Executive Summary

The composition of privately held business wealth has evolved from traditional common equity ownership toward increasingly complex and economically differentiated interests.

For transfer-tax purposes, these interests may present significantly different valuation, liquidity, and appreciation characteristics despite arising from the same underlying transaction.

As ownership interests become more economically differentiated, valuation becomes an increasingly important component of transfer-tax planning and reporting.

Introduction: Complex Capital Structures are Becoming More Common

Capital structures of privately held businesses have become increasingly sophisticated in recent years. Once the preserve of venture capital and large private equity transactions, complex capital structures now appear regularly in family-owned businesses, founder-led companies, and real estate holding and other closely held investment companies.

Several forces have contributed to the proliferation of preferred equity, convertible securities, profits interests, earnouts, carried interests, and other forms of structured participation rights across privately held companies. Private equity investment has introduced institutional capital structure concepts to the middle market. Founders are increasingly comfortable with exit transactions that provide partial liquidity and future upside participation. Companies competing for management talent frequently utilize incentive equity compensation arrangements designed to reward future value creation rather than historical ownership.

The relevance of complex capital structures for gift and estate tax planning has increased as they have become more prevalent. At the same time, these arrangements engender significant valuation complexity.

Unlike traditional single-class equity structures, the value of a particular interest within a complex capital structure depends not only on aggregate enterprise value but also on the specific rights, preferences, and economic features associated with each ownership class.

This article discusses how modern transactions create economically differentiated ownership interests and examines the valuation considerations those interests present in transfer tax contexts.

EXHIBIT 1

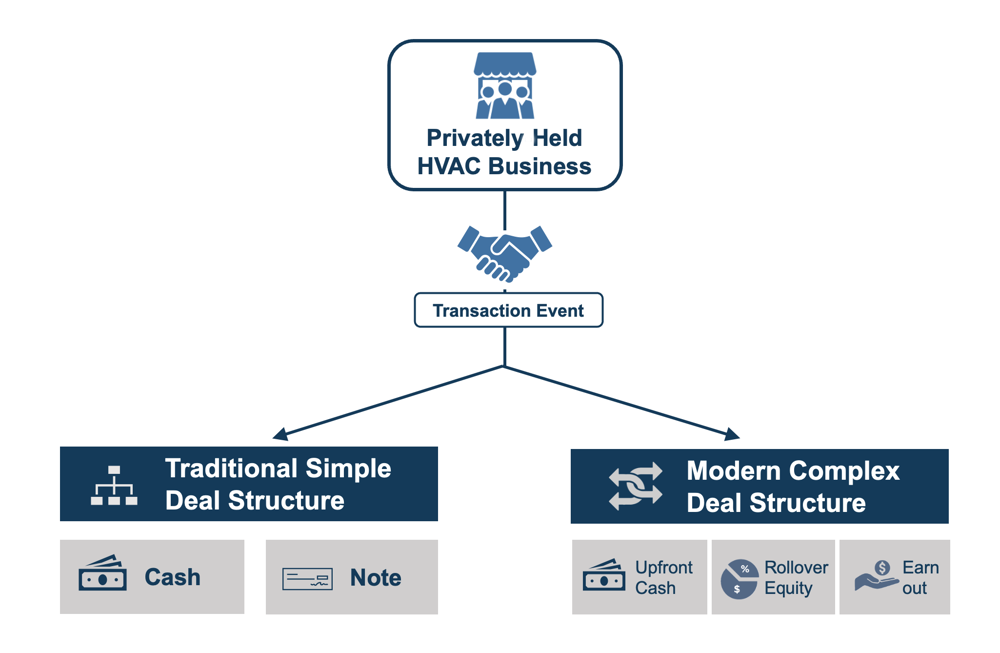

Illustration: Middle-Market Transactions Have Evolved

Consider the sale of a founder-owned HVAC services company. Historically, these transactions were often completed through straightforward cash purchases of the owner’s equity interest.

Today, a private equity-backed acquisition frequently includes multiple forms of consideration, such as upfront cash proceeds, rollover equity in the acquiring platform, management incentive equity, and contingent earnout arrangements tied to future performance.

As a result, owners and management teams increasingly participate in layered capital structures with differing rights to current value, downside protection, and upside participation.

On the Nature of Risk and Return: The Economic Logic Underpinning Complex Capital Structures

Rather than treating all equity holders the same, complex capital structures allocate value, risk, and return differently (i.e., non-pro rata) across ownership classes. In broad terms, total equity is often conceptually bifurcated into senior and junior classes. Senior classes, such as preferred equity, usually provide downside capital protection using structural features such as liquidation preferences, priority distribution rights, or fixed rates of return. Junior interests, by contrast, participate disproportionately in future enterprise value after specified thresholds or return hurdles have been satisfied, and are often used to align management incentives with future value creation. As a result, different equity classes embody materially different economic profiles despite deriving value from the same underlying business.

These arrangements can accommodate different objectives, time horizons, and risk tolerances among ownership groups. Such structures often arise in contexts involving succession planning, charitable giving, wealth transfers across generations, alignment of family stakeholders with differing economic goals, risk management, and other estate planning objectives. A thoughtful examination of the underlying economic features, often against the backdrop of the business and industry characteristics, is necessary to understand their valuation implications.

Crucially, complex capital structures separate current economic value from future appreciation potential. Depending on the structure, certain interests may represent most of the enterprise’s current value, while others derive much of their value from future growth and liquidity outcomes. These differences in economic rights can result in materially different fair market values of the various ownership classes.

Modern Transactions Create Economically Differentiated Interests

A Common Example: Private Equity-Backed Transaction

A defining characteristic of modern middle-market transactions is that a single transaction may create multiple ownership interests with materially different economic profiles. PE buyers typically favor structured consideration over a simple cash payment, often using some combination of upfront cash, seller notes, rollover ownership interests in the acquiring company (platform), and contingent consideration or earnouts. Rather than holding a single class of common equity, founders, management teams, and investors may each hold interests with distinct economic rights, return expectations, and valuation characteristics.

Sponsors typically hold senior equity positions that have liquidation preferences and preferred returns. The downside protection and stable return provisions enable capital providers to manage risks while limiting upside participation. Conversely, employees participate in residual value creation through profits interests or other equity compensation mechanisms. These interests are economically junior and riskier, primarily offering upside upon a successful liquidity event. The rollover interests, usually common equity in the platform, typically occupy an economic position between the senior preferred and junior incentive interests.

By design, profits interests participate only in appreciation above a specified threshold value or hurdle amount. Their values are predicated less on current (intrinsic) benefits and more on the optionality of the upside. Similarly, contingent earnout arrangements have a riskier economic profile compared to cash payments or seller notes, accruing value only upon the achievement of specified results.

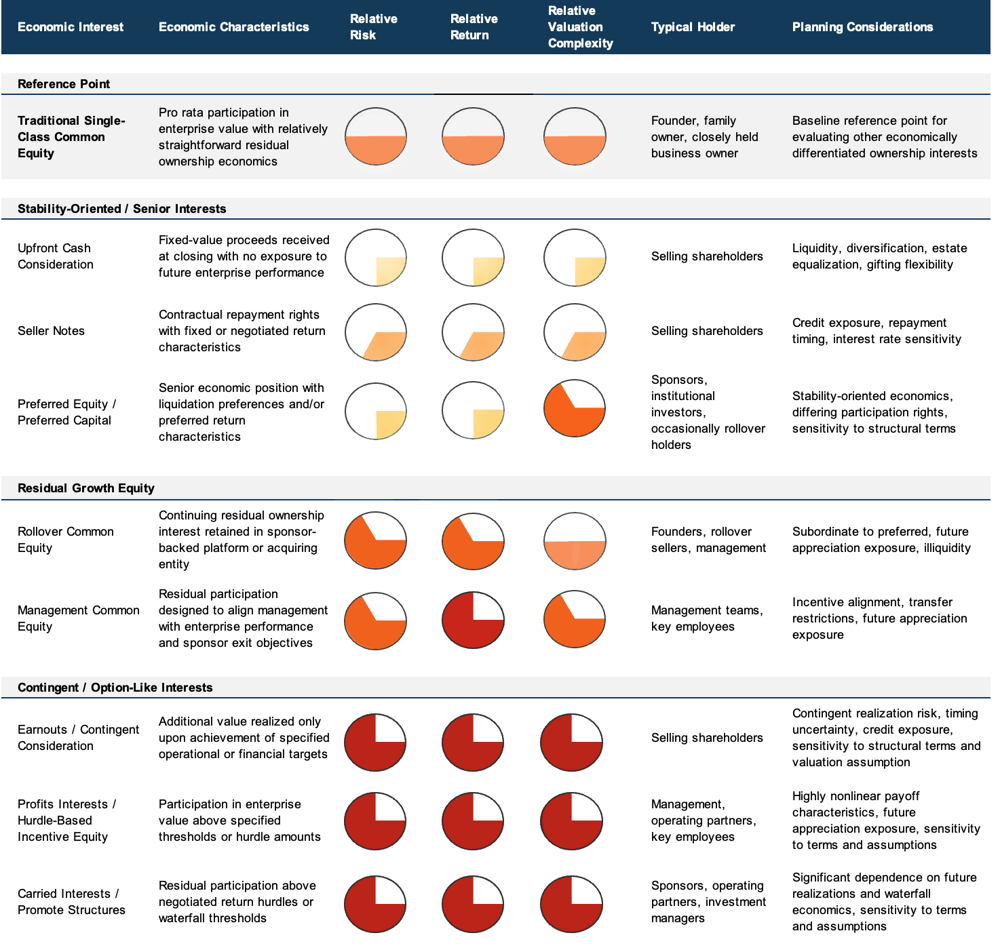

The following table summarizes economic interests that may arise from a PE transaction. From the perspective of transfer-tax planning, these interests may present materially different valuation, liquidity, and appreciation characteristics despite arising from the same underlying transaction.

EXHIBIT 2

Illustration: One Transaction, Multiple Economic InterestsSingle-class equity included as a baseline for evaluating the profiles of other economic interests

Single-class equity included as a baseline for evaluating the profiles of other economic interests

Variations on a Theme: Structural Features

Components of complex capital structures are often described using broad labels such as preferred equity, common equity, rollover equity, and incentive compensation. However, the underlying economics can vary substantially depending on the specific rights embedded within the governing agreements.

Liquidation preferences. A preferred security is usually entitled to receive preferential payments before junior interests participate in proceeds. The amount and structure of that preference can vary considerably. Some interests may receive only a return of invested capital, while others may include cumulative preferred returns or enhanced liquidation rights that increase the senior claim over time.

Participation rights. Some preferred interests cease participating once a specified return threshold has been achieved, while others continue to share in future value creation alongside junior interests. Participation rights may be capped or uncapped and can materially affect both downside protection and upside participation.

Conversion features. In some structures, preferred interests may convert into common equity upon the occurrence of specified events or at the election of the holder. The ability to transition from a senior economic position to a residual ownership interest can significantly affect expected returns and valuation outcomes.

Incentive compensation. Arrangements frequently incorporate performance-based thresholds designed to align management with value creation objectives. These thresholds may be based on enterprise value, internal rates of return (IRR), multiples of invested capital (MOIC), or other performance metrics.

Viewed collectively, these features illustrate that complex capital structures rarely fit neatly into traditional categories such as debt or common equity. Instead, the constituent interests often occupy a continuum of risk and return characteristics ranging from relatively stable instruments with defined economic rights to highly contingent interests whose value depends on future enterprise performance and liquidity outcomes. Where a particular interest falls along this continuum is often essential to both its economic behavior and its value.

Valuation Considerations

The valuation process typically begins with a determination of the overall value of the underlying business using traditional valuation approaches, including the income, market, and asset approaches. These methodologies establish the aggregate value of the enterprise before considering allocation of value across the capital structure.

When a business has multiple classes of equity with differing economic rights, value can no longer be allocated on a simple pro rata basis. As capital structures become more sophisticated, allocating value among ownership classes becomes increasingly complex. Consequently, understanding the relevant economic features is as important as understanding the legal form of the ownership interest.

Valuation outcomes can be highly sensitive to assumptions regarding volatility, holding period, and the rights associated with each class. In our experience, allocation attempts based on rules of thumb are usually deficient. The variety and complexity of these structures make simplifying assumptions potentially misleading. There are no shortcuts – the analysis must consider how distributions, future appreciation, and exit proceeds are expected to flow through the capital structure under a range of potential outcomes.

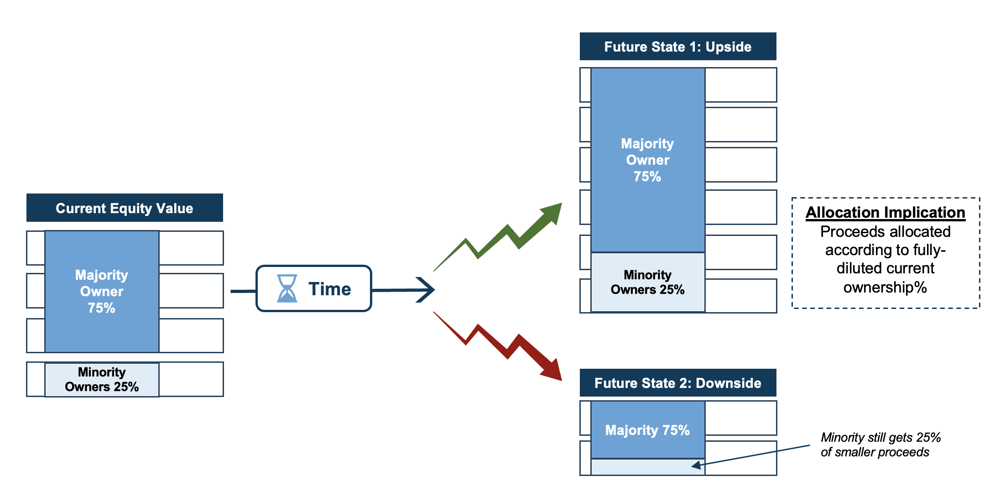

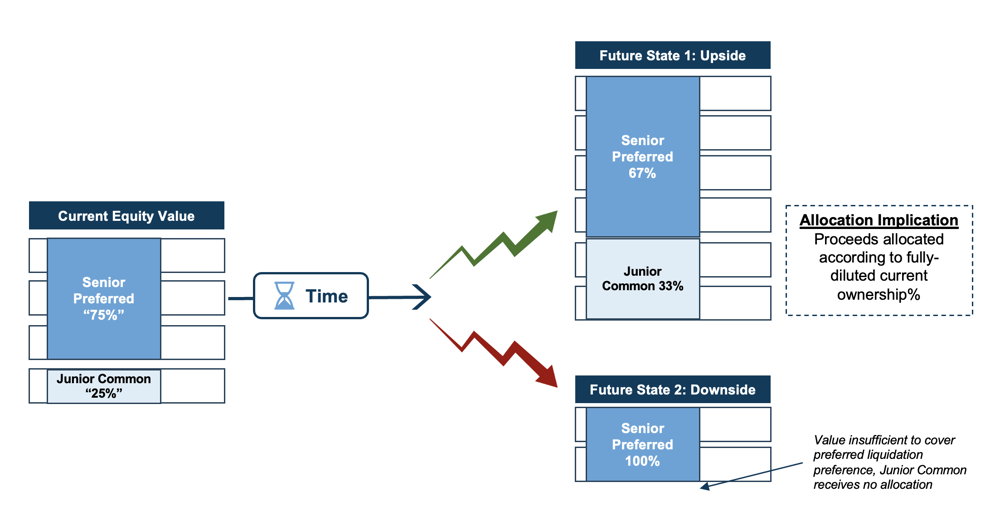

EXHIBIT 3

Potential Outcomes with Traditional Pro-Rata Common Ownership

Potential Outcomes with Preferred/Common Ownership

EXHIBIT 4

Option-Like Features of Junior Equity Can Result in Unintuitive Valuation Results

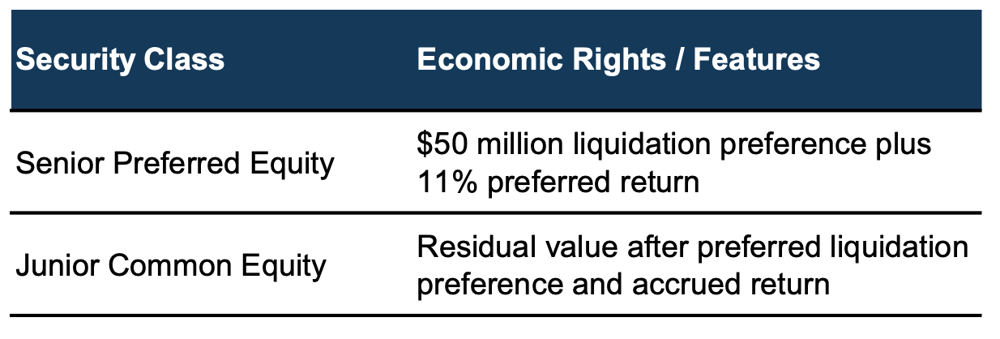

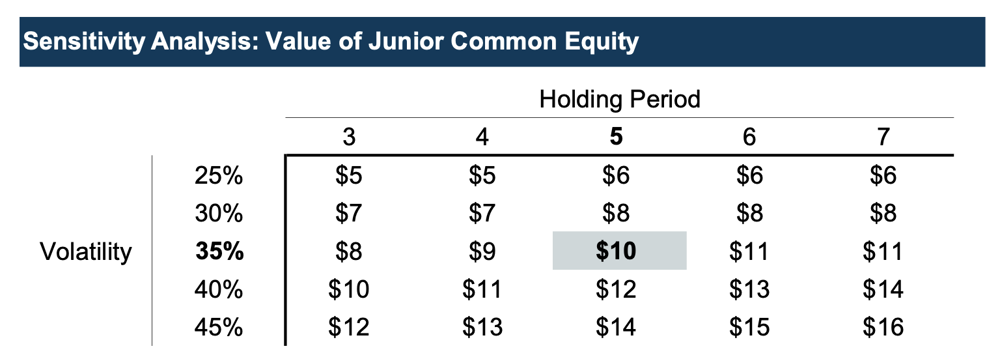

Consider a privately held business with total equity value of $50 million. The capital structure includes preferred equity with a $50 million liquidation preference and 11% preferred return, and common equity that receives the residual.

A simple allocation using total equity value and terms of the preferred equity may suggest the junior common class has little to no residual value at present. However, there is significant optionality embedded in the economic rights/features of the common equity. Assuming a holding period (time until exit) of 5 years, volatility of 35%, no interim distributions, and a risk-free rate of 4% within a Black-Scholes option pricing framework, the junior class has a value of $10 million or 20% of the equity value.

The following illustrates changes in the value of the common equity for various holding period and volatility assumptions.

Several valuation methodologies are commonly used in practice, sometimes in combination, depending on the facts and circumstances:

The scenario-based method (“SBM”) is often the most intuitive, but it usually requires a deft touch. The analyst identifies discrete outcomes (scenarios) with associated future enterprise values, each of which is allocated through a waterfall to the various classes based on their relative rights and preferences. The scenarios are probability-weighted, and the allocated amounts are discounted to the present. This method is useful when a near-term transaction, financing event, or liquidity event is anticipated.

The option pricing model (“OPM”) is frequently used when there are no near-term transactions or liquidity events to consider and a longer holding period is anticipated. Under the OPM framework, each class of security is treated as a call option on enterprise value, with exercise prices determined by liquidation preferences and participation thresholds.

Monte Carlo simulation techniques may be necessary for capital structures with highly complex or path dependent payoffs, including certain earnouts, incentive compensation arrangements with discontinuous payoffs, and certain derivative-like instruments.

In addition, voting rights, distribution authority, and other governance provisions form an additional overlay of considerations for the valuation of the subject interests.

Conclusion: Valuation as Part of the Planning Process

As private company capital structures continue to evolve, valuation is an increasingly integral component of the planning process itself rather than functioning solely as a downstream reporting exercise. For complex capital structures, a thorough reading of governing agreements is critically important for the overall defensibility of a valuation analysis. Since companies can have customized provisions around liquidation preferences, participation rights, conversion features, and incentive compensation, there is no one-size-fits-all valuation model. Each analysis should carefully consider the relevant documents to capture the economics accurately. Given the non-linear payoffs involved, valuation conclusions are sensitive to a number of assumptions including expected growth and future exit outcomes.

A rigorous analysis provides defensible valuation conclusions and helps stakeholders understand the economics embedded within increasingly differentiated ownership interests arising from modern transactions. In that context, involving valuation professionals early in the transfer planning process may be invaluable.

Mercer Capital assists clients with independent valuations for gift and estate tax reporting, including analyses of complex capital structures. To confidentially discuss a transfer tax planning opportunity or learn more about the nuances of these complex capital structures, please contact a Mercer Capital professional.