Following several years of balance sheet volatility and margin pressure, the operating environment for banks improved in 2025 as most posted higher earnings on expanded net interest margins. The outlook for 2026, at least prior to the outbreak of the U.S./Israel-Iran war, reflects(ed) a relatively stable operating environment.

Stability, however, introduces a different challenge. Loan growth has moderated across much of the industry, and the benefit from asset repricing has largely been realized. In this environment, earnings growth is less dependent on external tailwinds and more dependent on internal discipline. As a result, capital allocation has moved to the center of strategic decision-making.

The Expanding Capital Allocation Toolkit

Capital allocation discussions are often framed around dividends and, to a lesser extent, share repurchases. In practice, the range of capital deployment decisions is broader and more interconnected. Banks today are balancing:

Organic balance sheet growth

Technology and infrastructure investment

Dividends

Share repurchases

M&A

Balance sheet repositioning

Retained capital for flexibility

Each alternative carries different implications for risk, return, and long-term franchise value.

Organic growth often is the preferred use for internally generated capital when the risk-adjusted returns exceed the cost of equity. However, competitive loan pricing and a tough environment to grow low cost deposits have narrowed spreads, reducing the margin for error. Similarly, technology investments may improve efficiency over time but require upfront capital with uncertain timing of returns.

Returns, Valuation, and Market Discipline

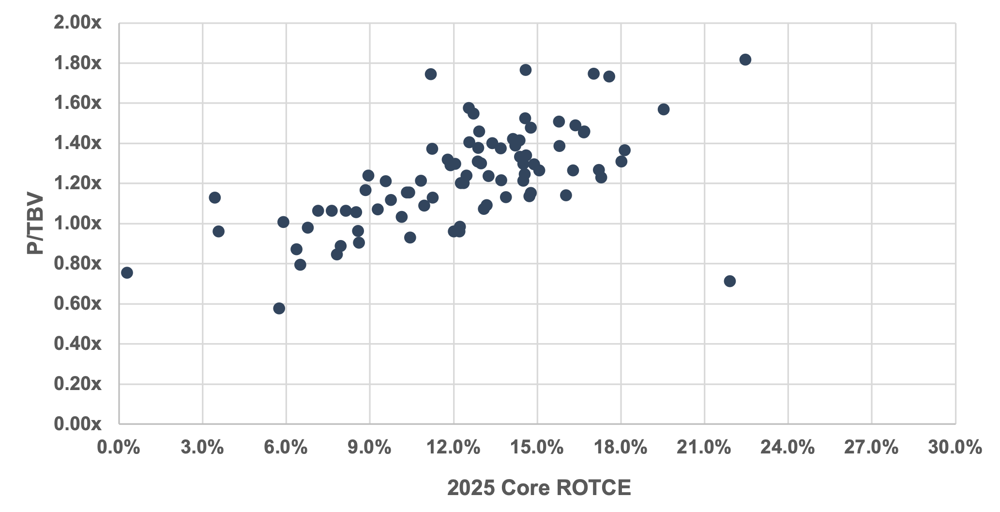

Public market valuations provide a useful lens for evaluating capital allocation decisions. As shown in Figure 1(on the next page), banks that generate higher returns on tangible common equity (ROTCE) tend to command higher price-to-tangible book value multiples. This can also be expressed algebraically, at least on paper, whereby P/E x ROTCE = P/TBV, while P/Es reflect investor assessments about growth and risk.

This relationship reflects a straightforward principle: capital should be deployed where it earns returns in excess of the cost of equity. When internal opportunities meet that threshold, reinvestment should be appropriate. When returns are below the threshold, returning capital to shareholders through special dividends or repurchases may create greater per-share value.

Share repurchases, in particular, can be an effective tool when executed below intrinsic value and when capital levels remain sufficient to support strategic flexibility. However, repurchases that do not improve per-share metrics or are offset by dilution from other sources may have limited impact.

Figure 1: Publicly Traded Banks with Assets $1 to $5 Billion

Balance Sheet Repositioning as Capital Allocation

In some cases, capital allocation decisions are embedded within the balance sheet itself. One example is securities portfolio repositioning.

Many banks continue to hold securities originated during the low-rate environment of 2020 and 2021. While unrealized losses associated with these portfolios have moderated, the yield on these assets often remains well below current market rates.

Repositioning the portfolio, by realizing losses and reinvesting at higher yields, represents a tradeoff between near-term capital impact and longer-term earnings improvement. In effect, this decision can be evaluated similarly to other capital deployment alternatives, with management weighing the upfront reduction in Tier 1 Capital against the expected lift to net interest income and returns over time.

As with M&A, the concept of an “earnback period” can be applied. Institutions that approach repositioning with a clear understanding of the payback dynamics are better positioned to evaluate whether the strategy enhances long-term shareholder value. We offer the caveat that institutions who evaluate restructuring transactions should compare the expected return from realizing losses (i.e., reducing regulatory capital) with instead holding the securities and repurchasing shares. If the bank’s shares are sufficiently cheap, then it could make sense to continue to hold the underwater bonds until the shares rise sufficiently.

M&A and Capital Flexibility

M&A remains a viable capital deployment option, particularly for institutions seeking scale or improved operating efficiency. However, transaction activity continues to be constrained by pricing discipline, tangible book value dilution, and investor expectations around earnback periods.

Public market valuations ultimately serve as a governor on deal pricing, reinforcing the importance of aligning capital deployment decisions with shareholder return expectations.

Conclusion: Discipline Drives Outcomes

In a slower growth environment, capital allocation is not a secondary consideration; it is a core driver of performance. While banks cannot control market multiples, they can control how capital is deployed across competing opportunities.

Institutions that consistently allocate capital with a clear focus on risk-adjusted returns, strategic alignment, and per-share value creation are more likely to generate sustainable growth in earnings and tangible book value. In the current environment, disciplined execution may prove more valuable than more aggressive but less certain alternatives.