During Hamilton Lane’s (NASDAQ:HLNE) earnings conference call on May 21, 2026, CEO Erik Hirsch opined that secondaries offered one of the most compelling risk/reward assets in the private markets. In terms of LP-led secondaries, buyers get an interest in a seasoned, diversified portfolio whereas selling LPs obtain liquidity for an illiquid investment.

Hirsch offered a full throated defense of marking LP interests at NAV when the interest is purchased at a discount to the GP’s NAV mark, noting that what was sold was an interest in the fund and not the underlying assets. The LP interest is then marked consistent with all other LPs’ interest.

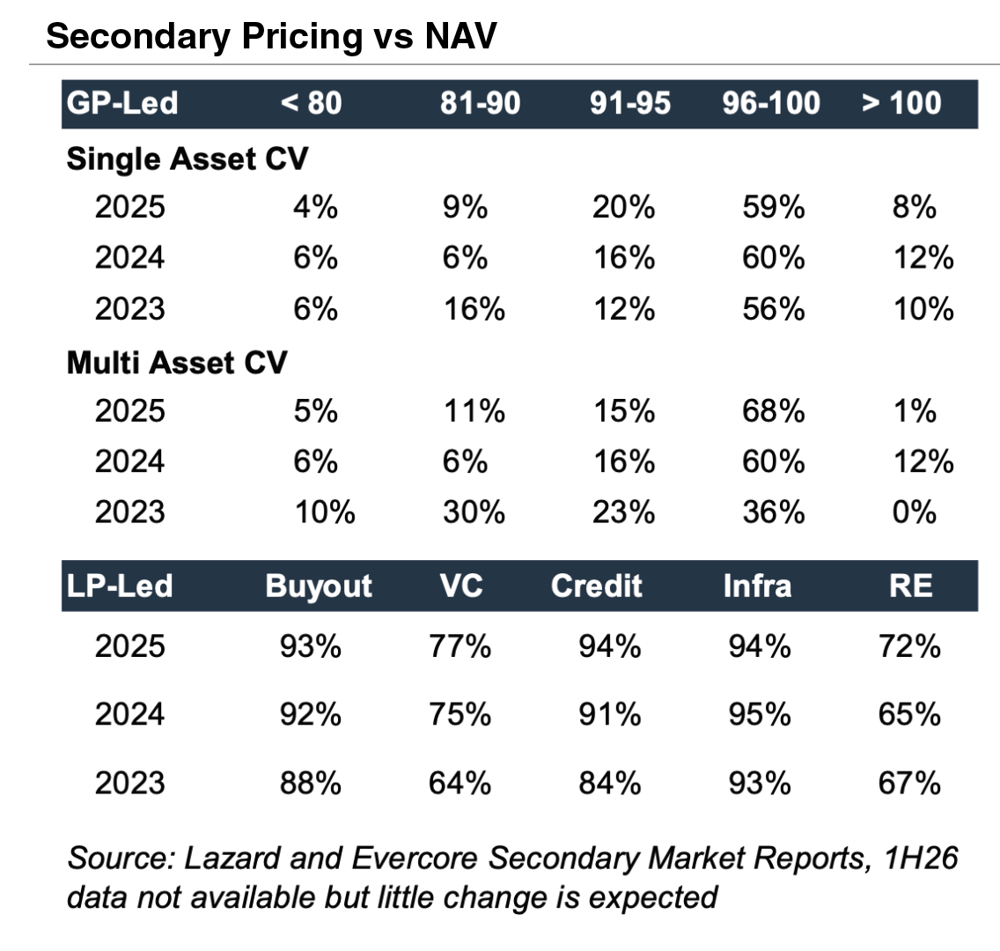

The logic is perfectly sensible. When LPs sell their interest via a secondary transaction, the delta with NAV will reflect a discount for lack of marketability (“DLOM”), though the DLOM may be overstated to the extent the NAV mark is overstated. The reverse would be true, too. During 2015 to 2025, the discount (i.e., DLOM) ranged between 7% and 19% and averaged 12% according to Hirsch. Discounts also vary based on the fund assets (e.g., 23% for venture vs 7% for buyout in 2025).

However, what about a discount to NAV when fund assets transact via a continuation vehicle (“CV”) in a GP-led secondary transaction? NAV is a reference point, but the GP’s valuation of the assets is not necessarily synonymous with a third party’s view of fair value for the assets. At a most basic level, the lead investor who capitalizes the CV may have a higher IRR requirement that Ben Graham and his acolytes would call “margin of safety” pricing. The discount, if one exists, becomes murkier when assets represent non-control equity and/or indirect ownership via assets that are held by another fund.

Transaction data indicates that on average discounts to NAV for GP-led CV deals have narrowed over the last few years, though the actual economics are less clear if earnouts, deferred payments and the like are marked-to-market rather than treated as nominal dollars that eventually will be realized. Given that a GP is a seller and a buyer for the same asset in a CV transaction, process followed is fundamental to evaluating pricing and fairness to LPs.

ILPA Doubles Down

The Institutional Limited Partners Association’s (“ILPA”) June 2026 draft Continuation Vehicle Guidance builds on ILPA’s May 2023 framework but adds expectations around LPAC engagement, competitive price discovery, disclosure parity, election timing, GP alignment, and documentation.

ILPA notes that CVs represented approximately 14% of sponsor-backed exits globally in 2025, up from 5% in 2021. That growth reflects a growing backlog of aging investments whereby M&A activity has been uneven with arguably insufficient capacity among strategic buyers to absorb the inventory when combined with a valuation gap between what buyers would be willing to pay and what GPs think the asset is worth.

The June 2026 guidance moves beyond broad principles by prescribing what a well-run continuation vehicle process should look like. Among other Actions. , ILPA expects GPs to do:

Demonstrate why a continuation vehicle is preferable to alternatives such as a traditional sale, fund extension, NAV facility, preferred equity solution, strip sale, tender offer, cross-fund transaction, or mid-life co-investment.

Engage the LPAC early in the process and fully disclose all conflicts of interest, even where the LPAC arguably pre-clears them.

Conduct a targeted competitive bidding process supported by independent third-party price

validation.

Provide LPs with an anonymized summary of final-round bids, including price terms, non-cash consideration, deferred payments, earn-outs, and other key commercial and legal terms.

Explain how the transaction price was determined and how it compares to the fund’s most recent reported NAV.

The practical implication is that LPs should not be asked to rely solely on NAV, a single lead bid, or a fairness opinion without additional context. Instead, LPs should have sufficient information to assess whether the process generated an executable market-clearing price.

The LPAC as Gatekeeper

ILPA also recommends that the LPAC process include:

Live LPAC meetings rather than written consents.

In-camera sessions without the GP present.

At least ten business days to review conflicts materials before voting.

Equal treatment of all LPAC members.

The option to retain independent legal and

financial advisors.

These recommendations recognize that continuation vehicle conflicts are structural. Those conflicts cannot be eliminated, but they can be disclosed, evaluated, and managed through a robust governance process.

Election Timing Gets Longer

ILPA’s 2023 guidance recommended at least 30 calendar days, or 20 business days, for LP elections. The 2026 draft increases that minimum to 30 business days following delivery of the complete election package, with unrestricted access to the centralized data room throughout the election period.

Rolling LPs Should Be No Worse Off

ILPA continues to emphasize that rolling LPs should be no worse off economically than if the continuation vehicle transaction had not occurred. To that end, the guidance recommends that GPs:

Demonstrate that there is no overall increase in management fees or carried interest for rolling LPs, supported by modeling in actual dollars rather than headline percentages.

Extend existing side-letter protections where applicable and provide sufficient time to update those provisions to reflect current minimum requirements.

Avoid conditioning roll elections on minimum commitment sizes or stapled financing.

Avoid scaling back the elections of LPs choosing to roll.

These recommendations are intended to ensure that LPs who continue their investment are not disadvantaged economically or procedurally compared to selling investors or new capital providers.

The Valuation and Fairness Takeaway

ILPA’s June 2026 guidance, which is ultimately about process integrity, is not going to radically change how GP-led transactions are conducted; rather, assuming the guidance is adopted, corporate governance for such transactions will be strengthened to the extent GPs follow it. Mercer Capital can be an important partner in a GP-led transaction. We have over 40 years of experience in valuing illiquid securities and providing fairness opinions to boards of directors, special committees, LPACs, GPs and others involved in significant transactions such as GP-led secondaries.

Originally appeared in Mercer Capital's Portfolio Valuation Newsletter - Summer 2026