Key Takeaways

Whirlpool’s dividend suspension illustrates how dividend policy cannot be separated from operating performance, leverage, and reinvestment needs. Even a decades-long dividend history can become unsustainable when cash flow deteriorates and competing capital demands intensify.

Family business directors should evaluate dividends within a broader capital allocation framework that prioritizes long-term enterprise health alongside shareholder expectations. Maintaining distributions through rising leverage or deferred reinvestment can reduce financial flexibility and increase future risk.

Clear communication around dividend philosophy, financial thresholds, and tradeoffs is critical before conditions deteriorate. Shareholders are more likely to support difficult decisions when they understand how the board balances income needs, growth investments, debt obligations, and long-term value creation.

Whirlpool paid a dividend to investors for 70 years. Through recessions, inflationary periods, geopolitical shocks, housing cycles, and changes in consumer behavior, the quarterly dividend remained part of the company’s relationship with shareholders.

Until last week.

Whirlpool announced that it was suspending its dividend until further notice, citing the need to improve operating margins and continue reducing debt. The market’s reaction to the news was swift, with investors bidding Whirlpool shares down from near $55 per share to almost $40 per share (-27%). While the business fundamentals leading to the decision had been visible for several quarters, investors interpreted the dividend suspension as a negative signal about the company’s prospects for a near-term turnaround.

One lesson for family business directors is that no dividend policy exists apart from the financial performance and condition of the business. Dividends compete with interest, taxes, capital expenditures, and other capital needs to sustain the company’s growth. When operating performance deteriorates, dividends become subordinate to the survival and reinvestment needs of the enterprise.

A durable dividend policy is firmly and intentionally tethered to financial reality.

Expectations Change

We mentioned Whirlpool in passing in a 2022 post on recession, expectations, and value. At the time, Whirlpool was one of several public companies whose CFOs had been asked how their businesses might fare in an economic downturn. Whirlpool’s CFO expressed confidence that pandemic-related demand would continue to outpace constrained supply.

That was a reasonable expectation at the time. But expectations are not static. Since then, cash flow deteriorated, leverage became more constraining, shareholder pressure intensified, and reinvestment needs did not disappear.

Cash Flow: Dividends Compete with Everything Else

In many family businesses, dividends play an important role in shareholder relations. They provide income to family members who are not employed in the business. They can help maintain support for patient capital. They may be viewed as evidence that the business is performing well and that ownership has tangible benefits. But dividends are ultimately a residual claim on cash flow.

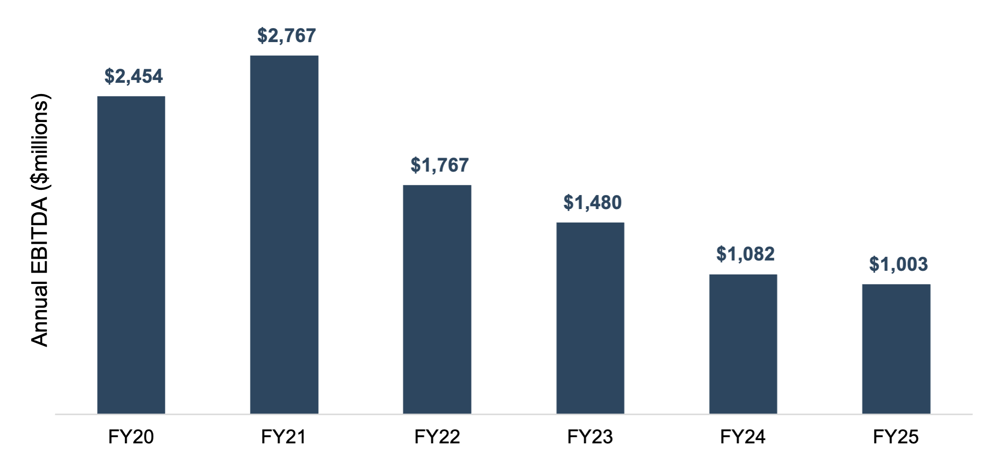

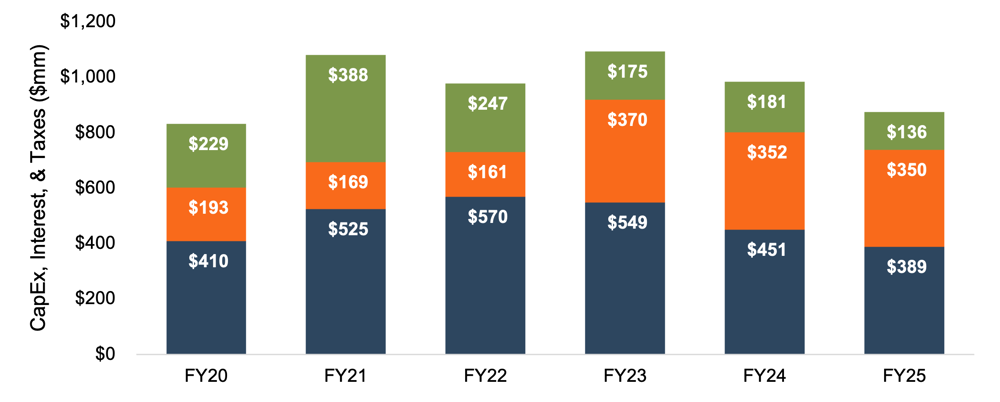

As shown below, Whirlpool’s cash flow (as proxied by EBITDA) had been declining for several years while the board elected to maintain dividends.

Meanwhile, capital spending required to sustain Whirlpool’s business was deferred to accommodate increased interest expense tied to debt incurred to finance ill-timed share repurchases in 2021.

As earnings fell, residual cash flow available for dividends, share repurchases, and other discretionary items fell from $1.6 billion in FY20 to $128 million in FY25, rendering Whirlpool’s $384 million annual dividend unsustainable.

Family businesses face the same brutal arithmetic. Cash flow must first fund working capital, taxes, capital expenditures, and debt service before supporting acquisitions, strategic investments, dividends, or share repurchases. When business conditions are favorable, those competing claims may be easy to manage. When margins compress or interest costs increase, dividend payments may be forced to take a back seat.

The board’s job is to decide where dividends fit in the hierarchy of capital allocation priorities. When conditions tighten, dividends should be evaluated in light of actual cash flow capacity rather than historical practice.

Risk & Return: Leverage Narrows the Board’s Choices

Dividend policy and capital structure are inseparable.

Earlier this year, Whirlpool announced plans to issue new shares to help reduce debt. The company had been downgraded below investment grade, raising its borrowing costs. The equity issuance was intended to strengthen the balance sheet, but public shareholders reacted negatively to the prospect of dilution.

David Tepper’s Appaloosa Management, a significant Whirlpool shareholder, criticized the company’s capital allocation decisions and argued that the equity issuance diluted existing shareholders at a high cost of capital. Whether one agrees with the criticism or not, the sequence is important: deteriorating cash flow and elevated leverage limited Whirlpool’s flexibility, and shareholders questioned the available remedies.

Family businesses usually do not experience that kind of public confrontation. There is no daily stock price announcing shareholder dissatisfaction. There may be no activist investor writing letters to the board. But the underlying tension is familiar.

Leverage can preserve ownership control and avoid dilution, but too much leverage can reduce financial flexibility. Issuing equity may strengthen the balance sheet, but it can dilute existing owners or alter control dynamics. Maintaining dividends can support shareholder relations, but doing so with borrowed money may increase risk. Suspending dividends can protect the enterprise, but it may disappoint shareholders who rely on current income.

There are no costless choices. For family business directors, the practical question is whether the dividend policy is consistent with the company’s risk profile. A business with modest leverage, stable margins, and limited reinvestment needs can support a different dividend policy than a business with cyclical earnings, rising debt service, and significant capital requirements.

The danger comes when shareholder expectations are calibrated to one risk profile while the business has migrated to another.

Growth: Reinvestment Still Has to Be Funded

Whirlpool has announced plans to spend $60 million on a new factory in Ohio to produce components and subassemblies for washers and dryers. At the same time, management is relying on price increases and tariff-related advantages to improve margins and restore financial performance.

Whether Whirlpool’s plan succeeds remains to be seen. But the capital allocation challenge is clear. The company needs to reduce debt, restore margins, invest in the business, and rebuild shareholder confidence. The dividend had to compete against all those priorities.

Family businesses often face a similar tension between current income and future competitiveness. A dividend that is easily funded in a mature, stable business may become more burdensome when the company needs to modernize facilities, expand capacity, invest in technology, make acquisitions, or withstand a cyclical downturn.

Directors have to balance the preferences of today’s shareholders with the needs of tomorrow’s enterprise. Some shareholders may prioritize current income. Others may prefer reinvestment to support long-term growth. Still others may be concerned about leverage, liquidity, or future ownership transitions. A thoughtful dividend policy provides a framework for balancing those competing objectives. Without that framework, dividend decisions can appear arbitrary: generous in good years, disappointing in bad years, and poorly understood in between.

The Best Time to Discuss Dividend Policy Is Before It Changes

Whirlpool’s public shareholders received a clear signal last week: the dividend is suspended until further notice. Family business shareholders may never receive news in such dramatic fashion, but dividend surprises can still be disruptive.

A reduction or suspension can raise difficult questions. Did management see this coming? Why was the dividend maintained so long? Is the business weaker than shareholders understood? Are family shareholders being asked to bear the cost of prior capital allocation decisions? When will distributions resume? What has to happen first?

Those questions are easier to answer if the board has already communicated how the dividend policy works.

For family businesses, good dividend communication does not require forecasting every downturn or committing to a fixed payout in all circumstances. It does require helping shareholders understand the principles that guide the board’s decisions. What level of cash flow is considered sustainable? How much leverage is appropriate? What reinvestment needs have priority? How does the board weigh shareholder income against long-term value creation?

In other words, shareholders should understand not only what the dividend is, but why it is what it is.

Questions for Family Business Directors

Whirlpool’s dividend suspension is a useful reminder that dividend policy should be revisited before circumstances force the issue. Directors might consider the following questions:

Is our dividend policy tied to sustainable cash flow or historical habit?

A long dividend history is valuable, but it is not a substitute for current analysis.What financial conditions would cause us to reduce or suspend the dividend?

If the answer is unclear in the boardroom, it will be even less clear to shareholders.Are we using debt capacity to preserve shareholder distributions?

Borrowing to fund dividends may be appropriate in limited circumstances, but it should not become a default practice.Are we underinvesting in the business to maintain the dividend?

Deferred reinvestment can make the dividend look more affordable than it really is.Do shareholders understand the tradeoffs?

Dividend policy is easier to support when shareholders understand the competing claims on capital.

Conclusion

Whirlpool’s dividend survived for 70 years, but it could not survive deteriorating cash flow and competing capital needs, providing a useful reminder that even long-standing capital allocation practices must remain tethered to financial reality.

Family businesses do not have to wait for a crisis to evaluate dividend policy. The better approach is to define the policy, explain the tradeoffs, and communicate the conditions under which the dividend could change.

No dividend is forever. But a well-designed dividend policy can help shareholders understand what the board is trying to accomplish, why the policy makes sense today, and how it may need to adapt tomorrow.