When people talk about the “value” of a company, it is easy to assume there is one correct “answer.” In practice, there are many possible answers, and which one is the best answer depends on the purpose of the valuation, the user, and the facts and circumstances at hand. The Internal Revenue Service’s Revenue Ruling 59-60 defines fair market value “as the price at which the property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of the relevant facts.” This is a great place to begin, but it is only the start.

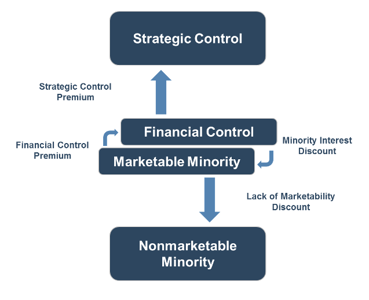

Business valuation also depends on the level of value being considered. A controlling interest can be worth more than a minority interest because control may allow the owner to direct strategy, dividends, capital allocation, or a sale process. Controlling interest values can be from the perspective of a strategic buyer, which may include premiums not available to other buyers following the integration of the business, or from the perspective of a financial control buyer, which does not include such premiums and focuses on a broader set of hypothetical owners. (Frequently, strategic control levels of value do not fall under the purview of fair market value.) A marketable minority interest reflects a noncontrolling stake that can still be freely traded, such as stock in a public company. A nonmarketable minority interest lacks both control and liquidity, which is why it is generally the least valuable level in the traditional hierarchy.

Another key variable is the premise of value – essentially, are we valuing the company as a going concern, assuming it will continue operating and producing cash flow into the future, or are we valuing it on a liquidation basis, assuming the business will cease operations and the underlying assets will be sold? That distinction matters enormously, because in the example of an airline, the same aircraft, gates, routes, brand, and customer base can produce very different values depending on whether they are

part of a functioning airline or being sold piecemeal in a wind-down. Spirit Airlines (formerly NYSE: SAVE) provides a useful case study in how quickly a going-concern can go from cruising altitude to fully grounded. (As a note: we usually try to keep the focus of these newsletter articles on events occurring in the quarter covered. Given the timing and relevance of the Spirit timeline, however, we did look at events and articles from as late as May 2026 when preparing this newsletter.)

For years, Spirit’s business model was built around a very simple proposition: sell low base fares, then monetize the extras. That “ultra-low-cost” model helped make air travel more accessible and forced larger carriers to respond with basic-economy products of their own. But the same model was also highly dependent on operating discipline, high aircraft utilization, and a cost structure that stayed low enough to support very thin margins. Spirit’s own 2024 filings and later coverage make clear that rising operating costs, debt, and the post-pandemic environment pushed the model into severe distress. By the time Spirit shut down in May 2026, the airline had operated for 34 years, had roughly 17,000 employees, and had struggled badly since the pandemic.

This is where Spirit becomes a useful case study from a valuation standpoint. The company moved through several very different value stories in a relatively short period of time. In 2022, the proposed JetBlue (NASDAQ:JBLU) transaction valued Spirit’s equity at $3.8 billion on a going-concern basis (the enterprise value, meaning the combined equity and debt value of Spirit, was estimated at $7.6 billion). JetBlue said that figure implied $33.50 per Spirit share, with the transaction value rising to as much as $34.15 per share depending on closing timing. In other words, this transaction reflected a strategic going-concern value, not a liquidation value, and not merely a minority trading value.

That transaction later fell apart after the court blocked it on antitrust grounds, and JetBlue terminated the deal in March 2024. The Justice Department said the merger had been abandoned after the court found that it would violate antitrust law and harm consumers. Spirit’s subsequent value picture changed quickly after that strategic exit disappeared.

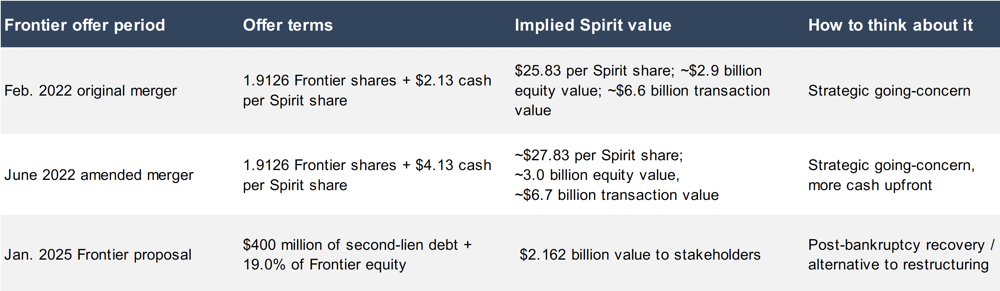

Frontier (NASDAQ:ULCC) made a series of offers to Spirit from 2022 through 2025. Frontier’s offers are a particularly useful illustration of how the same company can look very different depending on the deal structure and the valuation premise. Spirit’s 2022 deal with Frontier originally implied about $25.83 per Spirit share, or roughly $2.9 billion of equity value, with a transaction value of about $6.6 billion once debt and lease liabilities were included. Frontier later raised the cash component, but then, after Spirit entered distress, returned with proposals that were explicitly framed as bankruptcy recoveries rather than simple public company merger consideration. The valuation math changed from “What is this airline worth as a strategic going-concern?” to “What do creditors and equity holders receive in a reorganization or wind-down?”

By 2025, Spirit’s equity story was experiencing significant turbulence. Spirit’s own disclosures showed how fragile the going-concern case had become. In its 2024 Form 10-K, Spirit reported operating revenue of $4.9 billion and a net loss of $1.2 billion for the year, while also describing the continuing pressure from inflation, lower fares, and weaker operating performance. Its later filings show that it filed Chapter 11 again in August 2025 after emerging from an earlier restructuring only months before. That is the sort of sequence that tells a valuation analyst the relevant question is no longer “What is the stock worth?” but “What is the enterprise worth under distress?”

That distinction matters because a distressed airline may still have meaningful assets. Spirit retained aircraft, route authorities, gates, customer relationships, and a well-known brand. But when the business no longer generates durable cash flow, those assets are valued differently. At that point, the market is not pricing the enterprise as a going-concern. It is pricing the pieces, and that means a liquidation basis becomes more relevant than a going-concern basis.

Spirit’s business model depended on low costs, including low fuel prices, in order to keep its fares low. By May 2, 2026, Spirit said it had started an orderly wind-down, canceled all flights, and no longer offered customer service. The airline cited soaring jet fuel costs tied to the Iran conflict as the decisive blow.

The broader lesson is that valuation is not just about numbers. It is about the question being asked. Spirit could be worth one amount to a strategic acquirer, another amount to creditors in bankruptcy, and still another amount if broken apart and sold asset by asset. The company’s collapse does not mean the earlier valuations were “wrong.” It means they were answering different questions under different assumptions. That is the real lesson Spirit offers to valuation professionals: value is contextual, and context can change very quickly.