In August 2022, the SEC adopted final rules implementing the Pay Versus Performance Disclosure required by Section 953(a) of the Dodd-Frank Act. These rules go into effect for the 2023 proxy season and introduce significant new valuation requirements related to equity-based compensation paid to company executives. What does this mean, and how does it apply to you? What are the requirements, and why might there be significant valuation challenges involved? We discuss all that and more below.

Advance planning and processes will be needed to establish the scope and complexity of complying with the new rules, including identifying how many equity-based awards will require updated valuations to measure the period-to-period changes.

The new disclosures were mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act and were originally proposed by the SEC in 2015. These rules will add a new item 402(v) to Regulation S-K and are intended to provide investors with more transparent, readily comparable, and understandable disclosure of a registrant’s executive compensation. The new provisions apply to all reporting companies other than (i) foreign private issuers, (ii) registered investment companies, and (iii) emerging growth companies.

The rules apply to any proxy and information statement where shareholders are voting on directors or executive compensation that is filed in respect of a fiscal year ending on or after December 16, 2022. As such, the vast majority of registrants will be required to include related disclosure for their 2023 proxy statements, though there are relaxed requirements for smaller reporting companies.

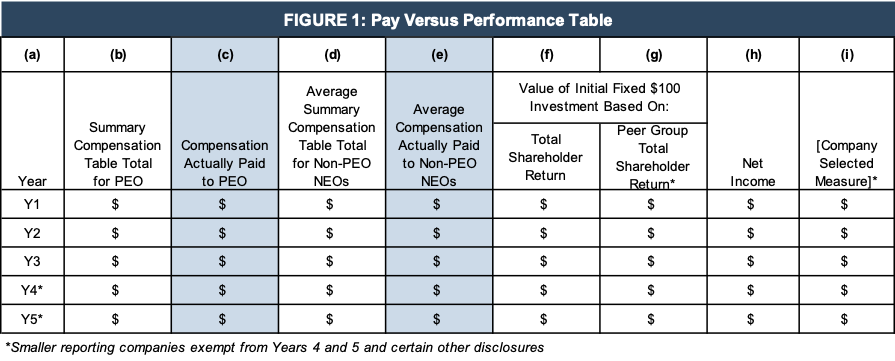

The new rules require registrants to describe the relationship between the Executive Compensation Actually Paid (“CAP”) and the financial performance of the registrant over the time horizon of the disclosure. Additional items include disclosure of the cumulative Total Shareholder Return (“TSR”) of the registrant, the TSR of the registrant’s peer group, the registrant’s net income, and a company-selected measure chosen by the registrant as a measure of financial performance. These items are to be disclosed in tabular form (based on an example included in the final rule), which is replicated below.

Click here to expand the table above

The table includes the following components:

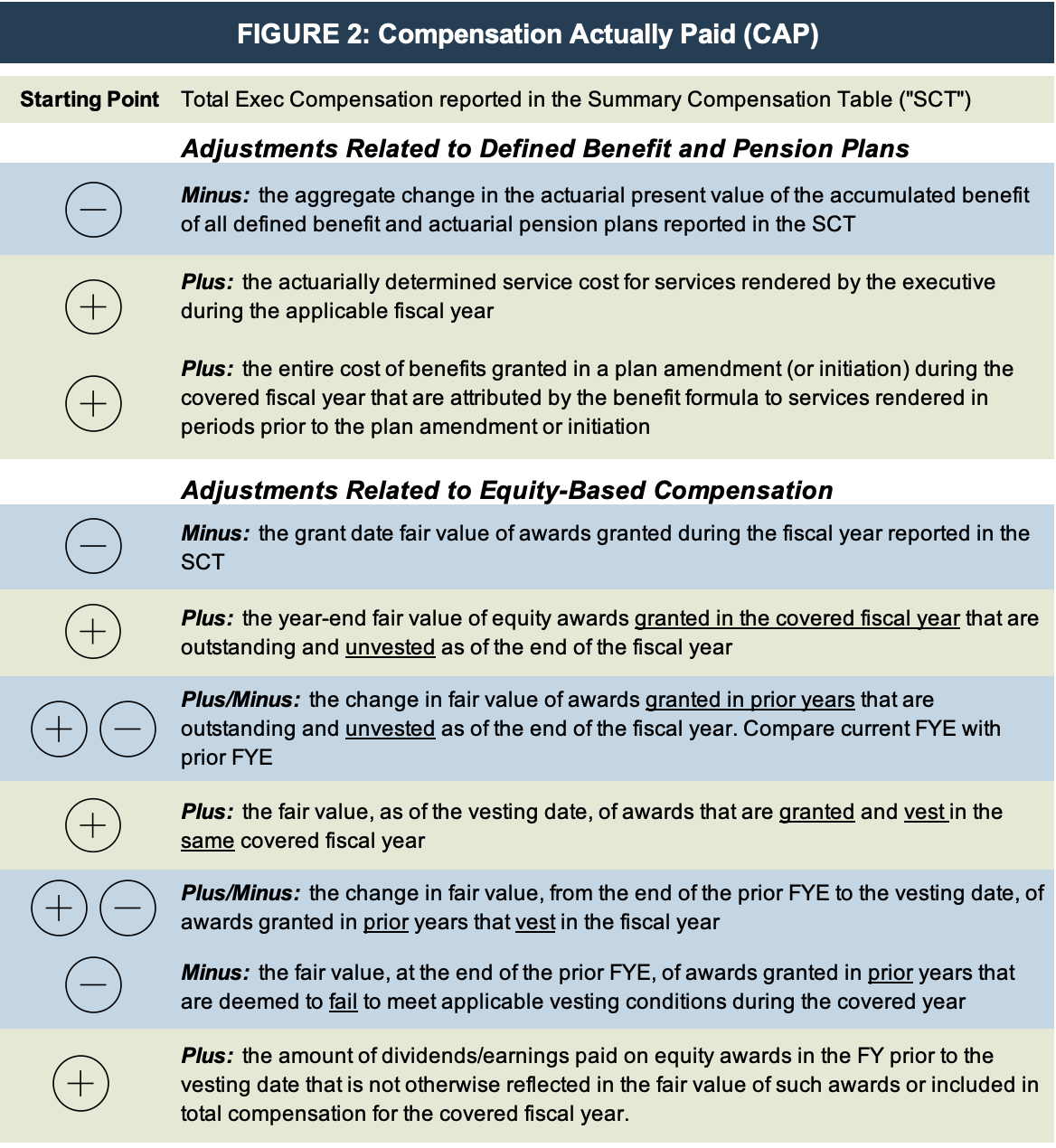

The remainder of this article focuses on the two shaded columns (c) and (e) which address Compensation Actually Paid and the valuation inputs that support these disclosures.

For each fiscal year, registrants are required to adjust the total compensation reported in Columns (b) and (d) for pension and equity awards that are calculated in accordance with US GAAP. The following table describes these adjustments in detail.

The pension-related adjustments should be calculated using the principles in ASC 715, Compensation – Retirement Benefits. The equity-based compensation adjustments will require registrants to disclose the fair value of equity awards in the year granted and report changes in the fair value of the awards until they vest. This means that it will be necessary to measure the year-end fair value of all outstanding and unvested equity awards for the PEO and other NEOs under a methodology consistent with what the registrant uses in its financial statements. For most registrants, this will be ASC 718, Compensation – Stock Compensation.

Appropriate footnote disclosure may also be required to identify the amount of each adjustment and any valuation assumptions that materially differ from those disclosed at the time of the equity grant.

The procedures used to calculate fair value will vary depending on the type of equity award.

Market condition awards come in many different flavors. Three of the most common types of plans include:

Each of the above plans has inputs and assumptions that drive the Monte Carlo simulation. When performing a subsequent year-end or vesting date fair value analysis, each of the grant-date assumptions will need to be reevaluated. For example, for a relative TSR plan with a three-year term, the subsequent year-end valuations will necessarily have shorter terms (2-year and 1-year), which will require new inputs for volatility and correlation factors. Shorter terms may make the use of option-implied volatility more relevant if sufficient market data is available.

For relative TSR plans that reference a group of companies or an index, some of the peers may have been acquired or merged in the subsequent periods. The plan documentation will often describe the steps to be taken when the composition of the peer group changes or there is a change in the benchmark index. A different group (or number) of companies will affect the correlation assumption as well as the percentile calculations in a ranked plan.

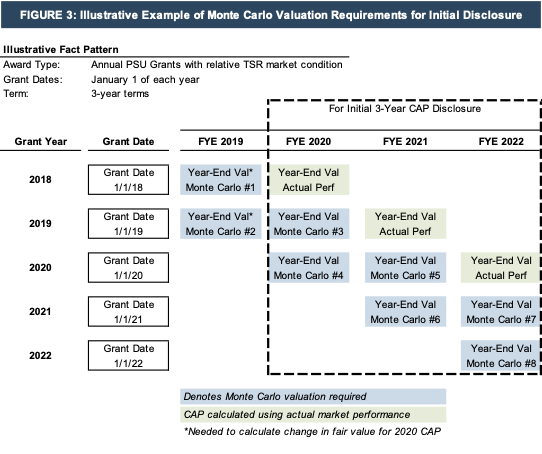

Regardless of the type of plan, it is important for registrants to understand how even a relatively simple award, if granted consistently for a period of years, can lead to a large number of Monte Carlo simulations for this initial proxy season and a significant amount of disclosure complexity.

As shown in Figure 3 below, if a company has made annual PSU grants (with a market condition) for each of the last five years, then up to eight Monte Carlo valuations could be required to calculate the CAP in each period.

Click here to expand the example above

In the example above, the blue boxes indicate when a valuation of prior grants would be necessary to calculate the change in fair value for each period of the CAP disclosure. For the final period of a relative TSR market condition plan, the company could use the actual market performance of its stock (and the comparative index) to calculate the expected value of the award.

While the new SEC Pay Versus Performance disclosure rules can seem daunting, they can be managed with proper planning and a systematic approach. For the CAP disclosures, registrants need to understand the details of all equity awards that have been awarded to named executive officers (how many and what type of award). The award characteristics will determine which valuation method is most appropriate and how many valuations need to be performed.

If you have questions about the valuation techniques used for the various types of equity compensation awards or would like to discuss the process, please contact a Mercer Capital professional.