Q3 2023: Alts Take the Lead as Other RIAs Lose Traction

Market Uncertainty and Fee Compression Trends Lead Investors to Take an Alternative Approach to RIA Investing

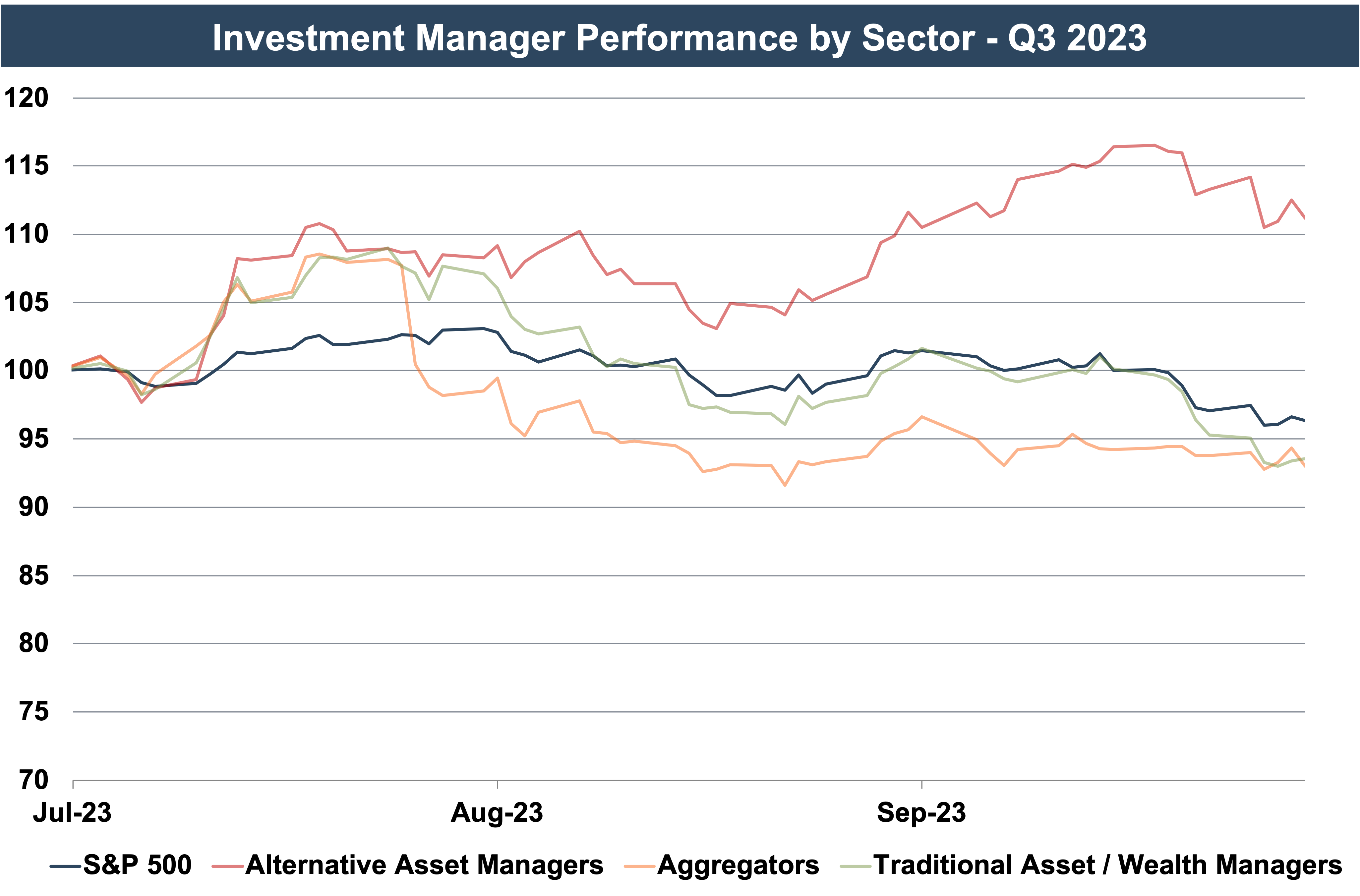

Share prices for most publicly traded asset and wealth management firms trended in line with the steady decrease in the broader market during Q3 2023. Alternative asset managers were a notable exception to this trend, ending the quarter up about 10%. On a year-over-year basis, all categories of RIAs experienced exceptional growth as the markets rebounded from their Q3 2022 trough, which marked the deepest dip since March 2020. RIAs directly benefit from improving market conditions as they result in a stronger asset base on which to collect fees.

Performance by Sector

The market decline in Q3 translated to decreased prices for most public RIAs. Prices for aggregators and traditional asset managers faced a slightly more severe decline than the S&P 500. On the other hand, alternative asset managers experienced an increase in share price of just over 10%. In the last twelve months, most RIA sectors saw a decline in year-over-year earnings and revenue, reflecting the lower average AUM. Market volatility since 2020, which drove volatility in AUM during this period, is one of the factors responsible for the increased demand for alternative asset manager stocks. Private equity funds and other alternative investment vehicles typically lock in assets for ten to twelve years, leading to a more predictable and stable revenue stream that is less correlated with the broader market.

Performance by Size Category

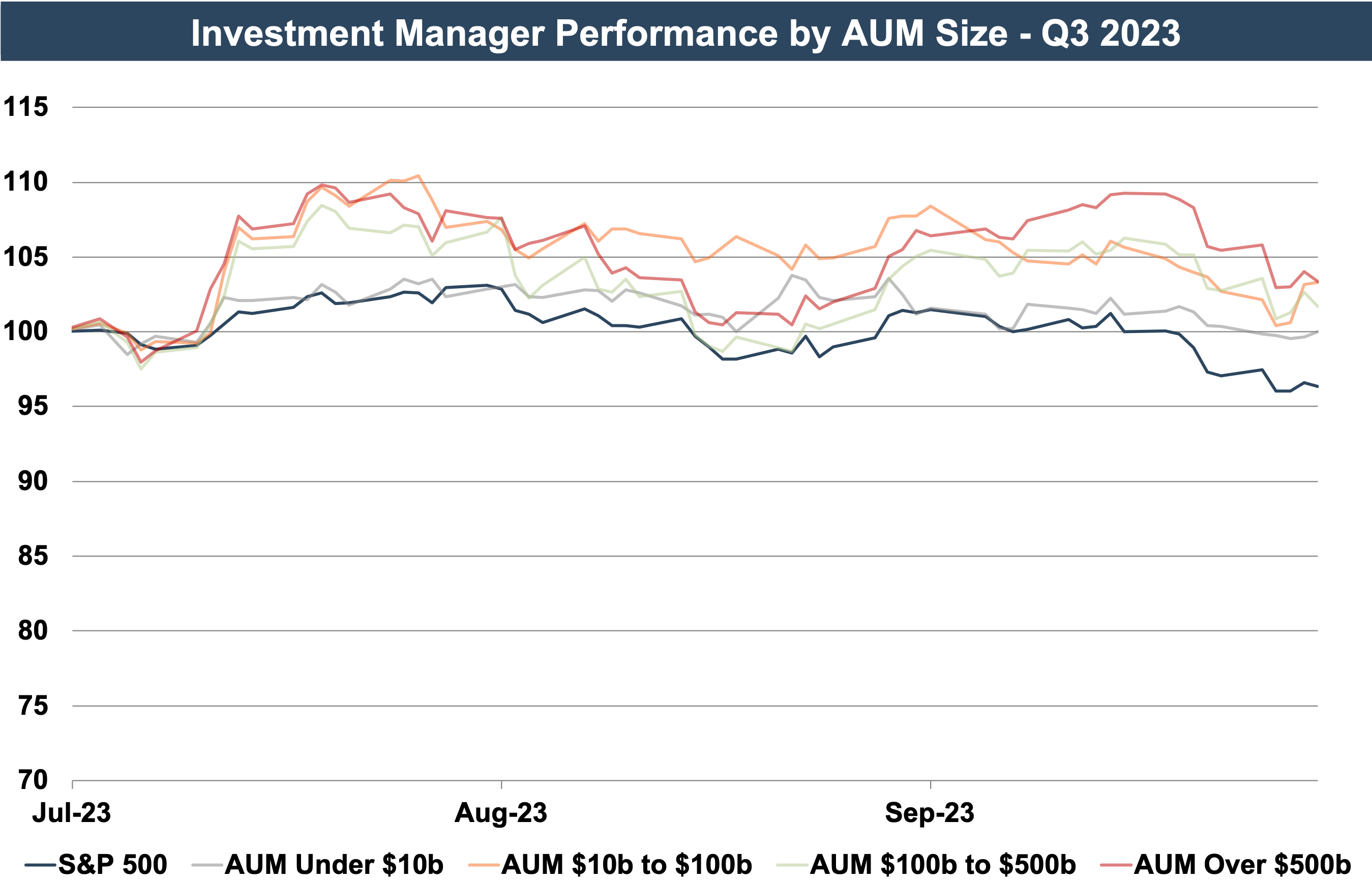

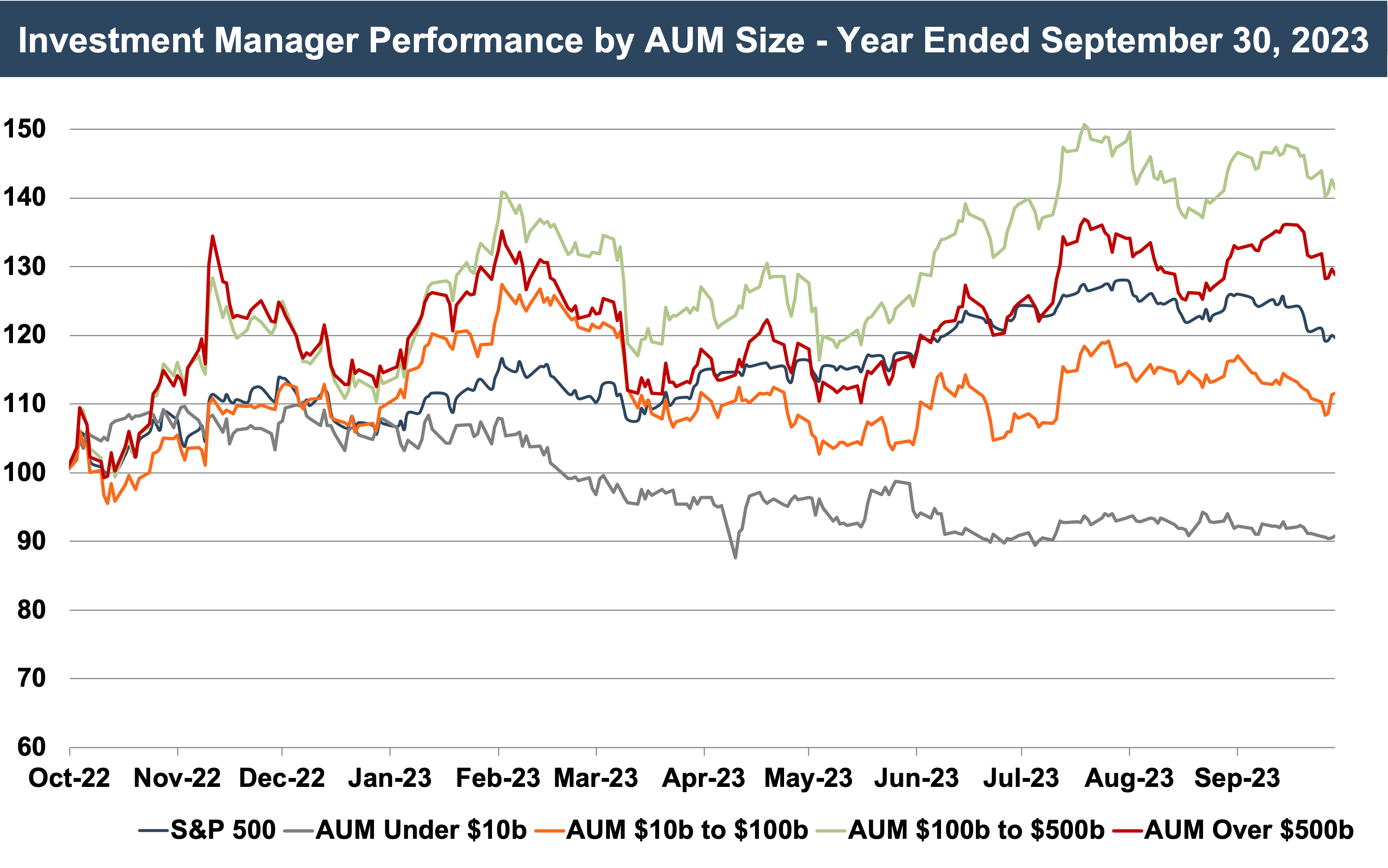

As measured by AUM size, all groups of RIAs outperformed the S&P 500 during Q3. Over the past year, larger RIA (the $100b to $500b and the >$500b AUM groups) outperformed the S&P 500, with smaller RIAs underperforming the S&P. While all AUM size groups outperformed the S&P during Q3, larger asset managers experienced a stronger increase in share price.

Pricing Trends

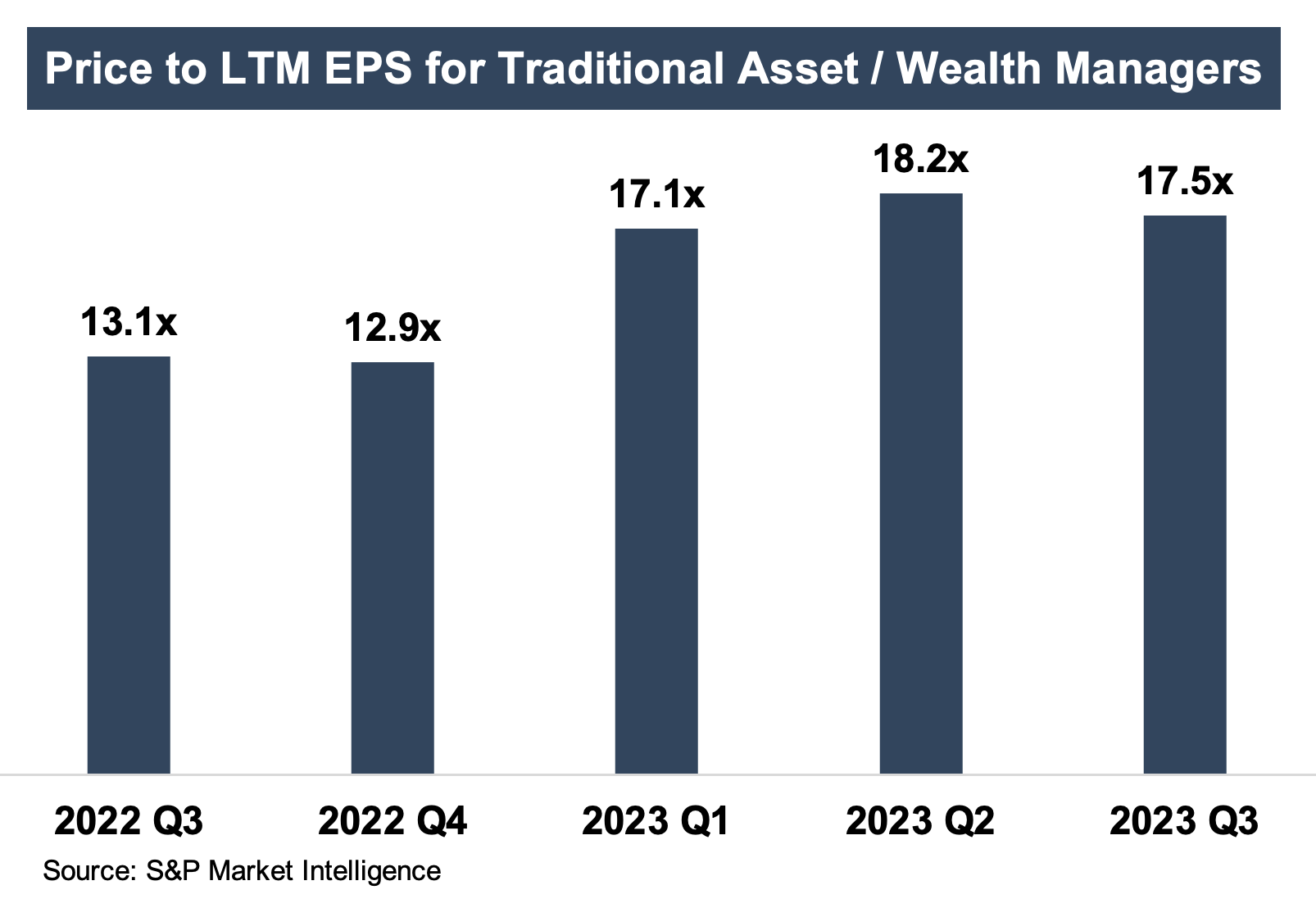

The median LTM earnings multiple for publicly traded asset and wealth management firms decreased 3.8% during the third quarter of 2023, representing the first decrease since Q4 2022. After trending downwards for most of 2022, multiples began to increase during the first half of 2023 as LTM earnings metrics began to fully reflect the impact of 2022 market conditions. The modest multiple decrease in Q3 2023 also reflects the moderating interest rate environment and market decrease during the quarter, translating into slightly lower AUM balances and future earnings power for RIAs.

Implications for Your RIA

The value of public asset and wealth managers provides some perspective on investor sentiment towards the asset class, but strict comparisons with closely held RIAs should be made with caution. Many smaller publics are focused on active asset management, which has been particularly vulnerable to headwinds such as fee pressure and asset outflows to passive products. Many sectors of closely held RIAs, particularly wealth managers and larger public asset managers, have been less impacted by these trends and have seen more resilient multiples as a result. In the case of wealth management firms, strong demand from aggregators has also helped to bolster pricing in recent years. Focusing on the fundamentals of your RIA—compensation structures, cost controls, hiring practices, etc.—may offer protection from arbitrary changes in market multiples.

In our July M&A update, we described the increase in volume of transactions, both in number of firms and AUM transacted. M&A is often viewed as a lagging economic indicator since deals take several months or even quarters to complete. Later this month, we will report on Q3 2023 M&A activity to keep you informed on market trends.

About Mercer Capital

We are a valuation firm that is organized according to industry specialization. Our Investment Management Team provides valuation, transaction, litigation, and consulting services to a client base consisting of asset managers, wealth managers, independent trust companies, broker-dealers, PE firms and alternative managers, and related investment consultancies.