Key Takeaways

M&A activity in the Eagle Ford Shale has remained subdued through early 2026, reflecting a broader trend of limited deal volume driven by basin maturity, scarce high-quality inventory, and disciplined capital allocation.

The few notable transactions, such as Crescent Energy’s acquisition of Ridgemar and ongoing divestiture processes by ExxonMobil and Baytex highlight a market shaped by portfolio optimization and selective consolidation rather than aggressive expansion.

Structural factors including competition from the Permian Basin, commodity price volatility, and limited scalable assets continue to constrain transaction activity, resulting in a more opportunistic and measured M&A environment.

Eagle Ford Shale M&A Update

Overview

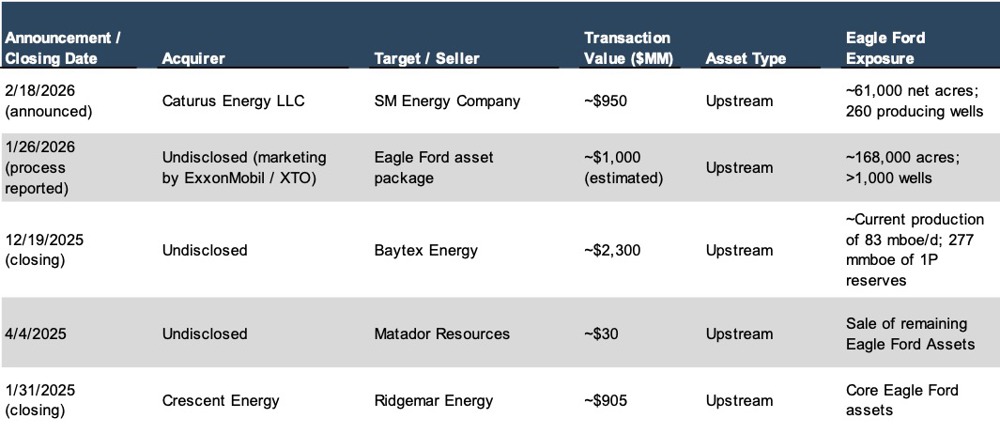

M&A activity in the Eagle Ford Shale during the January 2025 through March 2026 remained muted relative to other U.S. shale basins, continuing a multi-year trend of limited transaction volume. A 2024-2025 analysis by Mercer Capital noted that only two “pure-play” Eagle Ford transactions closed in the prior twelve-month period.

While the basin remains a prolific hydrocarbon system with established infrastructure and proximity to Gulf Coast markets, transaction flow has been constrained by increasing scarcity in quality shale inventory, portfolio high-grading by operators, and competition from the Permian Basin. In addition, the increasing emphasis on capital discipline and shareholder returns across the upstream sector has further tempered acquisitive behavior, with operators prioritizing free cash flow generation, debt reduction, and share repurchases over large-scale expansion. This shift in corporate strategy has contributed to a more measured pace of consolidation within the Eagle Ford relative to earlier development cycles.

Transaction Activity (January 2025 - March 2026)

Transaction activity over the review period was limited, with only one clearly identifiable pure-play Eagle Ford acquisition, supplemented by corporate-level transactions and asset marketing processes that include Eagle Ford exposure. As a result, observable transaction data remains sparse, limiting the availability of directly comparable valuation benchmarks and reinforcing the importance of asset-specific analysis in underwriting potential acquisitions.

Key Transactions

Crescent Energy – Ridgemar Energy

Crescent Energy completed the acquisition of Ridgemar Energy’s Eagle Ford assets for approximately $905 million, expanding its oil-weighted production base and drilling inventory. This transaction represents the primary datapoint for Eagle Ford-specific valuation within the review period and reflects continued consolidation among mid-cap operators. The acquisition also highlights the strategic focus on contiguous acreage positions and operational synergies, as buyers seek to enhance capital efficiency through longer laterals, optimized development spacing, and reduced per-unit costs.

ExxonMobil (XTO Energy) - Eagle Ford Divestiture Process

In early 2026, ExxonMobil initiated a process to market a large Eagle Ford position, estimated at approximately $1 billion. Although not yet completed, this process is indicative of:

Portfolio high-grading by major operators

Increasing availability of mature Eagle Ford assets

Potential for incremental deal flow in subsequent periods

Should the process result in a completed transaction, it may provide additional insight into current market-clearing valuation levels for mature, large-scale Eagle Ford positions.

Baytex Energy - Eagle Ford Divestiture Process

In November 2025, Baytex Energy entered into a definitive agreement to sell its entire U.S. Eagle Ford asset base for approximately $2.305 billion in cash to an undisclosed buyer, with closing expected in December 2025. The transaction represents a full exit from the Eagle Ford and U.S. operations, reversing Baytex’s prior expansion into the basin through the 2023 Ranger Oil acquisition. Strategically, the divestiture is framed as a portfolio high-grading initiative, with proceeds expected to materially strengthen the balance sheet, including repayment of outstanding debt and a transition to a net cash position, while supporting increased shareholder returns through buybacks and dividends.

Market Dynamics Impacting M&A

Transaction activity in the Eagle Ford over the review period reflects a convergence of structural and cyclical factors that continue to suppress deal flow. As a mature basin with a largely consolidated operator base, the Eagle Ford offers fewer scalable acquisition targets relative to earlier development phases. At the same time, macroeconomic pressures, including commodity price uncertainty and capital discipline among upstream operators, have contributed to wider bid-ask spreads and reduced transaction velocity. These dynamics, combined with competition for capital from higher-return basins, have resulted in a market environment characterized by selective, opportunistic transactions rather than broad-based M&A activity.

Limited Inventory of Scalable Assets

The Eagle Ford is a mature basin, and prior consolidation has reduced the number of sizable, high-quality acquisition opportunities. Remaining opportunities are often fragmented or require operational turnaround, limiting the pool of buyers with both the technical expertise and financial flexibility to execute acquisitions at scale.

Commodity Price Volatility

Lower and more volatile oil prices in 2025 contributed to wider bid-ask spreads, slowing transaction execution. Uncertainty around forward price expectations has further complicated underwriting assumptions, particularly for assets with higher decline rates or limited remaining inventory.

Capital Allocation to Higher-Return Basins

The Permian Basin continues to attract the majority of upstream investment due to superior drilling economics and inventory depth, limiting capital directed toward the Eagle Ford. This relative capital disadvantage has contributed to fewer competitive bidding processes for Eagle Ford assets, particularly when compared to recent Permian transactions.

Strategic Portfolio Optimization

Major operators continue to divest non-core assets, as evidenced by ExxonMobil’s marketing process, while reinvesting in higher-margin opportunities. This trend is expected to persist as companies refine portfolios to emphasize scale, operational efficiency, and returns on invested capital.

Outlook

Looking ahead, Eagle Ford M&A activity is likely to remain selective, with transaction volume dependent on the pace of asset divestitures by larger operators and the willingness of mid-cap buyers to pursue bolt-on acquisitions. While the basin’s maturity constrains large-scale consolidation opportunities, its established infrastructure, favorable market access, and predictable production profiles continue to support its relevance within diversified upstream portfolios. As such, incremental transaction activity is expected to be driven by strategic repositioning rather than broad-based market expansion.