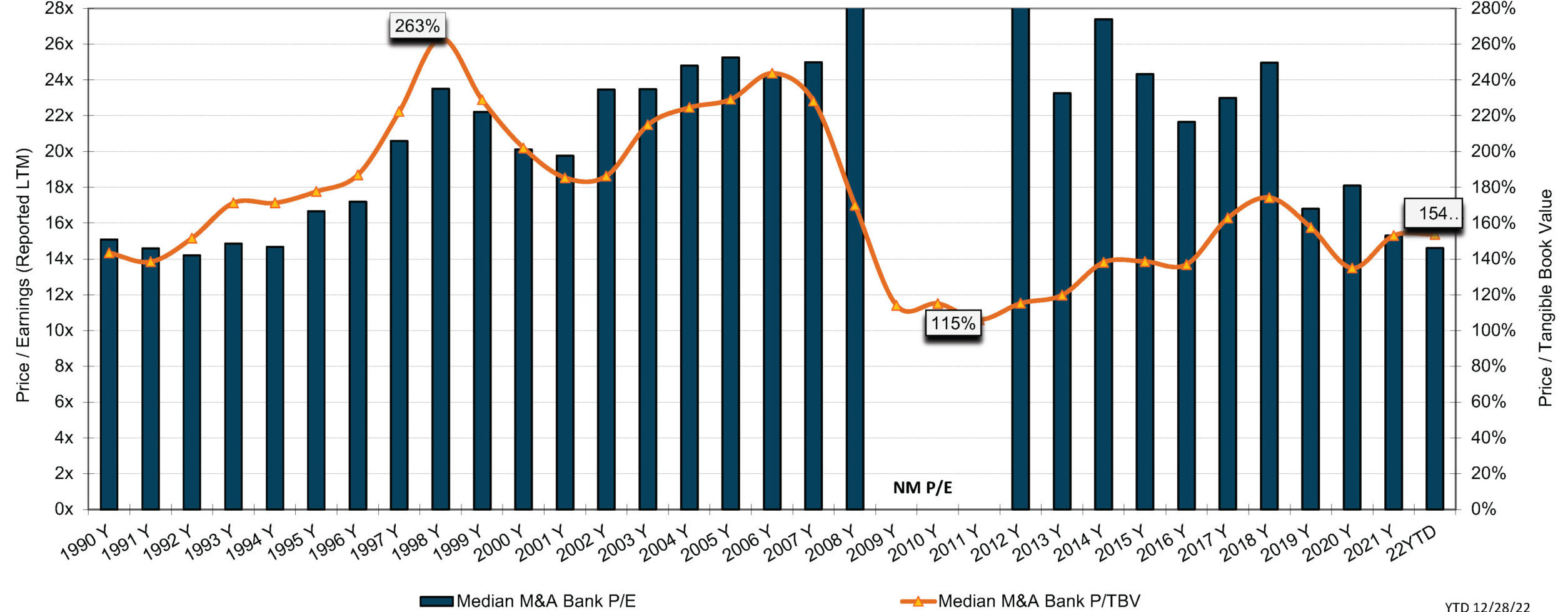

Pricing—as measured by the average price/tangible book value (P/TBV) multiple—was unchanged compared to 2021. As always, color is required to explain the price/earnings (P/E) multiple based upon reported earnings.

The median P/TBV multiple was 154% in 2022. As shown in Figure 1, the average transaction multiple since the Great Financial Crisis (GFC) peaked in 2018 at 174% then declined to 134% in 2020 due to the impact of the short but deep recession on economic activity and markets.

The median P/E in 2022 eased slightly to 14.6x from 15.3x in 2021; however, buyers focus on pro forma earnings with fully phased-in expense saves that often are on the order of 7x to 8x unless there are unusual circumstances. Accretion in EPS is required by buyers to offset day one dilution to TBVPS and to recoup the increase in TBVPS that would be realized on a stand-alone basis as investors expect TBVPS payback periods not to exceed three years.

Click here to expand the image above

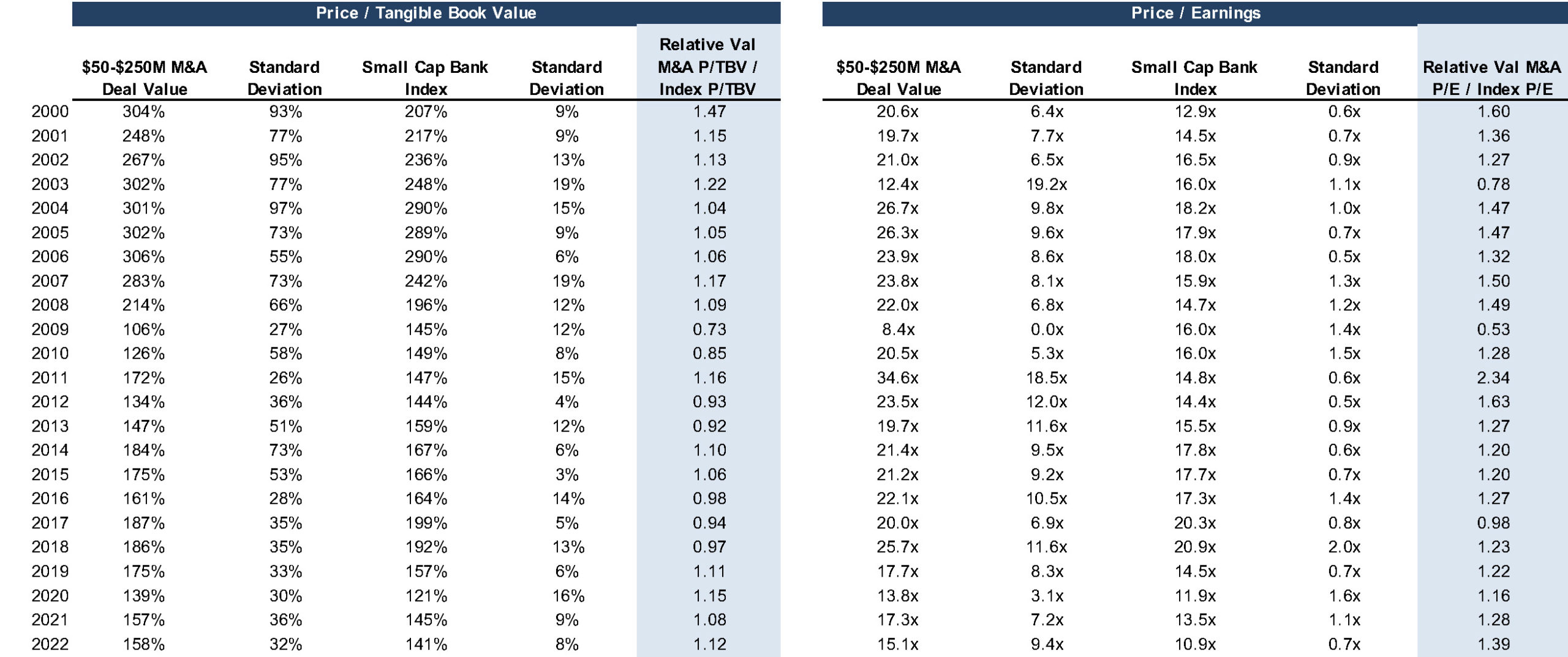

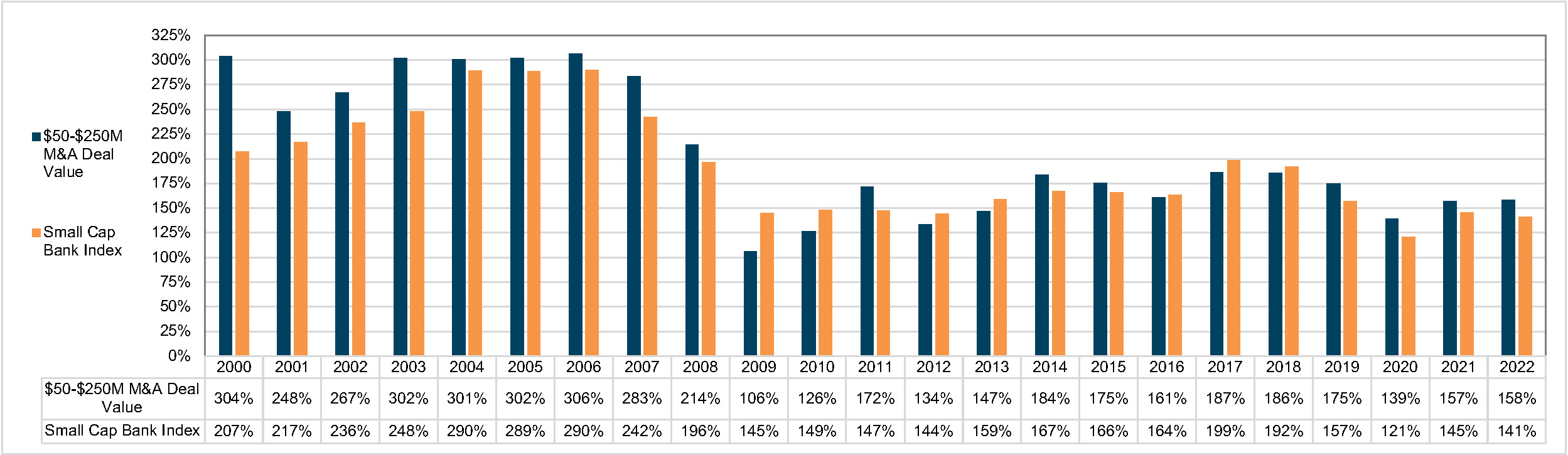

Figure 2 compares the annual average P/TBV and P/E for banks that were acquired for $50 million to $250 million since 2000 with the average daily public market multiple each year for the SNL Small Cap Bank Index.1 Among the takeaways are the following:

Click here to expand the image above

Click here to expand the image above

Investors often focus on what can be referred to as icing vs the cake in the form of acquisition premiums relative to public market prices. Investors tend to talk about acquisition premiums as an alpha generator, but long-term performance (or lack thereof) of the target is what drives shareholder returns.

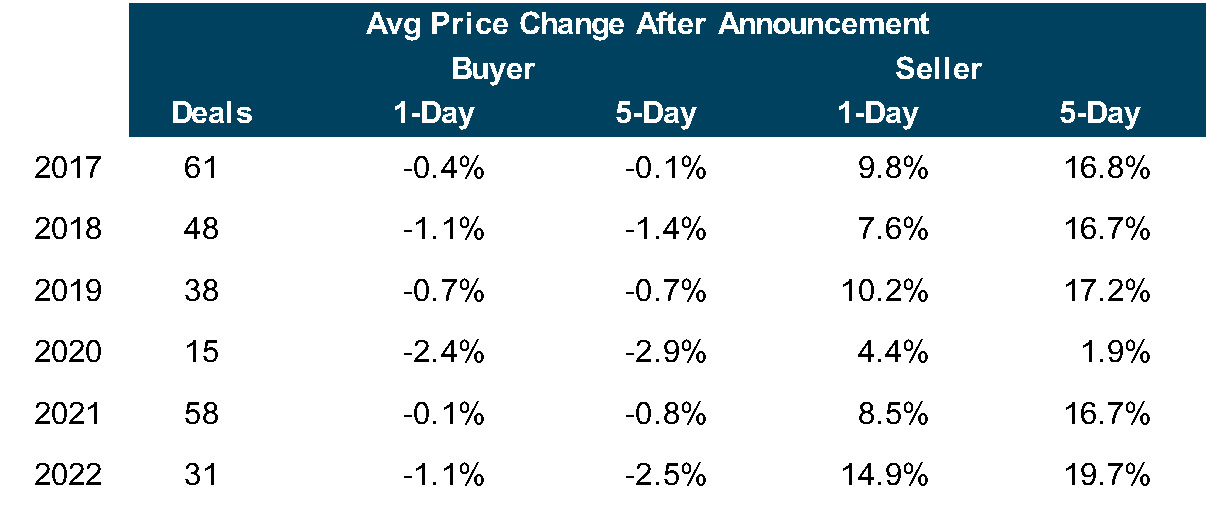

As shown in Figure 4, the average five-day premium for transactions announced in 2022 that exceeded $100 million in which the buyer and usually the seller were publicly traded was about 20%, a level that is comparable to recent years other than 2020. For buyers, the average reduction in price compared to five days prior to announcement was 2.5%. There are exceptions, of course, when investors question the pricing (actually, the exchange ratio), day one dilution to TBVPS and earn-back period. For instance, Provident Financial (NASDAQ: PFS) saw its shares drop 12.5% after it announced it would acquire Lakeland Bancorp (NASDAQ: LBAI) for $1.3 billion on September 27, 2022.

M&A entails a lot of moving parts of which “price” is only one. It is especially important for would be sellers to have a level-headed assessment of the investment attributes of the acquirer’s shares to the extent merger consideration will include the buyer’s common shares. Mercer Capital has 40 years of experience in assessing mergers, the investment merits of the buyer’s shares and the like. Please call if we can help your board in 2023 assess a potential strategic transaction.

For this quarterly update, we bring together a couple of strands of our medtech and device industry practice. First, as long-term observers, public market developments in 2022 were interesting and perhaps marked an inflection point for the short to medium term. Second, in October, we attended a medtech industry conference, where we were able to gather a rich set of perspectives. The implications for some of the larger companies in the space are probably clear-cut. The downstream reverberations to private, development stage companies may be less straightforward. Nevertheless, since development stage companies are typically constrained by currently available funds and continually contemplating the next funding round, these developments are of critical importance.

A tumultuous year in the public markets is coming to a close. By the end of the third quarter 2022, the S&P 500 was down nearly 25%, marking a near-bottom for the year. The broader medtech and devices industry largely followed suit. On the brighter side, established large, diversified companies, while lagging their own previous benchmarks, outperformed the broader market. As a group, some biotech and life sciences companies (see next section) also seemed to fare relatively well. A closer look reveals that within the group some of the larger companies with more diversified revenue bases and, perhaps more importantly, profitable operations performed much better than smaller companies promising higher growth but deferred profits.

Current profitability also appeared to differentiate better stock price performers among the medical device and healthcare technology companies. At the same time, negative sentiment was more apparent for wide swathes of these two groups compared to the broader industry. It is obvious in hindsight but over the course of 2022, as interest rates rose and remained high, markets seemed to prefer existing earnings and nearer-term cash flows over future (rosier) prospects.

The shift towards more caution also manifested in other measures of market sentiment and activity. Wholesale downward revisions of earnings (growth) estimates have not occurred so far (this may yet come to pass), so much of the price decline reflects compressing valuation multiples. The pace of M&A transactions, which had gone from strength to strength during 2020 and 2021 despite myriad disruptions and distractions, decelerated significantly in 2022. By our measure, total transactions volume in the industry through the first three quarters of 2022 was roughly equal to that of just the fourth quarter of 2021. The number of IPOs also slowed to a trickle.

No industry is an island but as we and others have pointed out, several long-term trends, demographic and otherwise, suggest a favorable overall outlook for the medtech and device space. Even against the seemingly dour recent market backdrop, a multitude of attendees at the medtech conference agreed on the relative merits of the industry compared to the broader economy and market. We work with a number of development stage medtech and device companies over the course of a typical year. From that perspective, we find the long-term trends interesting because of the structural emphasis on continual innovation that improve outcomes for patients and clinicians.

A defining feature of medtech innovation funding is that it occurs over multiple tranches as the technologies and companies achieve various developmental milestones. In this context, some observations for development stage companies:

An obvious first order effect of the recent public market developments over the past year is that development stage companies should expect generally lower valuations for funding rounds (at least) over the next couple of years.

Lackluster exit activity, via either M&A or IPO, delays and/or reduces deployable capital for venture capital funds, which will make them more cautious in considering investment decisions.

The sentiment shift towards more caution is shared by all investors, although the degrees will differ. Accordingly, in addition to valuation compression, some types of companies (for example, those at the pre-clinical stage) will find fundraising to be extremely difficult.

As a corollary, investors are likely to prize clean clinical data. Companies focused on demonstrating good clinical outcomes will be better prepared for future funding rounds.

Similarly, companies that can stretch their existing funds until they can achieve a good (clinical) milestone will be better rewarded in the next funding round.

Commercial traction after hurdling regulatory approval remains an important structural consideration, especially for the non-corporate investors.

Beyond the near-term market dynamics, a key conference takeaway for us was that the medtech funding eco-system is deep and diverse. We met and heard from traditional venture capital investors, corporate investors, and folks who operate in the continuum between them. The goals for the various investors differ to some degree, with some focused on financial attributes while others (like corporate VCs) include strategic considerations in the mix. Investors with broader goals and considerations are, to an extent, less sensitive to the prevailing market conditions and can afford to take a longer-term view. Even among these investors, financial terms and preferred deal structures vary considerably.

For development stage companies contemplating fundraising efforts, a deep and diverse investor eco-system can provide plenty of optionality. In keeping with a recurring theme of this update, a note of caution – evaluating a potential funding round requires both an examination of the financial terms and an understanding of the structural features and their longer-term implications.

Mercer Capital has broad experience in providing valuation services to medtech and device start-ups, larger public and private companies, and private equity and venture capital funds involved in the sector. Please contact us to discuss how we may be of help.

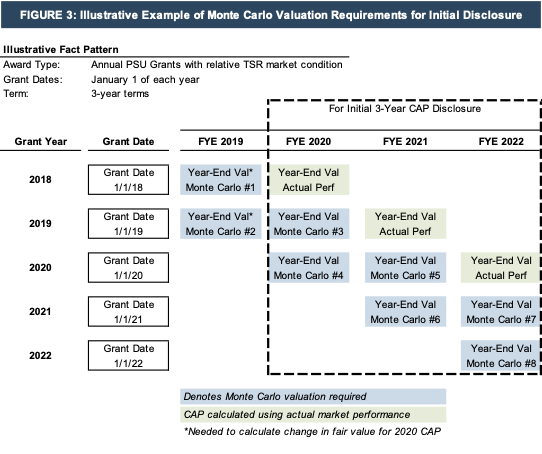

In August 2022, the SEC adopted final rules implementing the Pay Versus Performance Disclosure required by Section 953(a) of the Dodd-Frank Act. These rules go into effect for the 2023 proxy season and introduce significant new valuation requirements related to equity-based compensation paid to company executives. What does this mean, and how does it apply to you? What are the requirements, and why might there be significant valuation challenges involved? We discuss all that and more below.

Advance planning and processes will be needed to establish the scope and complexity of complying with the new rules, including identifying how many equity-based awards will require updated valuations to measure the period-to-period changes.

The new disclosures were mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act and were originally proposed by the SEC in 2015. These rules will add a new item 402(v) to Regulation S-K and are intended to provide investors with more transparent, readily comparable, and understandable disclosure of a registrant’s executive compensation. The new provisions apply to all reporting companies other than (i) foreign private issuers, (ii) registered investment companies, and (iii) emerging growth companies.

The rules apply to any proxy and information statement where shareholders are voting on directors or executive compensation that is filed in respect of a fiscal year ending on or after December 16, 2022. As such, the vast majority of registrants will be required to include related disclosure for their 2023 proxy statements, though there are relaxed requirements for smaller reporting companies.

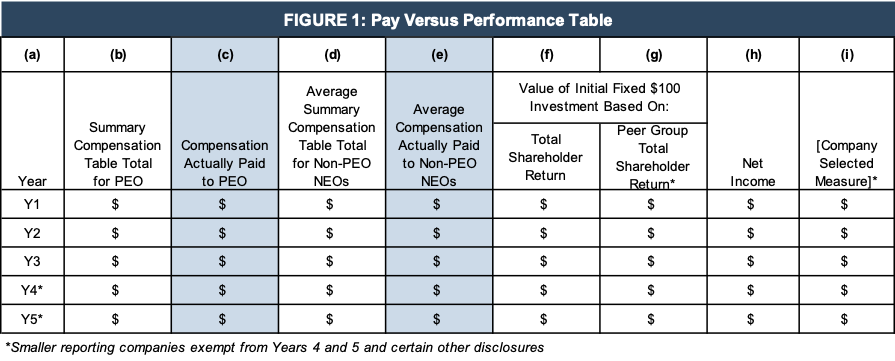

The new rules require registrants to describe the relationship between the Executive Compensation Actually Paid (“CAP”) and the financial performance of the registrant over the time horizon of the disclosure. Additional items include disclosure of the cumulative Total Shareholder Return (“TSR”) of the registrant, the TSR of the registrant’s peer group, the registrant’s net income, and a company-selected measure chosen by the registrant as a measure of financial performance. These items are to be disclosed in tabular form (based on an example included in the final rule), which is replicated below.

Click here to expand the table above

The table includes the following components:

The remainder of this article focuses on the two shaded columns (c) and (e) which address Compensation Actually Paid and the valuation inputs that support these disclosures.

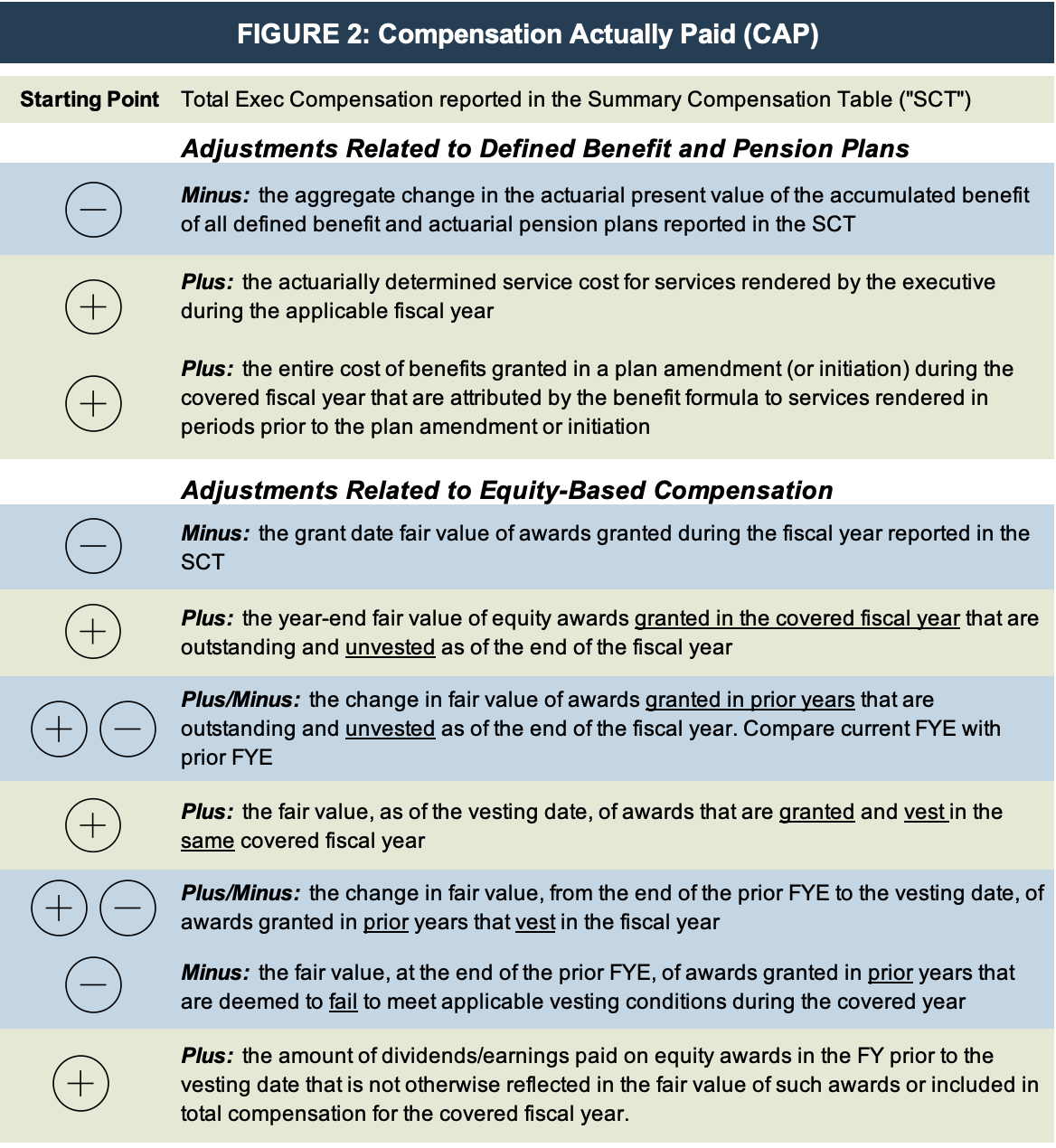

For each fiscal year, registrants are required to adjust the total compensation reported in Columns (b) and (d) for pension and equity awards that are calculated in accordance with US GAAP. The following table describes these adjustments in detail.

The pension-related adjustments should be calculated using the principles in ASC 715, Compensation – Retirement Benefits. The equity-based compensation adjustments will require registrants to disclose the fair value of equity awards in the year granted and report changes in the fair value of the awards until they vest. This means that it will be necessary to measure the year-end fair value of all outstanding and unvested equity awards for the PEO and other NEOs under a methodology consistent with what the registrant uses in its financial statements. For most registrants, this will be ASC 718, Compensation – Stock Compensation.

Appropriate footnote disclosure may also be required to identify the amount of each adjustment and any valuation assumptions that materially differ from those disclosed at the time of the equity grant.

The procedures used to calculate fair value will vary depending on the type of equity award.

Market condition awards come in many different flavors. Three of the most common types of plans include:

Each of the above plans has inputs and assumptions that drive the Monte Carlo simulation. When performing a subsequent year-end or vesting date fair value analysis, each of the grant-date assumptions will need to be reevaluated. For example, for a relative TSR plan with a three-year term, the subsequent year-end valuations will necessarily have shorter terms (2-year and 1-year), which will require new inputs for volatility and correlation factors. Shorter terms may make the use of option-implied volatility more relevant if sufficient market data is available.

For relative TSR plans that reference a group of companies or an index, some of the peers may have been acquired or merged in the subsequent periods. The plan documentation will often describe the steps to be taken when the composition of the peer group changes or there is a change in the benchmark index. A different group (or number) of companies will affect the correlation assumption as well as the percentile calculations in a ranked plan.

Regardless of the type of plan, it is important for registrants to understand how even a relatively simple award, if granted consistently for a period of years, can lead to a large number of Monte Carlo simulations for this initial proxy season and a significant amount of disclosure complexity.

As shown in Figure 3 below, if a company has made annual PSU grants (with a market condition) for each of the last five years, then up to eight Monte Carlo valuations could be required to calculate the CAP in each period.

Click here to expand the example above

In the example above, the blue boxes indicate when a valuation of prior grants would be necessary to calculate the change in fair value for each period of the CAP disclosure. For the final period of a relative TSR market condition plan, the company could use the actual market performance of its stock (and the comparative index) to calculate the expected value of the award.

While the new SEC Pay Versus Performance disclosure rules can seem daunting, they can be managed with proper planning and a systematic approach. For the CAP disclosures, registrants need to understand the details of all equity awards that have been awarded to named executive officers (how many and what type of award). The award characteristics will determine which valuation method is most appropriate and how many valuations need to be performed.

If you have questions about the valuation techniques used for the various types of equity compensation awards or would like to discuss the process, please contact a Mercer Capital professional.

The U.S. bond market is undergoing its worst bear market in decades. Barclays U.S. Aggregate Bond Market Index produced a total return of negative 14.5% through September 30, 2022 and negative 16.0% through November 8, 2022. Excluding coupon income, the year-to-date loss was 17.2% which speaks to how low coupon income is given the nominal difference between price change and total return.

Click here to expand the image above

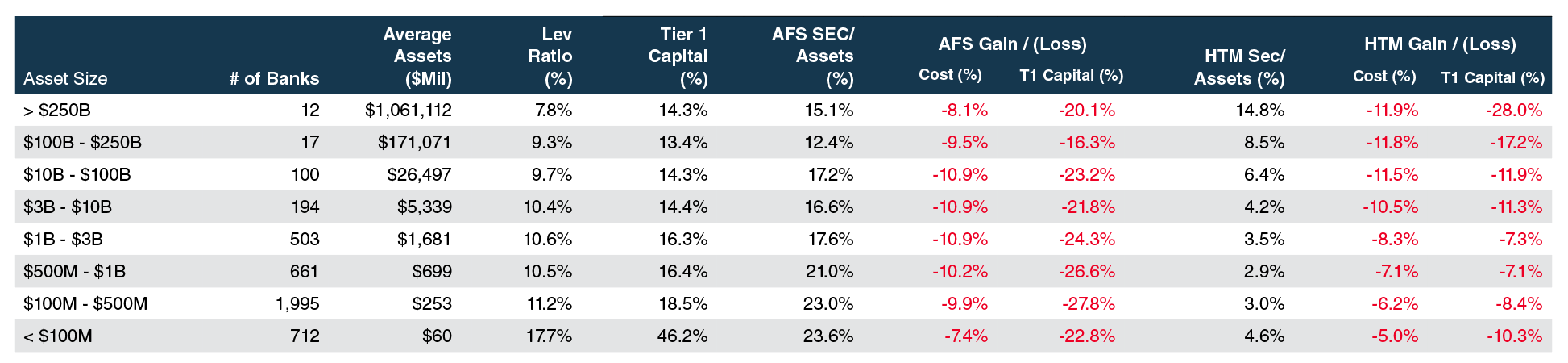

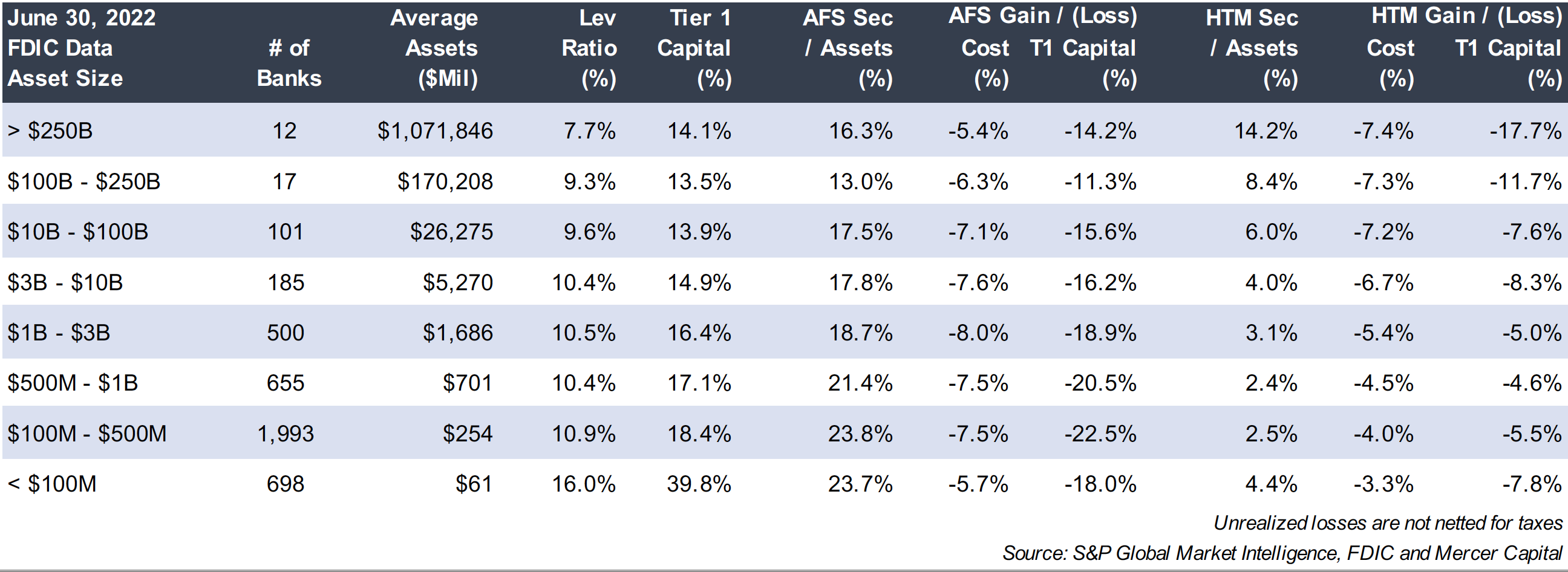

As shown in the figure below, U.S. commercial banks have suffered unrealized losses in their bond portfolios equal to roughly 10% of the cost basis of both AFS and HTM classified portfolios as of September 30, which compares to a price reduction of 15.6% in the Barclay’s index as of quarter end.

The less-worse performance by U.S. banks likely reflects less duration than the index, which has an effective duration of 6.25 years and weighted average maturity of 8.25 years. Our observation is that for the most part outsized losses among U.S. banks reflect an outsized position in municipals and/or MBS. The index composition is heavily skewed to U.S. Treasuries and U.S. Agency obligations given the heavy issuance of government backed debt the past 15 years or so.

While management and directors at most banks are unhappy with their bond portfolios, institutional investors have taken a more nuanced view of the impact of rising rates based upon the tenor of third quarter earnings calls and the reaction of most stocks upon the release of earnings. Rising rates have supported bank earnings even though fixed-rate loan and bond portfolios are slow to reprice as floating-rate loans have repriced and banks have lagged deposit rates.

Investor concern is more focused on liquidity risks. Some (or many) banks eventually may have to raise deposit rates sharply to stem outflows and/or fund loan growth because selling bonds is not a viable option given the magnitude of unrealized losses that if realized will reduce regulatory capital.

Our prior commentary on bank bond portfolios following the release of the first and second quarter Call Reports can be found here and here.

Fixed income is undergoing one of the deepest bear markets in decades this year. There has been a lot of discussion surrounding the impact of rising rates on bank bond portfolios and bank stocks as rising rates have resulted in large unrealized losses in bank bond portfolios. My colleague, Jeff Davis, provides an update to his previous commentary on the topic based on third quarter Call Report data here.

If subjected to mark-to-market accounting like the AFS securities portfolio, most bank loan portfolios would have sizable losses too given higher interest rates and wider credit spreads; however, unrealized “losses” in loan portfolios do not receive much attention because there is not an active market for most loans unlike most bonds that populate bank portfolios. Further, accounting standards do not mandate mark-to-market for loans other than those held-for-sale.

While the trend in loan portfolio fair values is harder to examine given the lack of data, the following charts provide some perspective based on a survey of periodic loan portfolio valuations by Mercer Capital. To properly evaluate a subject loan portfolio, the portfolio should be evaluated on its own merits, but markets do provide perspective on where the cycle is and how this compares to historical levels.

Fair value is guided by ASC 820 and defines value as the price received/paid by market participants in orderly transactions. It is a process that involves a number of assumptions about market conditions, loan portfolio segment cash flows inclusive of assumptions related to expected prepayments and expected credit losses, appropriate discount rates, and the like.

The fair value mark on a subject loan portfolio includes two components – an interest rate mark and a credit mark. The interest rate mark is driven by the difference in the weighted average discount rate and weighted average interest rate of the subject portfolio. The discount rate that is applied to a subject loan should reflect a rate consistent with the expectations of market participants for cash flows with similar risk characteristics. The credit mark captures the risk that the borrower will default on payments and not all contractual cash flows will be collected.

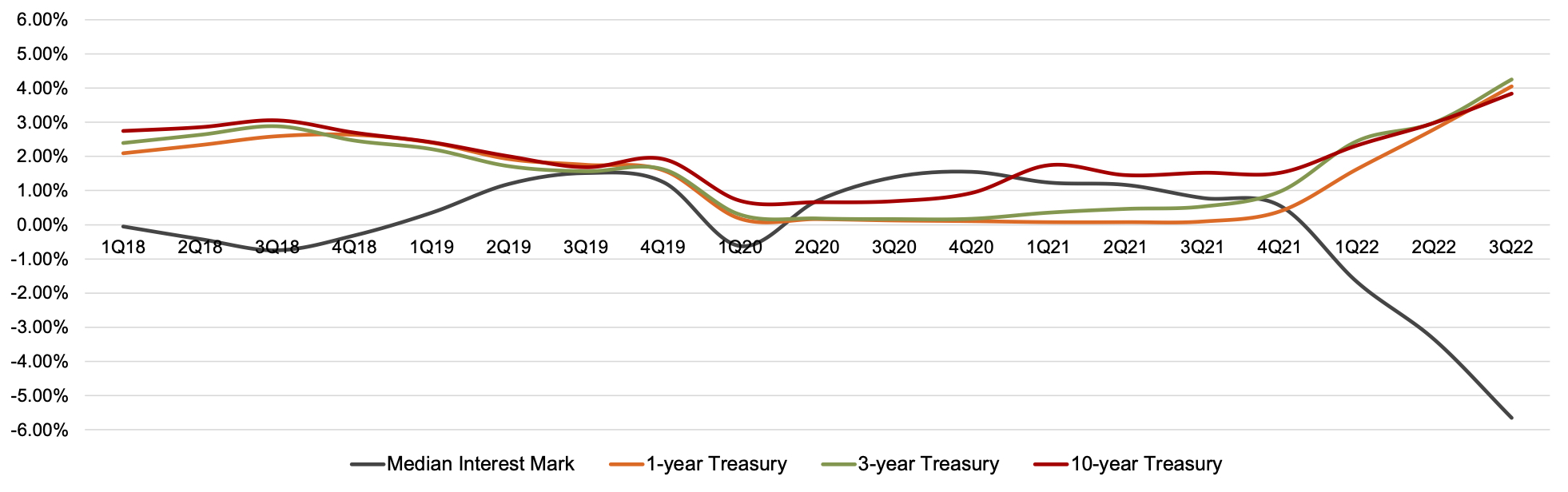

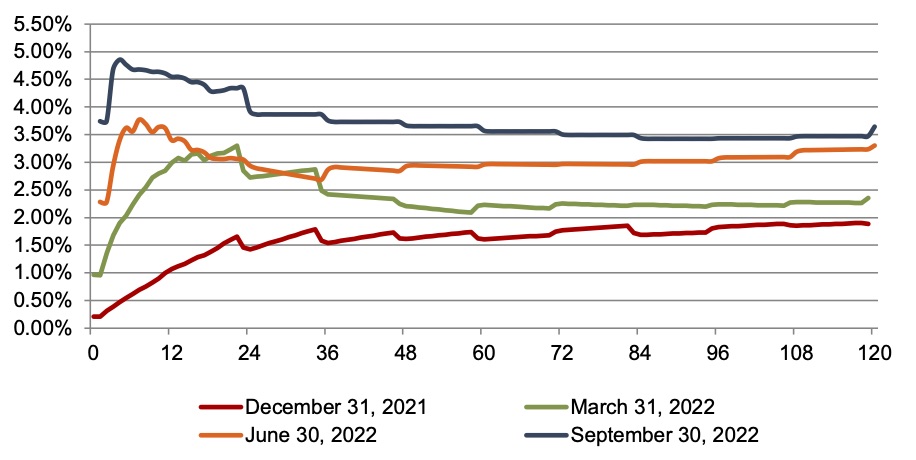

Since the end of 2021, rising market interest rates have been the predominant factor driving the change (i.e., reduction) in loan portfolio fair values. As shown in Figure 1, the median interest rate mark for our data sample has fallen from a modest 0.55% premium at December 31, 2021 to a 5.65% discount as of September 30, 2022. While bank earnings benefit from a higher rate environment and net interest margin expansion, it takes time for the increase in market rates to be passed on to customers via higher loan rates and for lower, fixed-rate loans to roll out of the portfolio. In talking with Mercer Capital clients and in our loan portfolio valuation practice, so far it seems that banks have been unable to fully pass on the increase in rates to loan customers.

Click here to expand the image above

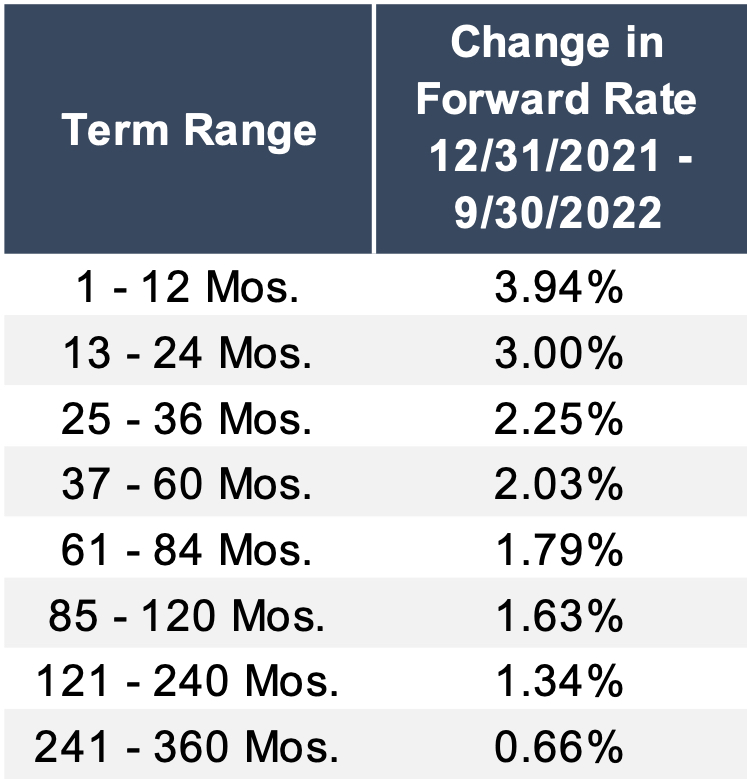

The shift in the valuation adjustment attributable to interest rates reflects an increase in market interest rates. Figure 2 depicts the LIBOR forward curve at December 31, 2021, March 31, 2022, June 30, 2022, and September 30, 2022. Relative to December 31, 2021, forward LIBOR rates have increased 66 bps to 394 bps on average with the largest increases occurring for periods ranging from 1 to 12 months following the valuation date.

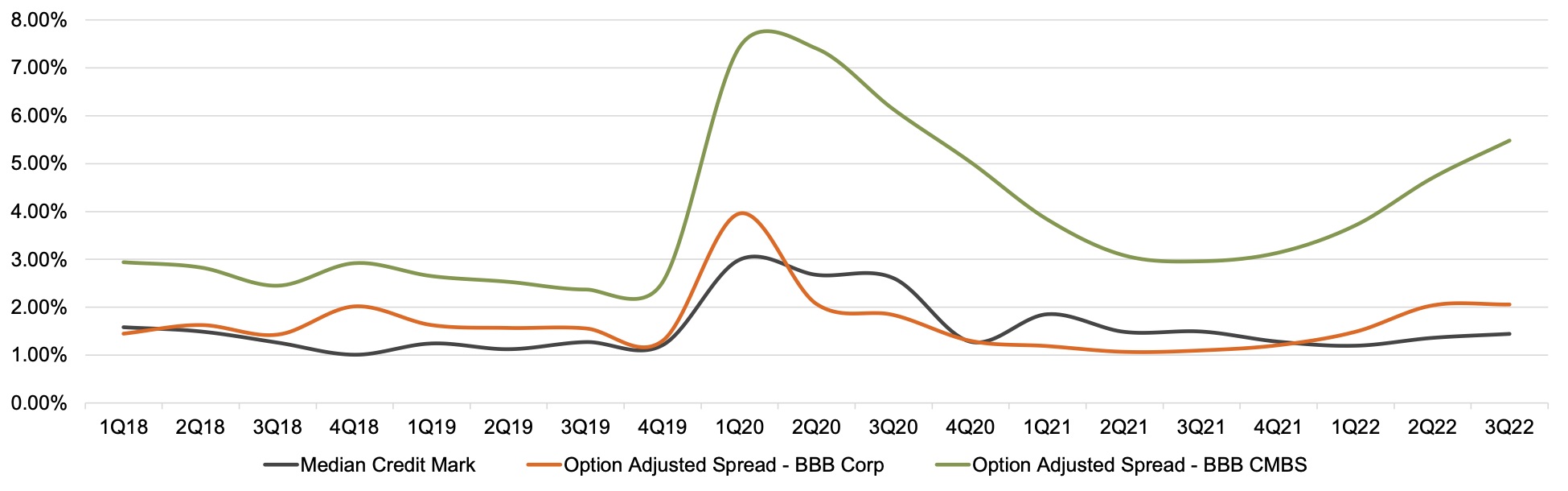

Figure 3 depicts the trend in the credit mark for our data sample relative to credit spreads. Credit spreads provide perspective on a number of factors, including where the credit cycle has been and where we may be headed.

Click here to expand the image above

Over the period shown in Figure 3, credit marks peaked at the start of the pandemic given the uncertainty and expectation of higher losses on loan portfolios. Credit marks trended down from the March 31, 2020 peak through the first quarter of 2022, as did banks’ loan loss provisions, as credit quality remained stable. While credit quality continues to remain strong, both credit spreads and credit marks have ticked up in 2022 with the weakening economic outlook and concerns that the Federal Reserve’s tightening interest rate policy may trigger a sharper downturn in economic activity.

Mercer Capital has extensive experience in valuing loan portfolios and other financial assets and liabilities including depositor intangible assets, time deposits, and trust preferred securities. Please contact us if we can be of assistance.

In-person conferences are back in 2022 and so are we. Our professionals have been speaking at and attending numerous conferences, so we thought it a good idea to reflect on a few of these conferences and share selected PowerPoint decks with you. Why? Because there are valuable materials on valuation, forensic and financial topics included in these PowerPoint decks. If your organization needs a speaker at your next conference or meeting, feel free to contact us.

We hope you have enjoyed our content in 2022 and we look forward to connecting further in 2023!

In this presentation, we ask and answer the questions “what is the purpose of a business valuation?”, “when and why a valuation is needed?” and explore what to look for in a valuation expert. In addition, this presentation provides an overview of valuation approaches and common valuation discounts. Active vs. passive appreciation and personal vs. enterprise goodwill are also presented. If you need a solid valuation overview, download the deck.

Is valuation an art or a science? This presentation begins with an overview of valuation theory. In addition, we include common flaws in valuations, provides an example of double/triple counting, and includes a valuation report checklist. For more, download the powerpoint deck.

Particularly when the marital estate includes a business asset, subject to a valuation, the topic of double counting must be considered. Is the same income stream which is creating a valued asset on the marital balance sheet also being used for income determination for support? Or, has compensation and business earnings properly been allocated to the asset and to the income? Further, what if there is a carve out to personal goodwill – how, if at all, does this impact the asset division as well as the income basis for support? We address these questions in this presentation.

What are the nuances and critical issues of valuation, forensic, and other analyses for marital dissolution? In this presentation, we delve into specific issues that must be considered since they are unique to marital dissolution as well as state statute and precedent. Specifically, we touch on if a marital asset ever become a separate asset or vice-versa, personal vs. enterprise goodwill, valuation adjustments in marital dissolution engagements, double-dipping, asset tracing, and how to construct a lifestyle (pay and need) analysis.

Chris Mercer is one of the founding fathers of business valuation. Given his place in the profession, he is one of the few qualified to opine to the future of the business valuation profession. In this presentation, he begins by discussing the profession’s current realities and then ventures into what the future might hold about the profession, valuation theory, and how to reach the market.

In this presentation, our Karolina Calhoun along with Kevin Segler from Koons Fuller, covered all things related-party in divorce valuation, including entity structure issues, multi-layering with discounts, and tracing marital vs. separate asset ownership with complex multi-entity ownerships. Karolina and Kevin also discussed related parties in the business and said impact on ownership, valuation, and division – including the consideration of classes of stock in division, such as GP vs. LP or voting vs. non-voting.

David Harkins joined Karen Shapiro of Stein Sperling and Michele Laws of Turning Point Financial Group on a panel moderated by Cheryl Panther of Panther Financial Planning, to discuss the nuances of a case study presented to members of the ADFP. The case had numerous potential pitfalls with considerations for attorneys and divorce financial planners alike. Topics included business valuation, fraud, forensics, separate vs marital, etc. The crowd had numerous thought-provoking questions which led to an enlightening dialogue for all involved.

Karolina Calhoun and Audra Moncur of Wipfli, LLP tackled the questions: what is goodwill?; what is personal vs. enterprise goodwill?; and why is personal vs. enterprise goodwill important in valuations for divorce or transactions? They also presented an illustration of goodwill in transactions and presented case precedent for goodwill in divorce along with methods and considerations for determination allocation to personal and enterprise goodwill.

As we assist with complex financial and valuation issues on many Florida matters, this year we decided to sponsor and attend the AAML Florida Chapter Annual Institute. We enjoyed meeting and seeing familiar faces, and also appreciated conversations about complex valuation and financial issues. Mercer Capital’s Litigation Team looks forward to attending in future years!

Attending the Conference was:

Karolina Calhoun, CPA, ABV, CFF

November 10, 2022 | Chicago, Illinois

We were honored to be a Diamond Sponsor of the AAML Foundation Lifetime Members Luncheon, supporting the Foundation’s mission to assist families and children. Chris Mercer, Karolina Calhoun, and Scott Womack are members of the Forensic & Business Valuation Division of the AAML Foundation.

Attending the Luncheon were:

Scott A. Womack, ASA, MAFF

Karolina Calhoun, CPA, ABV, CFF

David W. R. Harkins, CFA, ABV

|

|

|

The AAML Florida Chapter

|

The AAML Florida Chapter

|

2022 AICPA & CIMA Forensic & Valuation Services ConferencePictured (L-R): Bethany Hearn (CLA), Karolina Calhoun, Natalya Abdrasilova (BDM), and Nicole Lyons (WithumSmith+Brown) |

|

|

|

2022 AAML Foundation Lifetime Members LuncheonPictured (L-R): Scott Womack, Karolina Calhoun, and David Harkins |

2022 AAML Foundation Lifetime Members LuncheonPictured (;-R): David Harkins, Bill Dameworth (Forensic Strategic Solutions), Jay Fishman (Financial Research Associates), Karolina Calhoun, and Scott Womack |

2022 AAML Foundation Lifetime Members LuncheonPictured (L-R): Paul Thiel (Northern Trust), Scott Womack, Karolina Calhoun, and David Harkins |

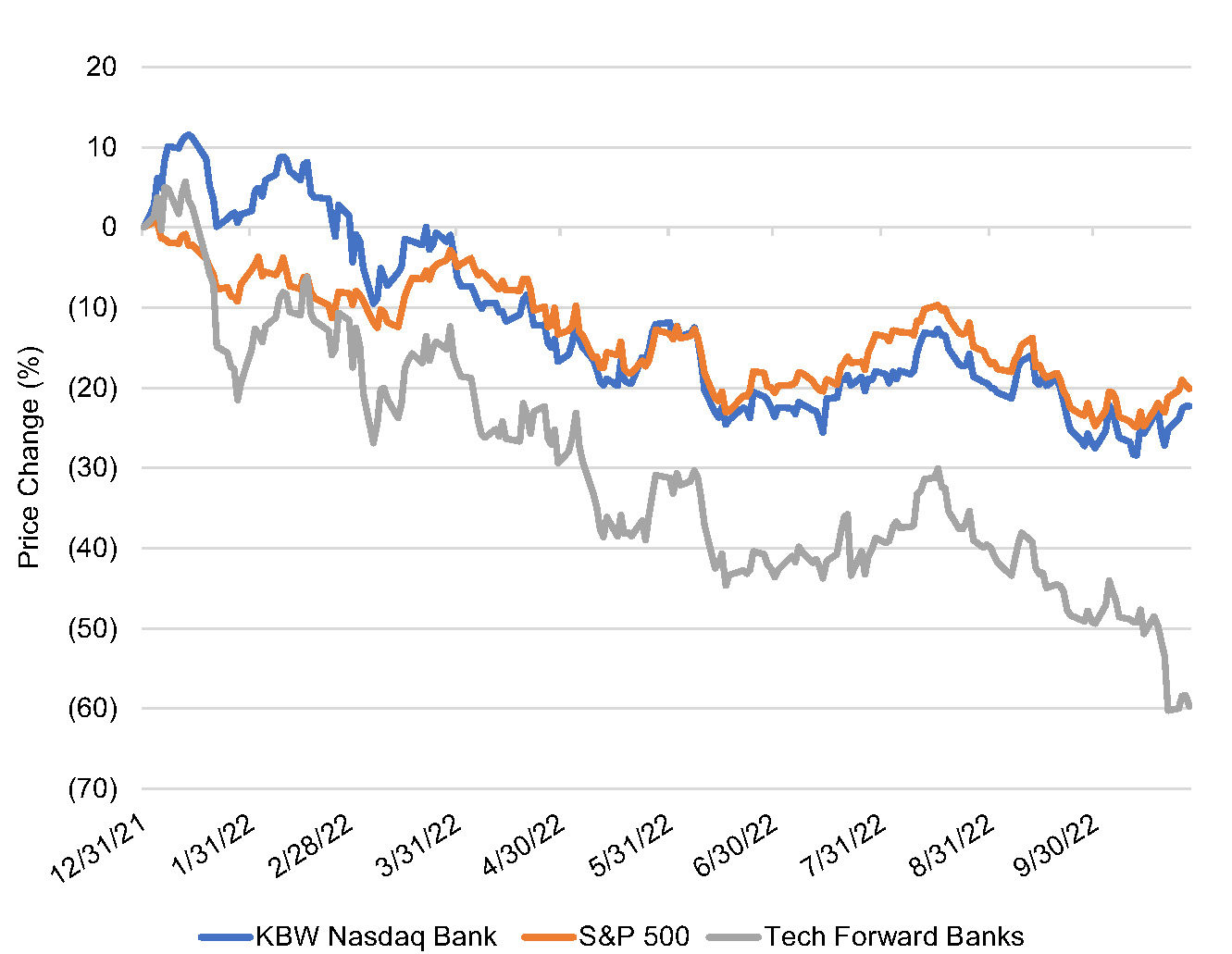

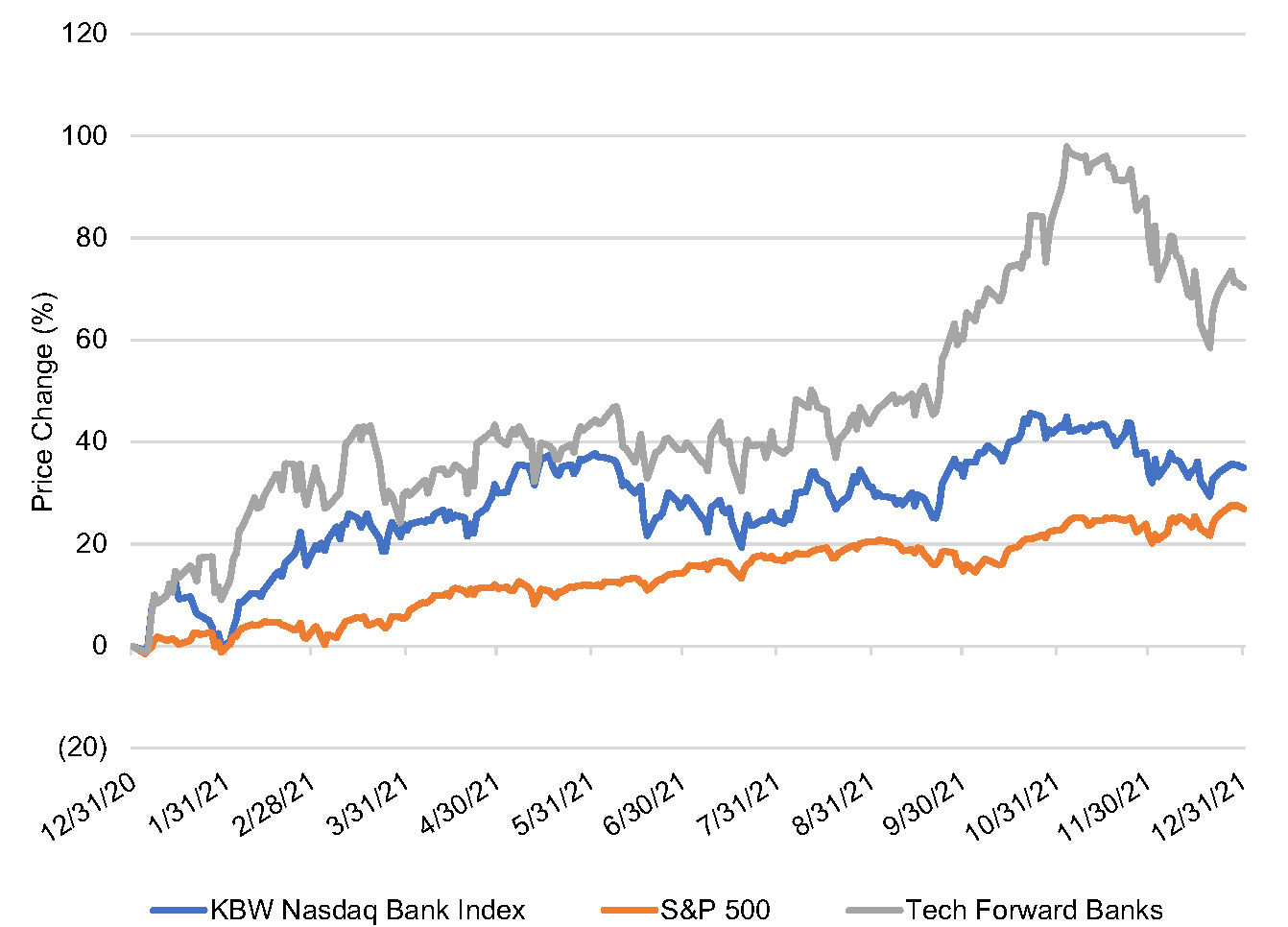

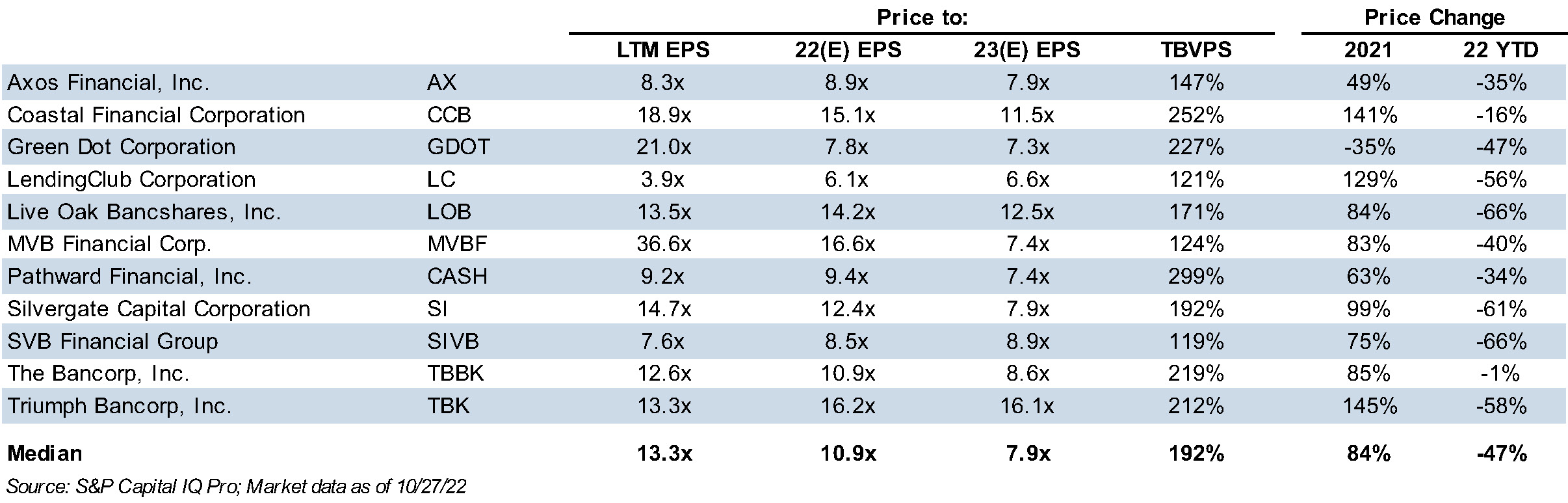

In the year-to-date period, the KBW Nasdaq Bank Index has declined 22%, compared to a decline of 20% in the S&P 500 through October 27. Tech-forward banks have underperformed the broader banking sector, down 60% in the year-to-date period.1 This is a reversal of the trend in 2021 when tech-forward banks outperformed the broader banking sector, logging a 70% increase compared to an increase of 35% in the KBW Nasdaq Bank Index.

Source: S&P Capital IQ Pro.

Source: S&P Capital IQ Pro.

The tech-forward bank landscape encompasses a variety of business models but generally refers to banks utilizing technology or partnering with fintechs to deliver financial products or services. Banks that partner with fintechs are often referred to as providing “banking as a service (BaaS)”. This model involves an FDIC member bank offering bank products to fintech customers, for example, credit and debit cards or personal loans. The bank holds the deposits associated with the accounts and earns a fee based on a percentage of interchange income specified in an agreement negotiated with the fintech partner. Other models are focused on facilitating payments or providing financial services to a specific niche, such as cryptocurrency.

While the largest banks have the resources to be at the forefront of technology adoption, many smaller banks have partnered with fintechs in recent years. This is due in part to the Durbin Amendment which places limits on interchange income for banks above $10 billion in assets. In many cases, the partnerships have accelerated growth and created new income streams for the bank partners.

However, bank partners also face unique risks. As displayed in the market performance, tech-forward banks have been more volatile than traditional banks. Tech-forward bank performance has been moored, to some degree, to more volatile technology stocks, which explains the stock market outperformance in 2021 followed by a larger retrenchment in 2022. For a community bank pursuing a fintech partnership strategy, there are multiple considerations, including the following.

Many fintech partner banks have continued growing deposits this year even though most banks have seen deposit growth stagnate or turn negative in the rising rate environment. An analysis performed by S&P Global Market Intelligence showed that fintech partner banks with assets between $1 billion and $3 billion experienced deposit growth of 15% (annualized) in the first half of 2022. This compares to deposit growth of 3% for commercial banks in the same asset size range.

The deposits generated from fintech partnerships are often noninterest bearing accounts, which are especially valuable in the current rising rate environment. Bank partners earn spread income from the deposits, often holding them at the Federal Reserve due to their volatility and uncertain duration. Balances at the Fed reprice immediately with changes to the Fed’s benchmark rate.

The largest impact on the revenue side typically shows up in noninterest income. Fintech partner banks tend to have a higher ratio of noninterest income to total income relative to traditional banks as they earn a share of the interchange income. In a period of flat or declining interest rates, this diversification of revenue can help to offset net interest margin compression.

For the tech-forward banks included in Figure 1 and 2, the median ratio of noninterest income to operating revenue was 29% in the trailing twelve

month period.

While fintech partnerships can be a source of growth, bank partners should be cautious about revenue or deposit concentrations. Fintechs can grow rapidly, and, as a result, a bank partner may develop a concentration within their deposit base or revenues. Banks must periodically renegotiate contracts with fintech partners, and there is a risk that the fintech will find another bank partner or demand more favorable terms. This single event could eliminate a major source of deposits or reduce noninterest income, causing a much greater impact than the ordinary loss of traditional bank customers.

For example, Green Dot Corporation (GDOT) provides the Walmart MoneyCard product and offers other deposit account products at Walmart. Green Dot’s second quarter 10-Q discloses that approximately 21% of its operating revenue in the year-to-date period was derived from products and services sold at Walmart locations.

Regulators have stepped up their scrutiny of bank-fintech partnerships this year, focusing on risk management controls. Many banks partnering with fintechs have less than $10 billion in assets, and banks that do not currently serve fintechs may not have the necessary compliance infrastructure to effectively manage potential fintech relationships. Compliance capability must be built over a long period of time and serves as somewhat of a barrier to entry for banks desiring to pursue this strategy.

Additionally, certain fintech partnerships may present an added element of risk as the bank could be impacted by the regulatory and compliance practices of the fintechs or the evolving regulatory/compliance landscape. One recent example of this risk arose in the crypto fintech niche as the FDIC released an order to a crypto brokerage firm demanding that it cease and desist from making false and misleading statements about its deposit insurance status, while the FDIC contemporaneously issued an advisory to insured institutions regarding FDIC deposit insurance and dealings with crypto companies.2

Bank stocks’ underperformance in 2022 has largely been attributed to economic uncertainty and the potential for recession brought on by the Fed’s aggressive rate hikes. Fintech partner banks have been more volatile than the broader banking market. The business models entail certain risks, as detailed above, that do not pertain to traditional banks to the same degree. In addition, the earnings from fintech partnerships are less predictable and potentially further out in the future.

As seen in figure 3, the range of valuation multiples observed for tech forward banks is wide, with forward P/Es ranging from 6.6x to 16.1x but most trade at 7x to 9x estimated 2023 earnings. It is important to note that the banks included in the table above represent a variety of sizes, strategies and niches, so comparability may be somewhat limited. Tangible book multiples likewise exhibit a wide range, but in general are high relative to the broader banking sector. In valuing fintech partner banks, investors weigh the growth potential provided by the partnership versus the risk that earnings growth does not materialize.

Click here to expand the image above

Mercer Capital has experience valuing and advising both banks and fintechs. If you are considering partnership opportunities or have questions regarding their valuation implications, please contact us.

The medical device manufacturing industry produces equipment designed to diagnose and treat patients within global healthcare systems. Medical devices range from simple tongue depressors and bandages to complex programmable pacemakers and sophisticated imaging systems. Major product categories include surgical implants and instruments, medical supplies, electro-medical equipment, in-vitro diagnostic equipment and reagents, irradiation apparatuses, and dental goods.

The following outlines five structural factors and trends that influence demand and supply of medical devices and related procedures.

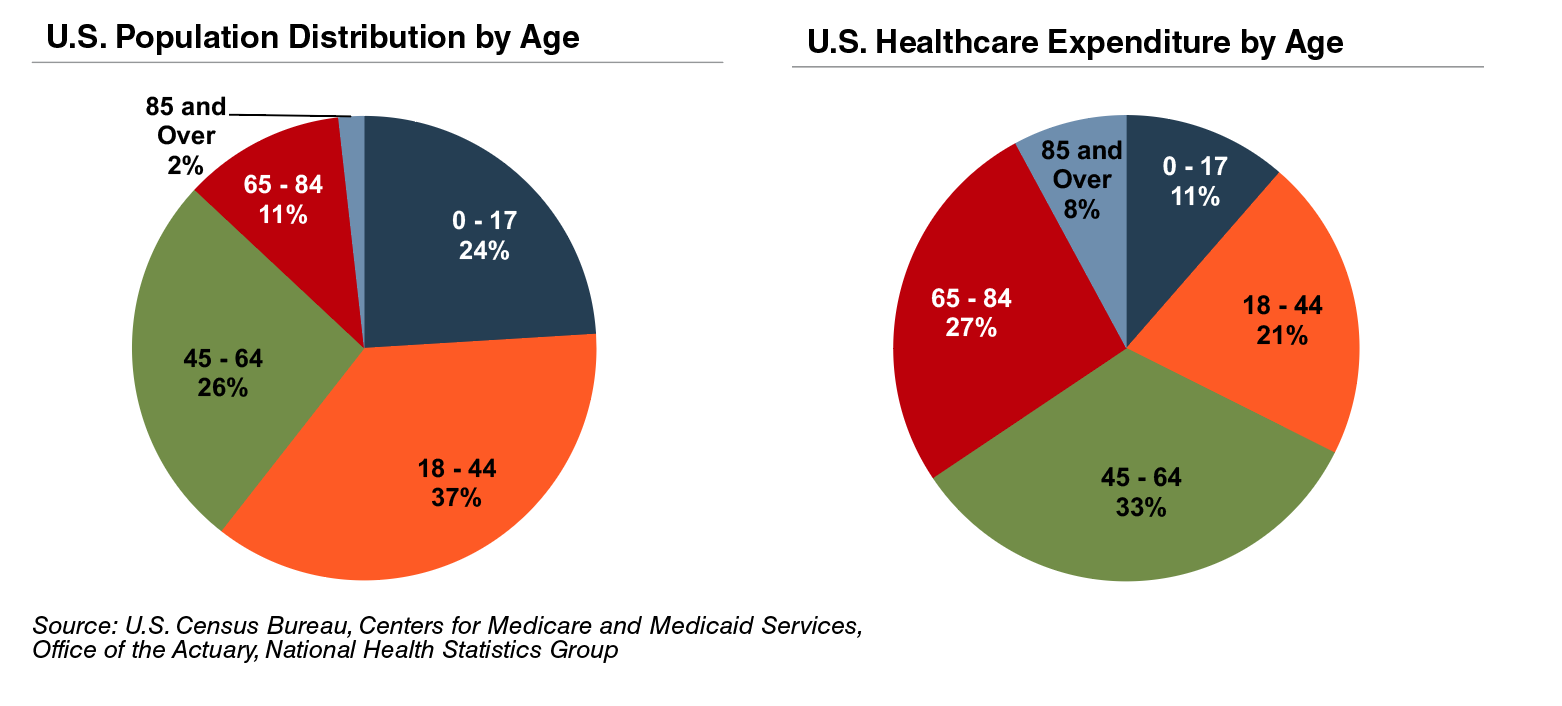

The aging population, driven by declining fertility rates and increasing life expectancy, represents a major demand driver for medical devices. The U.S. elderly population (persons aged 65 and above) totaled 40.3 million in 2021 (13% of the population). The U.S. Census Bureau estimates that the elderly will more than double by 2060 to 95 million, representing 23% of the total population.

The elderly account for nearly one third of total healthcare consumption in the U.S. Personal healthcare spending for the population segment was approximately $19,000 per person in 2014, five times the spending per child (about $3,700) and almost triple the spending per working-age person (about $7,200).

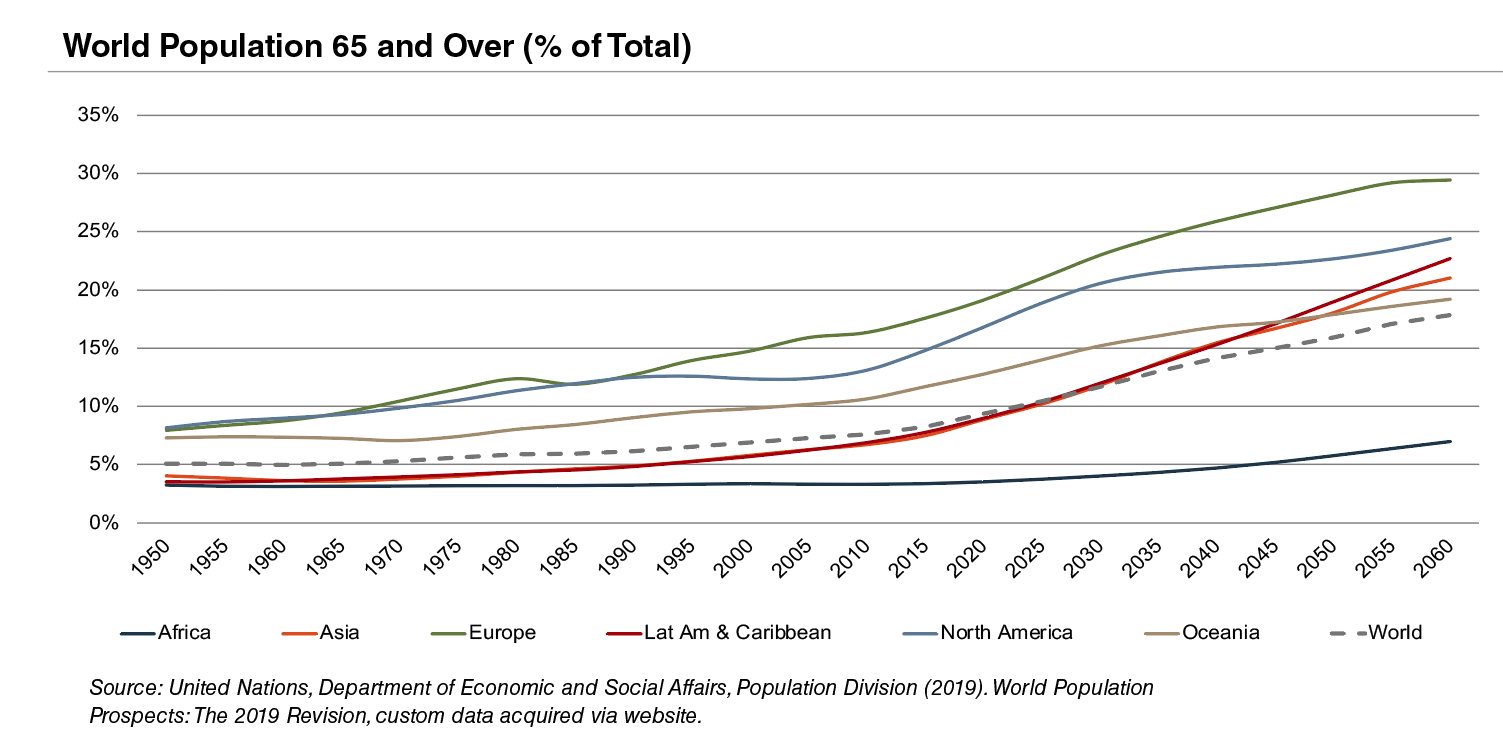

According to United Nations projections, the global elderly population will rise from approximately 608 million (8.2% of world population) in 2015 to 1.8 billion (17.8% of world population) in 2060. Europe’s elderly are projected to reach approximately 29% of the population by 2060, making it the world’s oldest region. While Latin America and Asia are currently relatively young, these regions are expected to undergo drastic transformations over the next several decades, with the elderly population expected to expand from approximately 8% in 2015 to more than 21% of the total population by 2060.

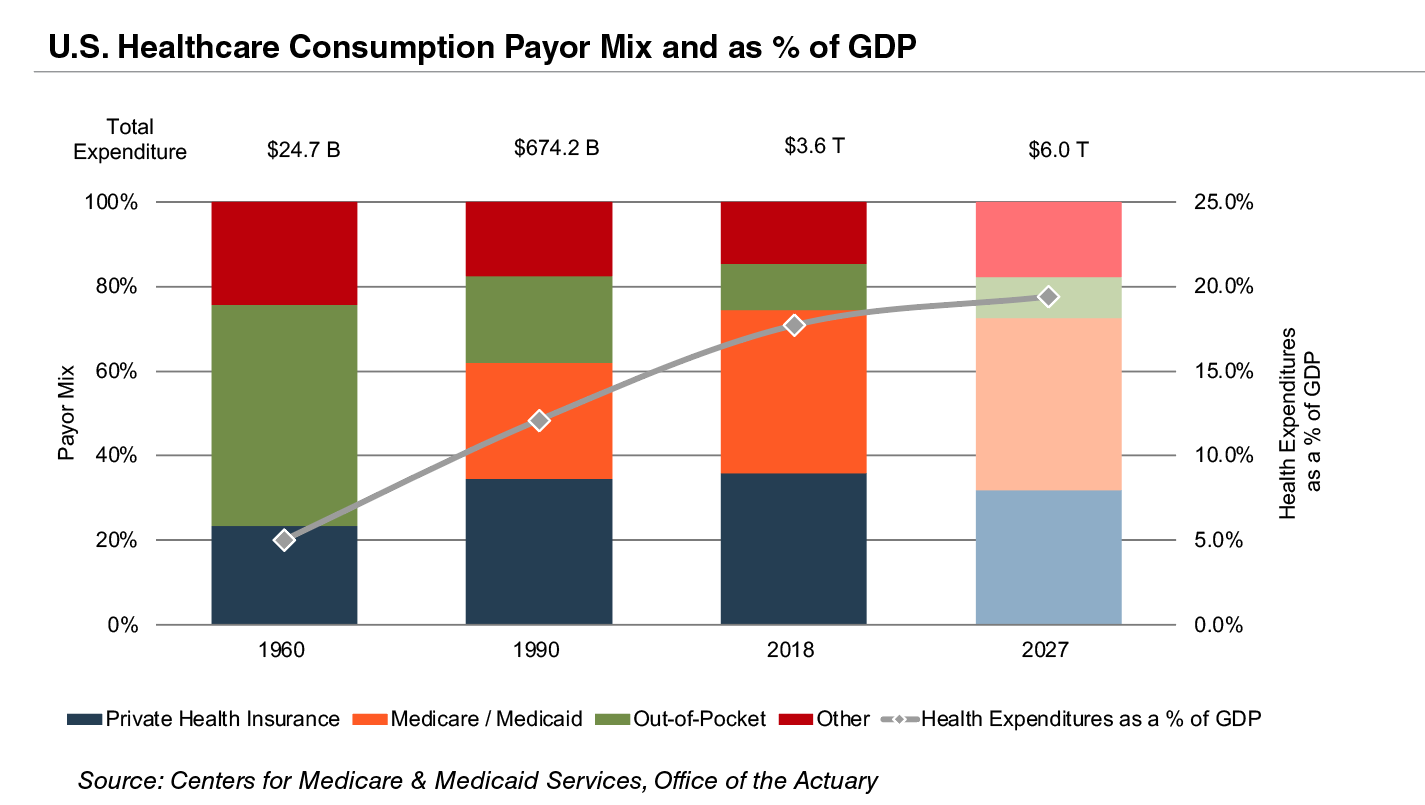

Demographic shifts underlie the expected growth in total U.S. healthcare expenditure from $4.1 trillion in 2020 to $6.2 trillion in 2028, an average annual growth rate of 5.4%. This projected average annual growth rate is faster than the observed rate of 3.9% between 2009 and 2018. Projected growth in annual spending for Medicare (4.3%) and Medicaid (5.6%) is expected to contribute substantially to the increase in national health expenditure over the coming decade. However, growth in national healthcare spending has slowed in 2021 to 4.2%, down from 9.7% in 2020. Healthcare spending as a percentage of GDP is expected to remain virtually unchanged from 19.7% in 2020 to 19.6% by 2030.

Since inception, Medicare has accounted for an increasing proportion of total U.S. healthcare expenditures. Medicare currently provides healthcare benefits for an estimated 60 million elderly and disabled people, constituting approximately 15% of the federal budget in 2018 and is expected to rise to 18% by 2028. Medicare represents the largest portion of total healthcare costs, constituting 20% of total health spending in 2020. Medicare also accounts for 25% of hospital spending, 30% of retail prescription drugs sales, and 23% of physician services.

Due to the growing influence of Medicare in aggregate healthcare consumption, legislative developments can have a potentially outsized effect on the demand and pricing for medical products and services. Net mandatory benefit outlays (gross outlays less offsetting receipts) to Medicare totaled $776 billion in 2020 and are expected to reach $1.5 trillion by 2030.

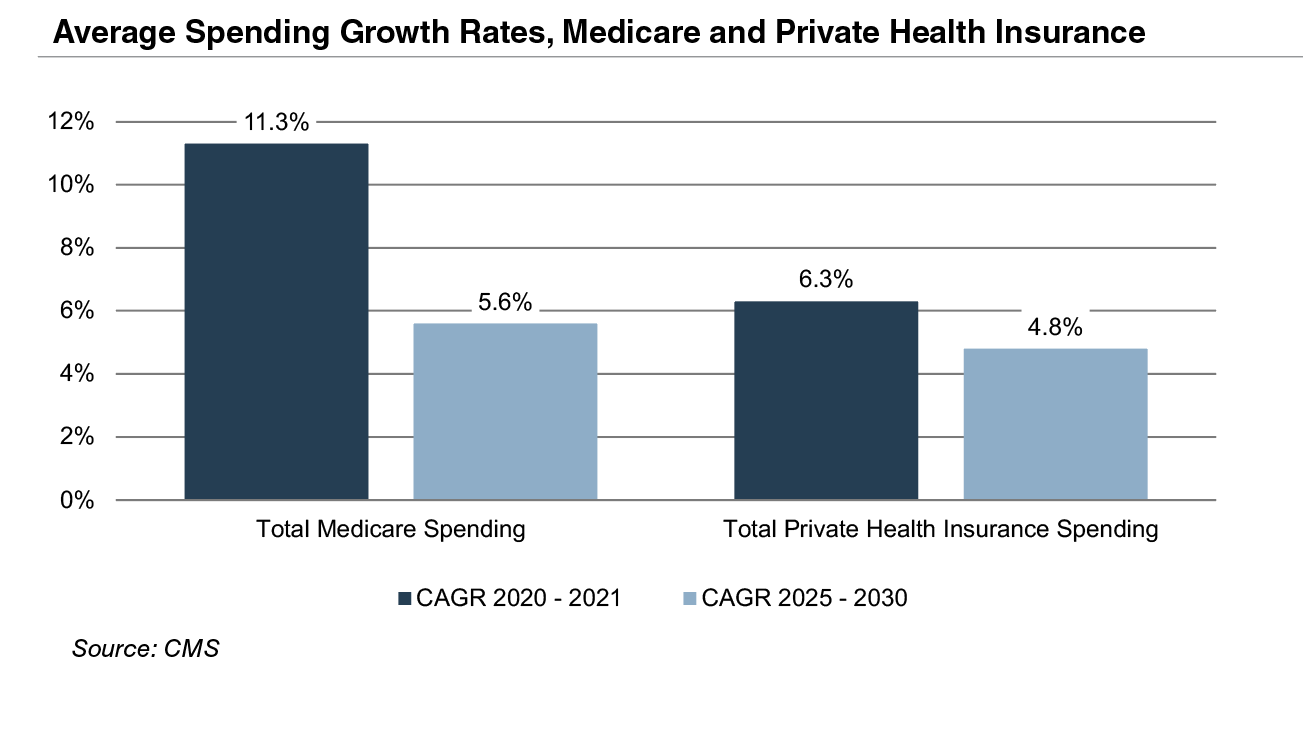

The Patient Protection and Affordable Care Act (“ACA”) of 2010 incorporated changes that are expected to constrain annual growth in Medicare spending over the next several decades, including reductions in Medicare payments to plans and providers, increased revenues, and new delivery system reforms that aim to improve efficiency and quality of patient care and reduce costs. While political debate centered around altering the ACA has been a continuous fixture in American politics since its passing, it is unlikely that material reform to the ACA occurs in the near future under the Biden Administration. Total Medicare spending is projected to grow at 5.6% annually between 2025 and 2030, compared to year over year growth of 11.3% in 2021 and 3.5% in 2020.

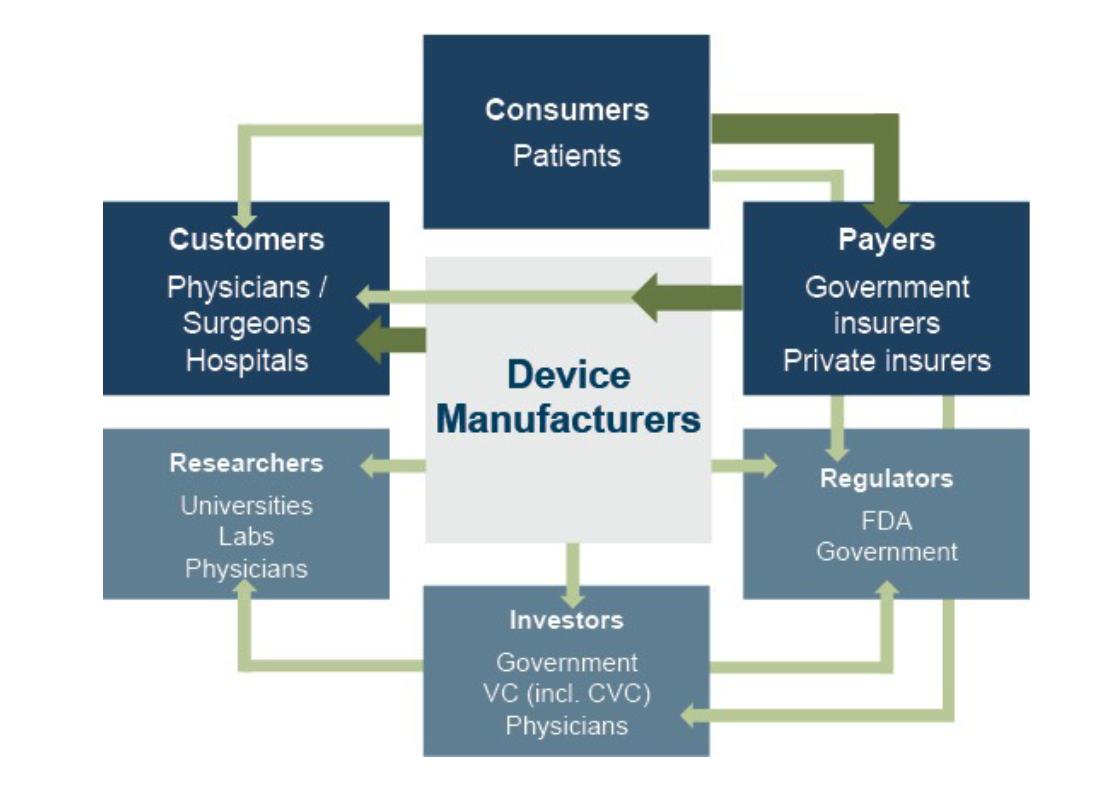

The primary customers of medical device companies are physicians (and/or product approval committees at their hospitals), who select the appropriate equipment for consumers (patients). In most developed economies, the consumers themselves are one (or more) step removed from interactions with manufacturers, and therefore pricing of medical devices. Device manufacturers ultimately receive payments from insurers, who usually reimburse healthcare providers for routine procedures (rather than for specific components like the devices used). Accordingly, medical device purchasing decisions tend to be largely disconnected from price.

Third-party payors (both private and government programs) are keen to reevaluate their payment policies to constrain rising healthcare costs. Several elements of the ACA are expected to limit reimbursement growth for hospitals, which form the largest market for medical devices. Lower reimbursement growth will likely persuade hospitals to scrutinize medical purchases by adopting i) higher standards to evaluate the benefits of new procedures and devices, and ii) a more disciplined price bargaining stance.

The transition of the healthcare delivery paradigm from fee-for-service (FFS) to value models is expected to lead to fewer hospital admissions and procedures, given the focus on cost-cutting and efficiency. In 2015, the Department of Health and Human Services (HHS) announced goals to have 85% and 90% of all Medicare payments tied to quality or value by 2016 and 2018, respectively, and 30% and 50% of total Medicare payments tied to alternative payment models (APM) by the end of 2016 and 2018, respectively. A report issued by the Health Care Payment Learning & Action Network (LAN), a public-private partnership launched in March 2015 by HHS, found that 35.8% of payments were tied to Category 3 and 4 APMs in 2018, compared to 32.8% in 2017.

In 2020, CMS released guidance for states on how to advance value-based care across their healthcare systems, emphasizing Medicaid populations, and to share pathways for adoption of such approaches. Ultimately, lower reimbursement rates and reduced procedure volume will likely limit pricing gains for medical devices and equipment.

The medical device industry faces similar reimbursement issues globally, as the EU and other jurisdictions face similar increasing healthcare costs. A number of countries have instituted price ceilings on certain medical procedures, which could deflate the reimbursement rates of third-party payors, forcing down product prices. Industry participants are required to report manufacturing costs, and medical device reimbursement rates are set potentially below those figures in certain major markets like Germany, France, Japan, Taiwan, Korea, China, and Brazil. Whether third-party payors consider certain devices medically reasonable or necessary for operations presents a hurdle that device makers and manufacturers must overcome in bringing their devices to market.

Historically, much of the growth of medical technology companies has been predicated on continual product innovations that make devices easier for doctors to use and improve health outcomes for the patients. Successful product development usually requires significant R&D outlays and a measure of luck. If viable, new devices can elevate average selling prices, market penetration, and market share.

Government regulations curb competition in two ways to foster an environment where firms may realize an acceptable level of returns on their R&D investments. First, firms that are first to the market with a new product can benefit from patents and intellectual property protection giving them a competitive advantage for a finite period. Second, regulations govern medical device design and development, preclinical and clinical testing, premarket clearance or approval, registration and listing, manufacturing, labeling, storage, advertising and promotions, sales and distribution, export and import, and post market surveillance.

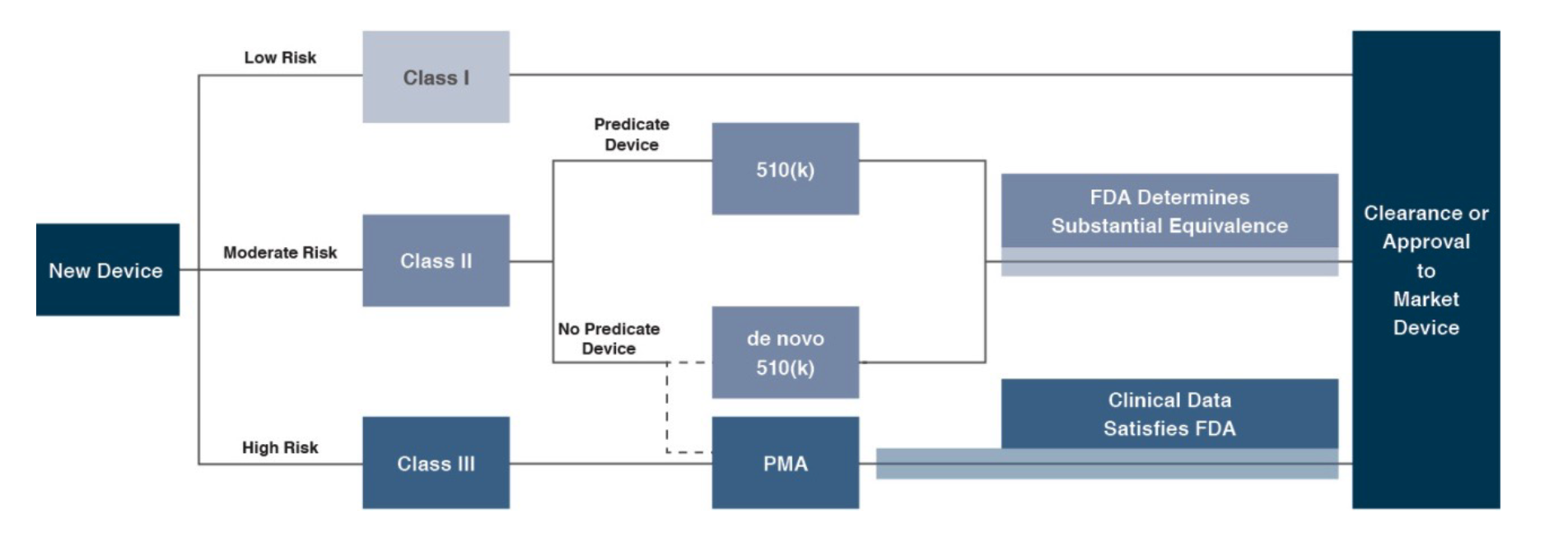

In the U.S., the FDA generally oversees the implementation of the second set of regulations. Some relatively simple devices deemed to pose low risk are exempt from the FDA’s clearance requirement and can be marketed in the US without prior authorization. For the remaining devices, commercial distribution requires marketing authorization from the FDA, which comes in primarily two flavors.

The premarket notification (“510(k) clearance”) process requires the manufacturer to demonstrate that a device is “substantially equivalent” to an existing device (“predicate device”) that is legally marketed in the U.S. The 510(k) clearance process may occasionally require clinical data and generally takes between 90 days and one year for completion. In November 2018, the FDA announced plans to change elements of the 510(k) clearance process. Specifically, the FDA plan includes measures to encourage device manufacturers to use predicate devices that have been on the market for no more than 10 years. In early 2019, the FDA announced an alternative 510(k) program to allow medical devices an easier approval process for manufacturers of certain “well-understood device types” to demonstrate substantial equivalence through objective safety and performance criteria. The plans materialized as the Abbreviated 510(k) Program later in the year.

The premarket approval (“PMA”) process is more stringent, time-consuming, and expensive. A PMA application must be supported by valid scientific evidence, which typically entails collection of extensive technical, preclinical, clinical, and manufacturing data. Once the PMA is submitted and found to be complete, the FDA begins an in-depth review, which is required by statute to take no longer than 180 days. However, the process typically takes significantly longer and may require several years to complete.

Pursuant to the Medical Device User Fee Modernization Act (MDUFA), the FDA collects user fees for the review of devices for marketing clearance or approval. The current iteration of the Medical Device User Fee Act (MDUFA IV) came into effect in October 2017. Under MDUFA IV, the FDA is authorized to collect almost $1 billion in user fees, an increase of more than $320 million over MDUFA III, between 2017 and 2022. Intended to begin in 2020, negotiations for MDUFA V were delayed due to the COVID-19 pandemic. The FDA and industry groups reached a deal for MDUFA V, slated to go into effect beginning fiscal 2023, which would generate up to $1.9 billion in fees to the agency over five years. The U.S. House of Representatives passed MDUFA V in June 2022 and the Senate is expected to follow suit by September 2022.

The European Union (EU), along with countries such as Japan, Canada, and Australia all operate strict regulatory regimes similar to that of the FDA, and international consensus is moving towards more stringent regulations. Stricter regulations for new devices may slow release dates and may negatively affect companies within the industry.

Medical device manufacturers face a single regulatory body across the EU. In order for a medical device to be allowed on the market, it must meet the requirements set by the EU Medical Devices Directive. Devices must receive a Conformité Européenne (CE) Mark certificate before they are allowed to be sold in that market. This CE marking verifies that a device meets all regulatory requirements, including EU safety standards. A set of different directives apply to different types of devices, potentially increasing the complexity and cost of compliance.

Emerging economies are claiming a growing share of global healthcare consumption, including medical devices and related procedures, owing to relative economic prosperity, growing medical awareness, and increasing (and increasingly aging) populations. According to the WHO, middle income countries, such as Russia, China, Turkey, and Peru, among others, are rapidly converging towards outsized levels of spending as their incomes increase. When countries grow richer, the demand for health care increases along with people’s expectation for government financed healthcare. Middle income country share, the fastest growing economic sector, increased from 15% to 19% of global spending between 2000 and 2017. As global health expenditure continues to increase, sales to countries outside the U.S. represent a potential avenue for growth for domestic medical device companies. According to the World Bank, all regions (except Sub-Saharan Africa and South Asia) have seen an increase in healthcare spending as a percentage of total output over the last two decades.

Global medical device sales are estimated to increase 5.4% annually from 2021 to 2028, reaching nearly $658 billion according to data from Fortune Business Insights. While the Americas are projected to remain the world’s largest medical device market, the Asia Pacific and Western Europe markets are expected to expand at a quicker pace over the next several years.

Demographic shifts underlie the long-term market opportunity for medical device manufacturers. While efforts to control costs on the part of the government insurer in the U.S. may limit future pricing growth for incumbent products, a growing global market provides domestic device manufacturers with an opportunity to broaden and diversify their geographic revenue base. Developing new products and procedures is risky and usually more resource intensive compared to some other growth sectors of the economy. However, barriers to entry in the form of existing regulations provide a measure of relief from competition, especially for

newly developed products.

The COVID-19 pandemic brought economic hardship to many. The second quarter of 2020 might go down as one of the quickest economic downturns ever recorded. However, in an effort to protect the economy, the Fed created an extremely hospitable environment for venture capital, and with the glaring supply chain issues, FreightTech became a cushy landing place for investor’s money. We have written about venture capital and FreightTech before, and it has only gotten bigger since then.

In the fourth quarter of 2020, American and European FreightTech companies raised a combined $4.1 billion from venture capitalists. This was a 21% increase quarter-over-quarter, and an increase of 49% on an annual basis. In less than twelve months, 2020 went from a dark and gloomy place for businesses to a 4th of July fireworks parade, during which $12.6 billion was poured into 555 deals in America and Europe.

The parade continued marching into 2021, with average pre-money valuations increasing by 28.4% to $30 million, and late-stage valuations increasing by 95.3% to $120 million. During these six quarters, companies like Loadsmith continued to introduce digital technologies that seek to revolutionize the brokerage industry and allow smaller brokerages and 3PLs to compete with the largest asset-based carriers.

Click here to expand the image above

Self-driving trucks have also remained a point of focus. Though one of our clients maintains that self-driving trucks are “always ten years away,” they are the holy grail of FreightTech. The trucking industry has long struggled with an exodus of workers, and during COVID a large portion of its aging labor force decided to either retire due to fears of contracting the virus or moved on to less-regulated sectors. To prevent driver shortages and reduce turnover, many companies are increasing driver pay. For example, Walmart began paying their drivers $110,000 in their first year. With a fleet of 12,000 drivers, that is a very expensive endeavor, so it is no surprise that companies like TuSimple, that develop self-driving trucks, already have deals in place with ready-to-pay customers. The CEO of Werner Enterprises was quoted as saying that “We look forward to building a hybrid world where drivers continue to haul freight while autonomous trucks supplement rising demand,” showing that self-driving freight modes are no longer only a fantasy of Silicon Valley, but a future of the industry.

Despite all the positive growth between the third quarter of 2020 and the fourth quarter of 2021, the proverbial truck ran into a roadblock. As the Federal Reserve increased interest rates in its efforts to tame inflation, the first quarter of 2022 recorded decreases of 3.6% and 20.4% on a quarterly and annual basis, respectively. Startups raised only $14 billion. The number of IPO listings decreased dramatically, alongside the average valuations of FreightTech firms.