Key Takeaways

The Permian Basin continued to increase production despite a decline in active rig counts, demonstrating ongoing gains in drilling efficiency, capital discipline, and operational productivity.

Commodity markets experienced heightened volatility due to weather events, changing natural gas fundamentals, and geopolitical tensions, particularly during the latter portion of the review period.

Strong operational performance and resilient commodity prices supported solid stock price appreciation for Permian-focused public companies, reinforcing the basin's leadership among U.S. oil-producing regions.

The economics of oil and gas production vary by region. Mercer Capital focuses on trends in the Permian, Eagle Ford, Haynesville, and Marcellus and Utica plays. The cost of producing oil and gas depends on the geological makeup of the reserve, the depth of the reserve, and the cost of transporting the raw crude to market. We can observe different costs in different regions depending on these factors. In this post, we take a closer look at the Permian.

Production and Activity Levels

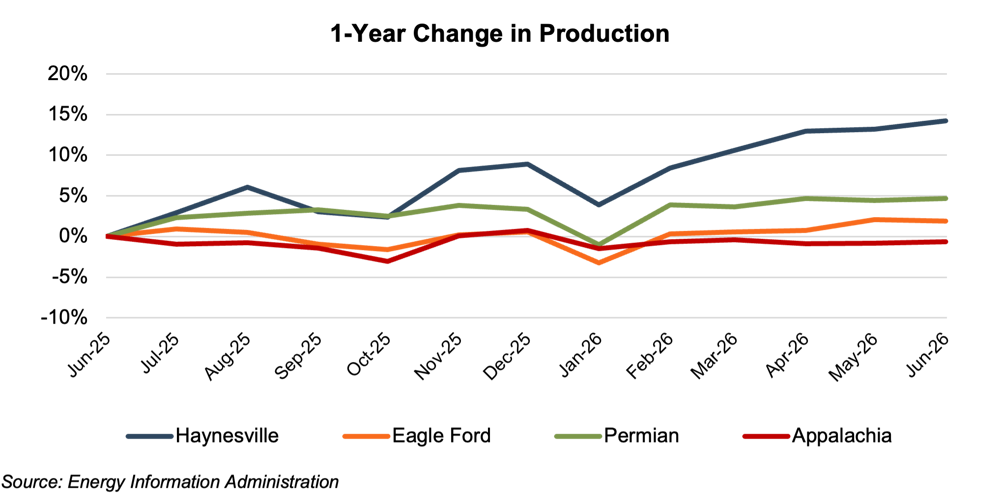

Permian production (on a barrels of oil equivalent, or “boe” basis) increased 4.7% year-over-year (YoY) through June 2026, rising from 11.1 mmboe/d in June 2025 to 11.7 mmboe/d in June 2026. Production in the nation's most prolific basin posted relatively steady gains through the second half of 2025 before dipping modestly in January 2026 to 11.0 mmboe/d, due in part to winter weather that temporarily disrupted oil and gas operations across West Texas. Production recovered in February to 11.6 mmboe/d and remained generally stable through June 2026, averaging 11.6 mmboe/d and ending the review period at 11.7 mmboe/d.

The Permian posted the second-highest YoY production growth among the four basins covered, trailing only the Haynesville. Haynesville production increased a very strong 14.3% YoY, rising from 2.4 mmboe/d in June 2025 to 2.8 mmboe/d in June 2026. Although Haynesville production fluctuated during the first seven months of the review period, it increased steadily from February through June 2026, reaching its highest level at the end of the review period. The stronger production growth during the final five months of the review period was driven largely by improving natural gas prices, increased drilling activity, and continued development in anticipation of expanding Gulf Coast LNG export capacity. The Eagle Ford posted a modest 1.9% increase while Appalachia posted the only decline at -0.6%.

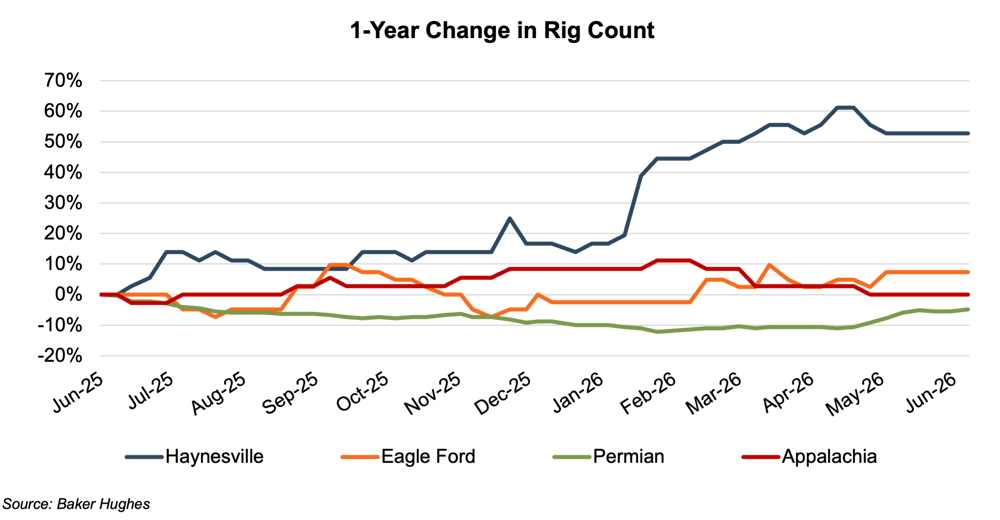

The Permian posted the only YoY decline in rig count among the four basins covered, ending the review period with 258 active rigs, down 5.0% from 271 rigs in June 2025. Permian rig activity declined gradually through February 2026 before recovering modestly over the remainder of the review period. The relatively modest decline in Permian rig activity reflects continued capital discipline among operators, who remained focused on drilling efficiencies, productivity improvements, and shareholder returns while sustaining production growth with fewer active rigs.

The Haynesville posted by far the strongest YoY rig count growth, increasing 53% from 36 active rigs in June 2025 to 55 rigs in June 2026. The increase in Haynesville drilling activity reflected improving drilling economics supported by expectations for stronger natural gas demand from expanding Gulf Coast LNG export capacity, together with an improved natural gas price outlook. The Eagle Ford posted a modest 7.3% YoY increase, while Appalachia remained stable throughout the review period.

Commodity Prices

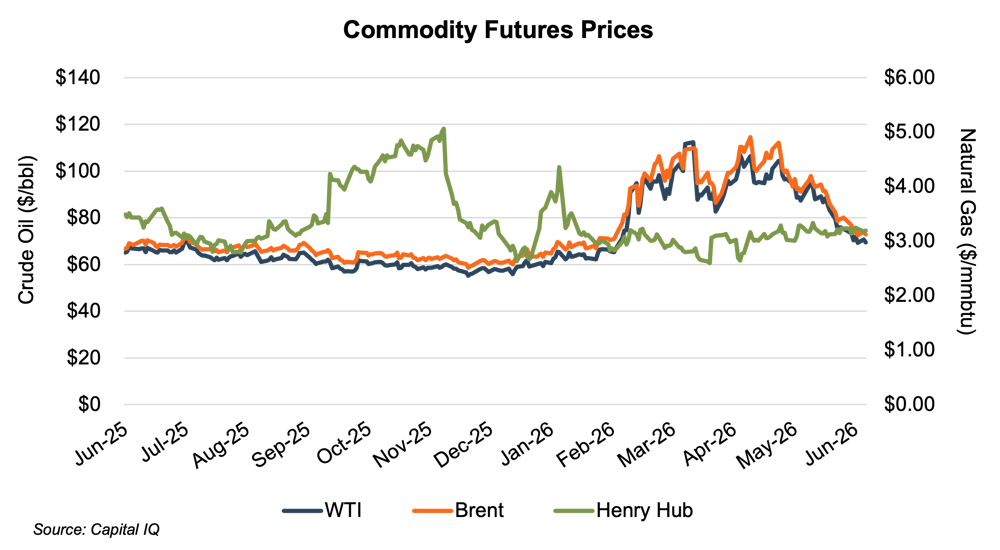

Oil prices, represented by the WTI and Brent benchmarks, declined gradually during the first half of the review period before recovering sharply in early 2026. Prices surged following U.S. military strikes on Iran that raised concerns over potential disruptions to crude oil shipments through the Strait of Hormuz. Oil prices remained considerably more volatile through the balance of the review period as geopolitical tensions influenced market expectations.

Natural gas pricing, represented by the Henry Hub benchmark, displayed its typical seasonal volatility during the review period. Prices rose in late 2025 due to weather-driven demand, a polar vortex event, and increasing LNG export demand before declining sharply as winter weather expectations shifted. Winter Storm Fern briefly lifted prices in late January, after which Henry Hub traded within a relatively narrow range through June 2026. The EIA noted that relatively high natural gas inventories helped limit price volatility during the latter portion of the review period.

Financial Performance

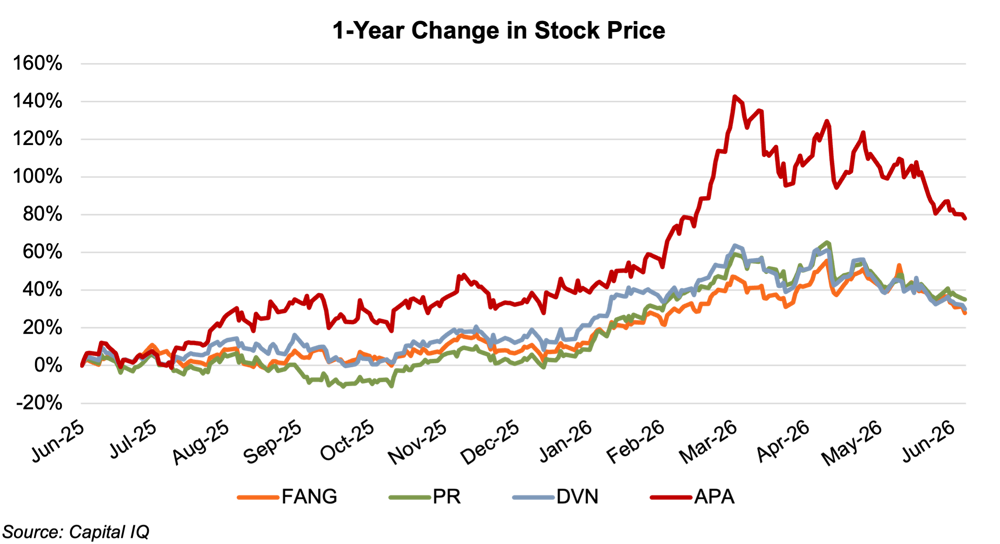

The Permian public company group posted strong one-year stock price performance through June 2026, with gains ranging from 28% to 78%. Diamondback Energy (FANG), Permian Resources (PR), and Devon Energy (DVN) posted relatively consistent gains, while APA Corporation (APA) substantially outperformed the group. APA's stronger performance likely reflected the greater proportion of its equity value attributable to future production growth and development projects, particularly GranMorgu offshore Suriname, compared to peers whose valuations are more heavily supported by existing producing assets and current operating cash flows.

Share prices for the Permian peer group generally traded within a relatively narrow range during the first half of the review period before volatility increased alongside rising geopolitical tensions and higher oil price volatility.

Conclusion

The Permian Basin continued to demonstrate its resilience through the latest review period. Despite a modest decline in rig counts, production reached new highs as operators continued to emphasize capital discipline, drilling efficiencies, and productivity improvements. Heightened geopolitical tensions introduced greater commodity price volatility during the latter portion of the review period, yet oil prices ended above year-earlier levels and Permian public companies posted strong stock price appreciation. The basin remains the nation's premier oil-producing region and continues to demonstrate its ability to adapt to changing market conditions.

Mercer Capital has assisted clients with a wide range of valuation needs in the upstream oil and gas industry across both conventional and unconventional plays in North America and around the world. Contact a Mercer Capital professional to discuss your valuation needs in confidence.