In previous posts, we have discussed the market pricing implications of publicly traded royalty trusts to royalty and mineral owners. We have explained the importance of understanding the specifics underlying those trusts before using them as a pricing benchmark. In this post, we will delve further into market prices of royalty and mineral interests and the important role of operators. We will look into the three publicly traded royalty trusts operated by SandRidge Energy: SandRidge Mississippian Trust I, SandRidge Mississippian Trust II, and SandRidge Permian Trust.

Market Observations1

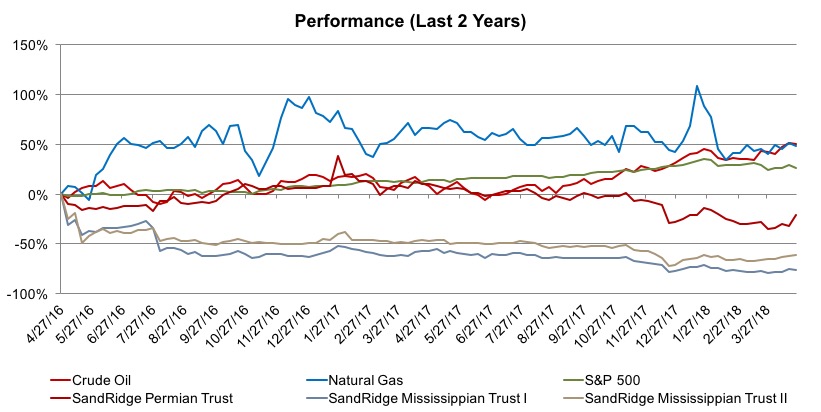

Over the previous two years, the performance of the 21 publicly traded royalty trusts has varied widely. Thirteen have experienced positive market value returns with an average of positive 57% and eight have returned market value losses during the previous two years with an average market value return of negative 39%.

Clearly, there are some winners and losers, with more winners than losers. The royalty trust with the highest market value return was Whiting USA Trust II (WHZT) (+330%), which was discussed in a recent blog post. Mesa Royalty Trust (MRT) (47%) was another big winner covered in a previous blog post. However, the focus of this blog post will be on some of the underachievers: SandRidge Mississippian Trust I (SDT) (-76%), SandRidge Mississippian Trust II (SDR) (-61%), and the SandRidge Permian Trust (PER) (-21%).

For comparison, the chart below shows the returns from PER, SDR, SDT, crude oil, natural gas, and the S&P 500.

Why has the value of these SandRidge Trusts depreciated so much over the past two years despite increasing commodity prices? Also, why has the Permian trust fared better than the Mississippian Trusts? Below is a discussion of the assets, underlying properties, and agreements of each Trust.

Why has the value of these SandRidge Trusts depreciated so much over the past two years despite increasing commodity prices? Also, why has the Permian trust fared better than the Mississippian Trusts? Below is a discussion of the assets, underlying properties, and agreements of each Trust.

SandRidge Mississippian Trust I

The only asset of the Trust is the conveyance of the Royalty Interests by SandRidge Energy, Inc. The Royalty Interest entitles the Trust to receive:

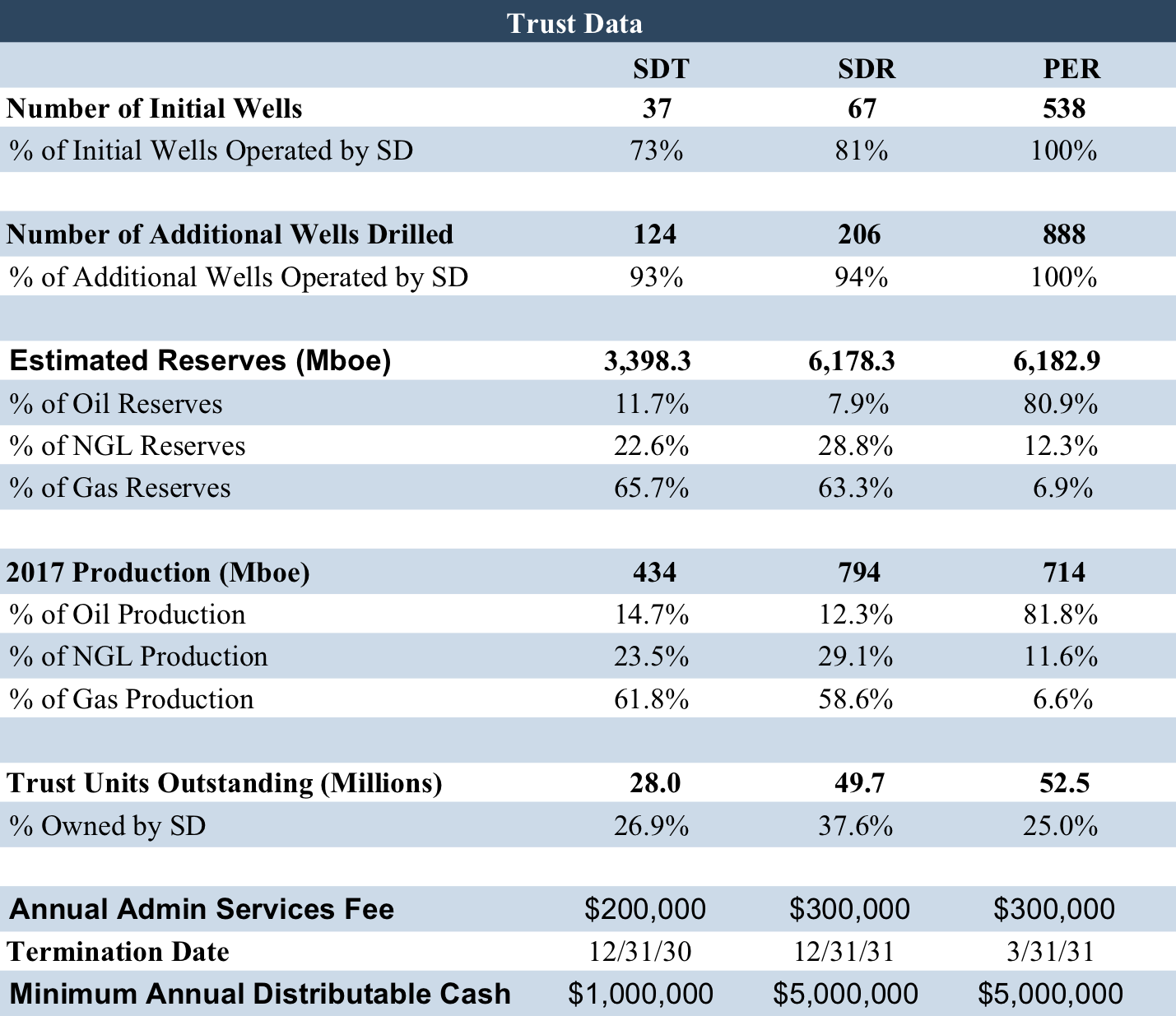

- 90% of the proceeds from the sale of oil, natural gas, and natural gas liquids ("NGL") production attributable to SandRidge’s net revenue interests in 36 wells producing at December 31, 2010, and one additional well undergoing completion operations at that time (together, the “Initial Wells”).

- 50% of such proceeds from 123 “Trust Development Wells” drilled within an area of mutual interest (“AMI”)

SandRidge Mississippian Trust II

The only asset of the Trust is the conveyance of the Royalty Interests by SandRidge Energy, Inc. The Royalty Interest entitles the Trust to receive:

- 80% of the proceeds from the sale of oil, natural gas, and natural gas liquids ("NGL") production attributable to SandRidge’s net revenue interests in 54 wells producing at December 31, 2011, and 13 additional wells awaiting completion at that time

- 70% of such proceeds from 206 horizontal “Trust Development Wells” drilled within an area of mutual interest (“AMI”)

SandRidge Permian Trust

The only asset of the Trust is the conveyance of the Royalty Interests by SandRidge Energy, Inc. The Royalty Interest entitles the Trust to receive:

- 80% of the proceeds from the sale of oil, natural gas, and natural gas liquids ("NGL") production attributable to SandRidge’s net revenue interests in 517 wells producing at April 1, 2011, and 21 additional wells awaiting completion at that time

- 70% of such proceeds from 888 horizontal “Trust Development Wells” drilled within an area of mutual interest (“AMI”)

The Trusts no longer have any hedging derivatives contracts, so they are exposed to oil and natural gas price volatility.

The Trusts no longer have any hedging derivatives contracts, so they are exposed to oil and natural gas price volatility.

Analysis of Trusts

Development Wells and Area of Mutual Interest

Each of the Trusts receives 80-90% of the proceeds from the sale of oil, natural gas, and NGLs (after deducting post-production costs and any applicable taxes). This is fairly common for publicly traded royalty trusts, but the Trust Development Wells are unique. At the IPO date for each Trust, well counts were relatively low. In fact, the initial wells made up less than 25% of the total well counts for the Mississippian Trusts and about 38% of the Permian Trust. This agreement allowed the Trusts to make distributions from currently producing wells in addition to offering growth opportunities with the future development wells.

The “development” aspect of the wells would seem to cast doubt upon the production of each Trust if it did not end up developing the total number of wells required or in a timely manner. The development agreement offered protection to investors. It is important to note that SandRidge fulfilled its development obligation in plenty of time in each case. Investors were further protected with the clause ensuring wells would be drilled in an area of mutual interest (AMI). This means SandRidge could not drill wells in random locations to fulfill its obligation.

Distributions

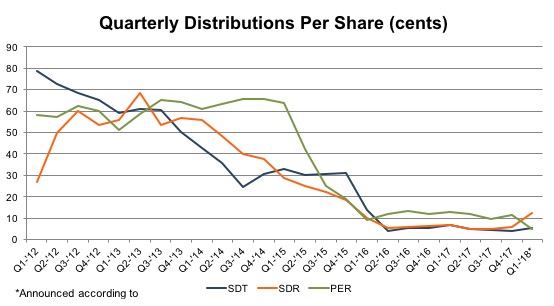

The Trusts make quarterly cash distributions of substantially all of its cash receipts, after deducting amounts for the Trusts’ administrative expenses and cash reserves withheld by the Trustee. The price for oil peaked in 2014 near $108 per barrel and close to $8 for natural gas before declining sharply in the latter half of the year. The low point was seen in late 2015, early 2016, with prices of approximately $28 and $1.64, for oil and gas. Prices currently stand around $68 per barrel and $2.80 per MCF, respectively. The steep decline in oil and gas prices in mid-2014 had a crippling effect on distributions. The following chart tracks the quarterly distributions per share for the Trusts since 2012.

Termination of the Trusts

The Trusts will dissolve and begin to liquidate on the “Termination Date” (noted in the table above). At the Termination Date, 50% of the Royalty Interests will revert automatically to SandRidge. The remaining 50% of the Royalty Interests will be sold at that time, and the net proceeds of the sale, as well as any remaining Trust cash reserves, will be distributed to the unitholders on a pro rata basis. SandRidge has a right of first refusal to purchase the Royalty Interests retained by the Trust at the Termination Date. There are certain provisions protecting investors in the case the Trust were to dissolve prior to the Termination Date, such as a requirement that cash available for distributions be above a certain threshold, as noted in the table above.

The Trusts are highly dependent on its Trustor, SandRidge, for multiple services including the operation of the Trust wells, remittance of net proceeds from the sale of associated production to the Trusts, administrative services such as accounting, tax preparation, bookkeeping, and informational services performed on behalf of the Trusts. For these administrative services, the Trusts pay SandRidge an annual fee (noted in the table above) which is payable in equal quarterly installments and will remain fixed for the life of the Trusts. SandRidge is also entitled to receive reimbursement for its out-of-pocket fees, costs, and expenses incurred in connection with the provision of any of the services under this agreement.

Termination of the Trusts

The Trusts will dissolve and begin to liquidate on the “Termination Date” (noted in the table above). At the Termination Date, 50% of the Royalty Interests will revert automatically to SandRidge. The remaining 50% of the Royalty Interests will be sold at that time, and the net proceeds of the sale, as well as any remaining Trust cash reserves, will be distributed to the unitholders on a pro rata basis. SandRidge has a right of first refusal to purchase the Royalty Interests retained by the Trust at the Termination Date. There are certain provisions protecting investors in the case the Trust were to dissolve prior to the Termination Date, such as a requirement that cash available for distributions be above a certain threshold, as noted in the table above.

The Trusts are highly dependent on its Trustor, SandRidge, for multiple services including the operation of the Trust wells, remittance of net proceeds from the sale of associated production to the Trusts, administrative services such as accounting, tax preparation, bookkeeping, and informational services performed on behalf of the Trusts. For these administrative services, the Trusts pay SandRidge an annual fee (noted in the table above) which is payable in equal quarterly installments and will remain fixed for the life of the Trusts. SandRidge is also entitled to receive reimbursement for its out-of-pocket fees, costs, and expenses incurred in connection with the provision of any of the services under this agreement.

SandRidge Energy and the Importance of the Operator

SandRidge Energy (SD) is an oil and natural gas exploration and production company headquartered in Oklahoma City. According to SD's website, its principal focus is on developing high-return, growth-oriented projects in the US Mid-Continent and Niobrara Shale.

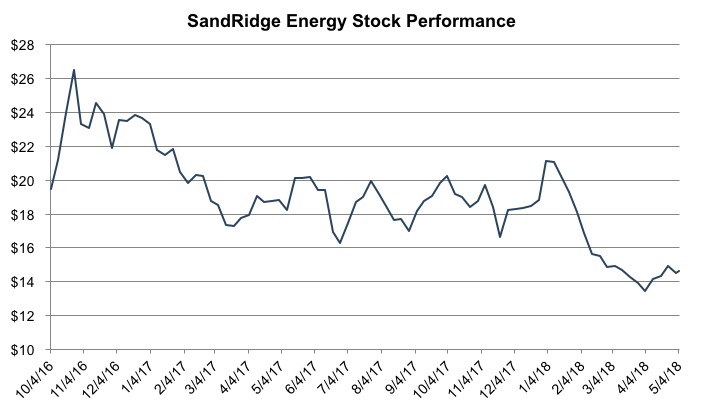

SandRidge filed for Chapter 11 bankruptcy in May 2016 and emerged from bankruptcy in October 2016, as we discussed in a blog post around that time. SandRidge was relisted on the NYSE around $19.50 per share. Its performance has been volatile and generally negative since, as seen in the chart below.

Activist investor Carl Icahn spent $82 million in October and November 2017 to acquire about 13.5% of SandRidge stock. Since he became a shareholder, Icahn has had a large impact, causing directors to cancel their planned $746 million purchase of Bonanza Creek Energy and lay off 80 employees including their CEO and CFO. He also played a role in the rejection of an acquisition attempt by Tulsa-based Midstates Petroleum Inc. in February.

Icahn recently expressed "grave concerns" with the board, claiming it had “a history of making poor decisions on behalf of stockholders.” Market confidence for SandRidge Energy is very low, after having gone through a bankruptcy-related restructuring recently as well.

These concerns are significant to the SandRidge Trusts because operators play a vital role for royalty interests. They are responsible for production, without which, there are no distributions. If an operator is unable to produce or becomes less focused on a particular well or region, the royalty interests attached to them are worth significantly less.

In the case of the SandRidge Trusts, turmoil with the operator has put future production into question. The lack of control for the royalty interests means they are tied to the fortunes of the operator. Even for securities with yields above 20%, the unsustainability of these distributions does not inspire confidence in investors.

Activist investor Carl Icahn spent $82 million in October and November 2017 to acquire about 13.5% of SandRidge stock. Since he became a shareholder, Icahn has had a large impact, causing directors to cancel their planned $746 million purchase of Bonanza Creek Energy and lay off 80 employees including their CEO and CFO. He also played a role in the rejection of an acquisition attempt by Tulsa-based Midstates Petroleum Inc. in February.

Icahn recently expressed "grave concerns" with the board, claiming it had “a history of making poor decisions on behalf of stockholders.” Market confidence for SandRidge Energy is very low, after having gone through a bankruptcy-related restructuring recently as well.

These concerns are significant to the SandRidge Trusts because operators play a vital role for royalty interests. They are responsible for production, without which, there are no distributions. If an operator is unable to produce or becomes less focused on a particular well or region, the royalty interests attached to them are worth significantly less.

In the case of the SandRidge Trusts, turmoil with the operator has put future production into question. The lack of control for the royalty interests means they are tied to the fortunes of the operator. Even for securities with yields above 20%, the unsustainability of these distributions does not inspire confidence in investors.

Conclusion

The operator is a key consideration for owners of royalty interests, particularly those interested in selling. As outlined in our post last week, offers received for royalty interests can be heavily dependent on operators and the uncertainty related to a change in operator.

Owners of mineral interests typically receive offers as multiples of average monthly revenue received. These multiples are typically determined by commodity prices, quality of operators, growth opportunities, and market sentiment. While owners of royalty interests do not have much control over these factors, they provide important starting points when considering selling.

We have assisted many clients with various valuation and cash flow questions regarding royalty interests. Contact Mercer Capital to discuss your needs in confidence and learn more about how we can help you succeed.

[1] Capital IQ