To celebrate a new year and everything that comes with new beginnings, the Mercer Capital Litigation Support Services Team has decided to start the year with a blog emphasizing the importance of the beginning of a family law engagement, defining the assignment.

In an engagement that requires a business valuation, the first step that attorneys and valuation experts should take is to define the assignment. This process involves the following:

While defining the assignment, the Standard of Value is another important consideration. Some simple questions that can help determine the standard of value include: Will the business continue to operate as a going concern or is a liquidation value more appropriate? Is “fair market value” or “fair value” required by the letter of the law for that specific engagement?

There are four standards of value that should be considered when defining a valuation assignment:

Each of these four business valuation standards may result in a different number to represent the value of the business, depending on the circumstances. Selecting the appropriate Standard of Value is crucial, and an experienced business valuation professional should be well-versed in selecting the standard of value that is most appropriate for the subject business interest being valued.

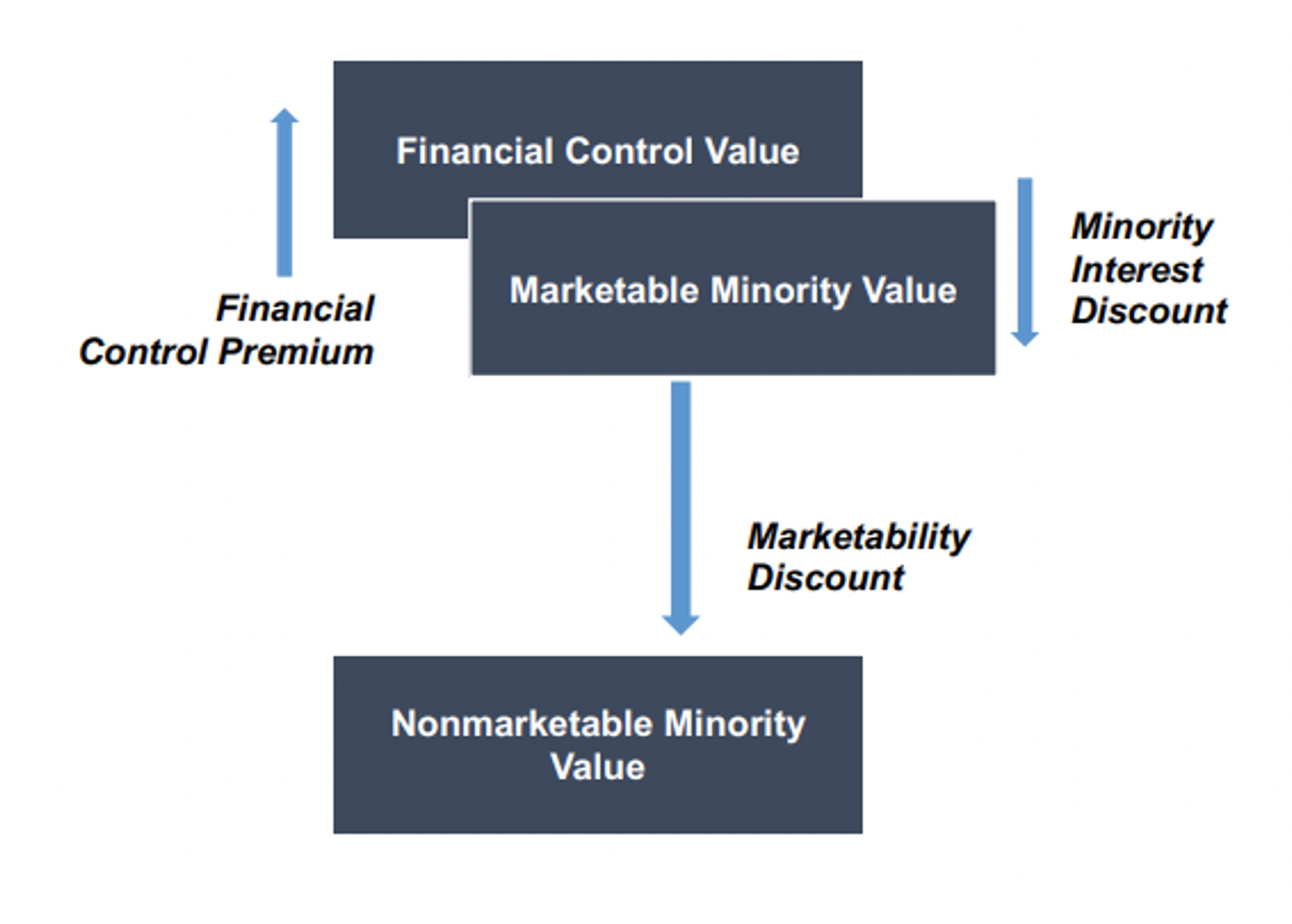

Business appraisers also refer to different kinds of values for businesses and business interests in terms of “levels of value.” As we noted in the Standards of Value section of this blog, the Fair Market Value standard of value opens the door for valuation discounts or premiums to be applied, which means that business appraisers may need to determine the appropriate Level of Value. See the chart below for the different Levels of Value that can be assigned to a valuation assignment:

To provide some examples, if the subject interest in a valuation assignment is a non-controlling minority investor, then the Nonmarketable Minority Value would likely be most appropriate. If the subject interest is a controlling owner, then the Financial Control Value could be considered. An experienced valuation expert should be able to help determine the appropriate level of value for an engagement and should also be able to quantify any Minority Interest Discount or Discount for Lack of Marketability that is deemed necessary in that engagement. Check out this blog post by Mercer Capital for a more in-depth look at the Levels of Value.

Defining the assignment in a valuation engagement can seem like a tall task but asking the right questions and having the right discussions with the right valuation expert at the beginning of an engagement can assist the process. You can think of the assignment definition process as building a road map for the valuation. Mercer Capital has extensive experience with a variety of valuation matters, including industry-expertise and complex scopes.