ExxonMobil made waves in the energy M&A markets by announcing its acquisition of Denbury, Inc. Exxon paid somewhere between Denbury’s stock price and a slight premium depending on the timing and stock price fluctuations. In total, the headline value was around $4.9 billion, according to Exxon’s news release.

However, while Denbury is an energy company on the whole, it is made up of two main segments that have very different economics. First, its carbon capture utilization and storage segment (CCUS). Second, its upstream enhanced oil recovery segment. These two businesses, in many ways, represent Denbury’s journey over the last several years that have one foot in the carbon future and one foot in the oily past. Neither of their business segments appears to be worth the $4.9 billion price tag. So what did Exxon buy exactly, and how might one value it?

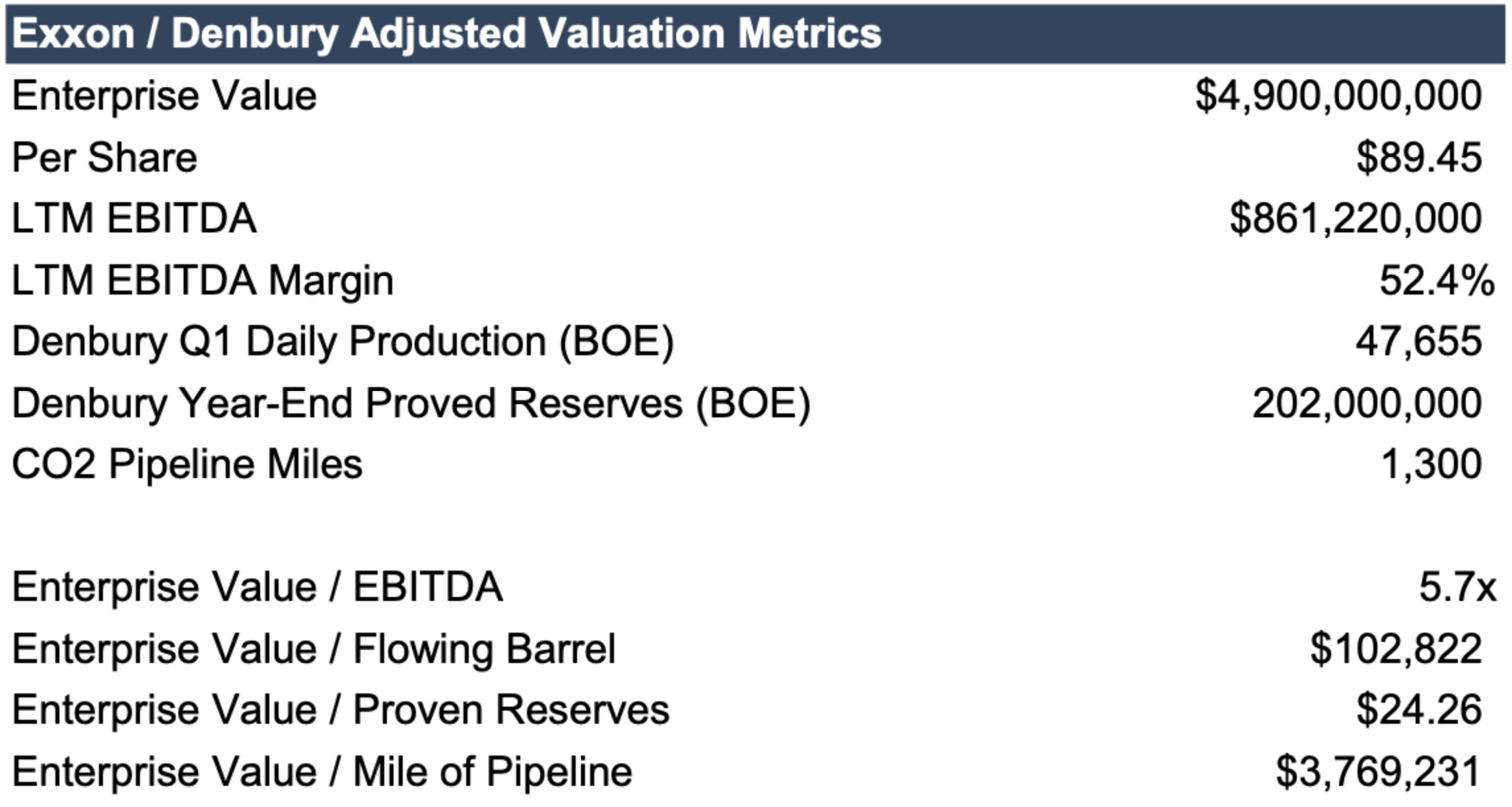

A quick look at some of the overall implied metrics related to the deal reveals some oddities compared to pure-play oil companies. As to CCUS transactions, there really have not been many to compare to, and certainly not at the scale that Denbury has achieved thus far. The table below was compiled based on figures from the announcement and Capital IQ data.

Just looking at the implied values relating to upstream multiples, the flowing barrel metric jumps out as high compared to most operators, especially with an EBITDA margin below 55%. This implies a higher multiple than much larger global companies such as BP, ConocoPhillips, and Occidental Petroleum—which does not make intuitive sense. On the other side of the equation, the value per mile of pipeline appears relatively high at first glance. This is considering management’s recent earnings call comments about construction costs being between $2 to $4 million per mile, coupled with the fact that the pipelines are not fully utilized yet. There clearly is a mix of segment-made contributions that drive different elements of the overall transaction price.

Just looking at the implied values relating to upstream multiples, the flowing barrel metric jumps out as high compared to most operators, especially with an EBITDA margin below 55%. This implies a higher multiple than much larger global companies such as BP, ConocoPhillips, and Occidental Petroleum—which does not make intuitive sense. On the other side of the equation, the value per mile of pipeline appears relatively high at first glance. This is considering management’s recent earnings call comments about construction costs being between $2 to $4 million per mile, coupled with the fact that the pipelines are not fully utilized yet. There clearly is a mix of segment-made contributions that drive different elements of the overall transaction price.

Denbury’s CCUS business represents the future of Denbury and embodies the key rationale for Exxon’s interest. Denbury has touted this segment, and most of its marketing, to investors centers on this aspect of its business. Its enthusiasm is apparent as its annual report spent almost all its focus on this area of the business. CCUS does represent a synergistic operational advantage for the company because Denbury has been one of the few upstream companies focusing on older, depleted fields that have lost what the industry calls “natural drive” and thus require incremental efforts to bring oil to the surface. Denbury’s solution to this challenge for a long time has been to inject its CO2 into the fields to create pressure and stimulate oil production.

However, the business model for a standalone CCUS business model is still relatively nascent, requiring hundreds of millions of dollars of investment and years before it could potentially reach cash flow sustainability separate from oil production activities. There’s already much in place now with 1,300 miles of pipeline and ten onshore sequestration sites, which was attractive to Exxon. However, things like the growth of offtake agreements, Section 45Q tax incentives (which I wrote about last year), and carbon storage contracts are not expected to generate net positive income for Denbury until several years in the future.

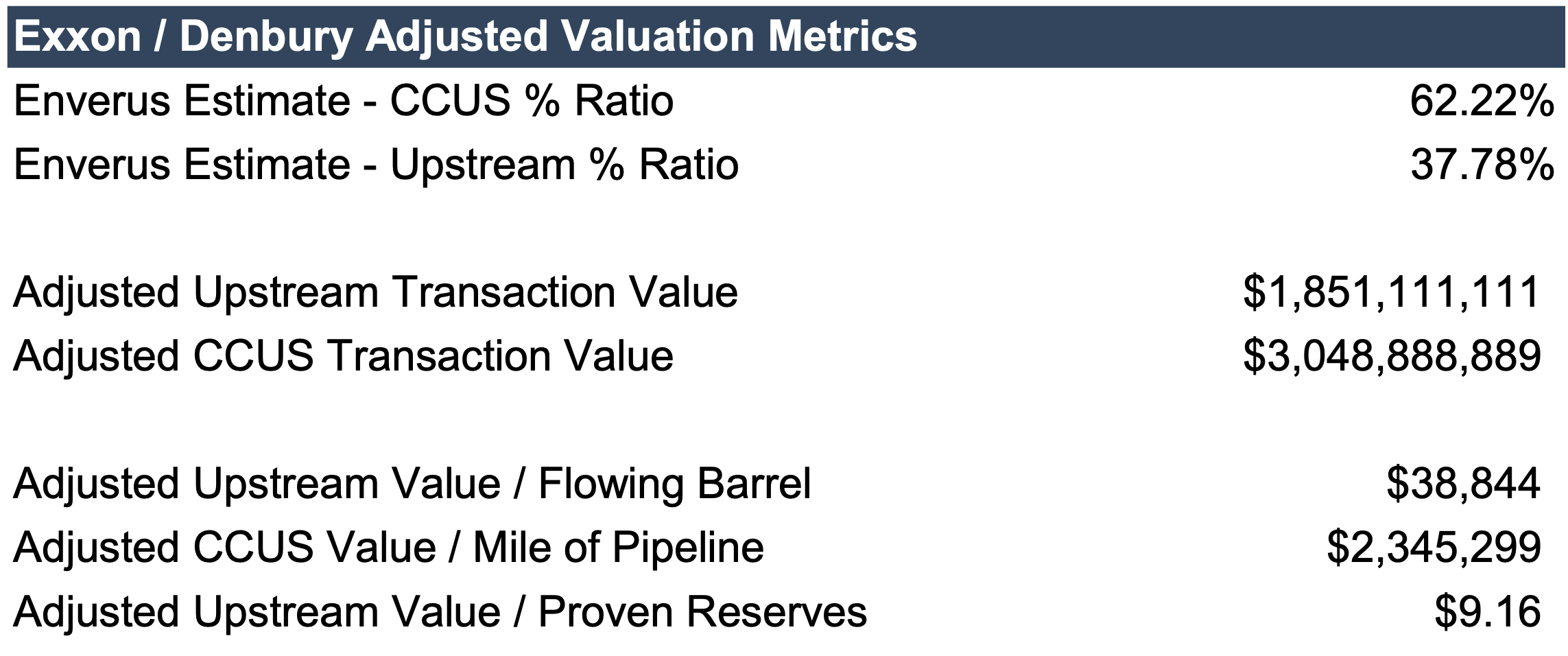

Nonetheless, this developmental potential and strategic location in the Gulf region have significantly contributed to Denbury’s stock price and Exxon’s interest. How much the CCUS is contributing to Denbury’s value is uncertain. But in an interesting article published a few days ago, Hart Energy interviewed Andrew Dittmar, a Director at Enverus, who estimated that (effectively) about 62% of Denbury’s value was based on their CCUS business. In the meantime, Denbury’s upstream enhanced oil recovery (EOR) business has been pulling the income statement’s performance along. Nearly all profits for Denbury are generated through this business line. However, compared to other public upstream companies, Denbury’s profitability is comparably lower, production is smaller, and production costs are higher. This is not a recipe for high comparative valuations, certainly not over $100 thousand per flowing barrel, which only the likes of Exxon and Chevron imply. (While we’re on the topic of segments, it is not a clean comparison either since Exxon and Chevron are two integrated companies with many segments that contribute to their values too).

Denbury is primarily a regional oil producer with less than 50 thousand barrels per day of production and EBITDA margins lower than many public oil companies. To its credit, Denbury does have lower decline rates than other companies due to the maturity of the fields they produce from. However, the flip side is that it costs $35-$39 per barrel to produce. Those are expensive lease operating costs when many companies operate somewhere in the teens per barrel. All that said, Enverus’s estimate in their Hart Energy interview was that the EOR business contributed about 38% of Denbury’s value. So, if Enverus’s analysis is to be applied here, that would put an adjusted value on Denbury’s production at around $39,000 per barrel and an adjusted value per pipeline mile of around $2.3 million. Take a look at these “adjusted” figures:

Under this scenario, Denbury’s upstream business would potentially be slotted in with public regional upstream producers with characteristics closer to: (i) under 200 thousand barrels per day of production and (ii) EBITDAX margins under 60%. Companies like Chord Energy (a Bakken-focused producer), Callon Petroleum (a smaller Permian operator), or maybe even Enerplus (another Bakken-focused producer) come to mind. Additionally, the value per mile of pipeline drifts down to the lower end of the construction estimate range, which also appears to be more realistic. Of course, this value depends on commodity expectations, regulatory stability, and execution of Denbury’s plan. Exxon appears to be optimistic about it. Whether or not Denbury’s shareholders will be remains to be seen.

Originally appeared on Forbes.com.