Key Takeaways

RIA M&A activity remains historically strong, but the market has become increasingly segmented. While transaction volume has held steady, a relatively small number of platform-scale acquisitions account for a disproportionate share of assets changing hands.

Premium valuations are becoming more selective. Buyers continue to reward firms with consistent organic growth, scalable infrastructure, institutional leadership, and differentiated service offerings rather than simply large asset bases.

Transaction structures are expanding beyond traditional acquisitions. Minority investments, recapitalizations, and other flexible ownership arrangements are giving RIA owners more strategic options to pursue liquidity, growth, and succession planning simultaneously.

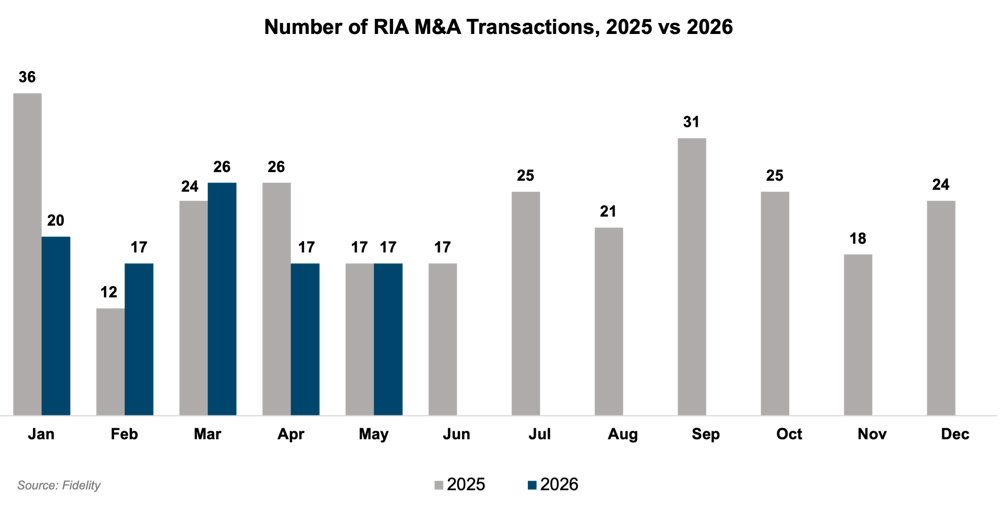

RIA M&A activity remained steady through May. Fidelity logged 97 announced wealth management transactions through the period, compared to 115 in 2025 and 87 in 2024. While 2026 is not running ahead of 2025, activity remains solidly above historical norms.

Although activity remains steady, the story has shifted. Rather than broad-based competition lifting all firms equally, the market is becoming increasingly segmented. Smaller tuck-in acquisitions continue at a steady pace, while a relatively small number of platform-scale transactions account for an outsized share of assets changing hands. Buyers remain active, but premium valuations are becoming more concentrated among firms with durable growth, leadership depth, and scalable infrastructure.

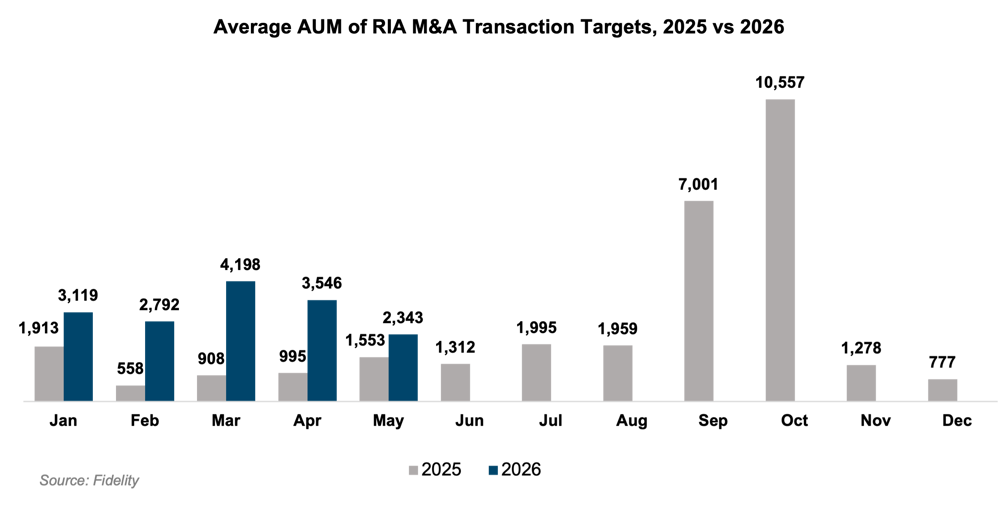

Monthly activity has also become more uneven. Fidelity reported 17 announced transactions in both April and May following 26 reported transactions in March. May deal volume totaled $39.8 billion in acquired assets, down meaningfully from April ($60.3 billion), as the market reverted closer to the historical median deal size after several very large transactions earlier in the quarter. RIA M&A has not slowed meaningfully, but aggregate AUM totals are increasingly driven by a handful of large platform transactions.

The largest deals announced since the beginning of April include LPL Financial and Private Advisor Group's acquisition of Mariner Advisor Network ($31.0 billion of AUM), Mesirow's acquisition of LeafHouse Financial Advisors ($24.1 billion of AUM), Wealthspire's acquisition of Sellwood Investment Partners ($11.0 billion of AUM), and Corient's acquisition of Capital Advisors ($7.8 billion of AUM). These transactions together accounted for 73.8% of April and May acquired assets.

Activity remains concentrated among repeat acquirers. Through May, Beacon Pointe had announced eight transactions, Savant seven, Cerity and Mercer Advisors five each, and CAPTRUST and Wealth Enhancement four each. The buyer universe remains broad, but transaction volume continues to be concentrated among the most active platforms.

A Two-Speed M&A Market

Fidelity's May data illustrates the shift. Approximately 70% of announced transactions involved RIAs with less than $1 billion in AUM, yet the relatively small number of larger transactions accounted for a disproportionate share of total assets changing hands. Meanwhile, aggregate deal value declined from April as transaction sizes returned to more typical historical levels rather than being driven by a handful of exceptionally large acquisitions.

This does not necessarily signal a slowdown in demand. Instead, it reflects a market that is increasingly operating on two tracks. On one end are smaller tuck-in acquisitions that allow established platforms to expand geographically, deepen advisor talent, or add complementary client relationships. On the other are larger strategic acquisitions that materially strengthen a buyer's capabilities, scale, or competitive position.

That distinction is becoming increasingly important from a valuation perspective. Premium pricing remains available, but it is not being applied uniformly across the market. Rather than rewarding size alone, buyers are increasingly differentiating between firms that simply add assets and those that enhance the long-term value of the platform.

RIAs that continue to command premium valuations generally share several characteristics:

Consistent organic growth, not just market-driven AUM expansion.

Institutional leadership that extends beyond a single founder, reducing key-person risk.

Scalable operating infrastructure, including technology, compliance, and repeatable processes.

Differentiated service offerings, particularly in tax planning, estate planning, retirement consulting, and family office services.

Strong client retention supported by recurring revenue and a demonstrated ability to integrate future growth.

As a result, valuation dispersion between average firms and exceptional firms appears to be widening.

At the same time, capital continues to be deployed through an increasingly diverse set of transaction structures. Traditional acquisitions remain common, but minority investments, equity recapitalizations, and structured partnerships are becoming more prevalent as firms seek capital for growth, technology investments, recruiting, and succession planning. As a result, today's market offers sellers considerably more flexibility than a simple decision to sell or remain independent.

One notable shift is that external transactions are increasingly viewed as a strategic growth decision rather than simply a succession solution. As transaction structures continue to evolve, firms can pursue liquidity, capital investment, succession planning, and continued ownership simultaneously. For many firms, the question is less about whether to sell and more about which ownership structure best supports the firm's long-term objectives.

Three Trends Worth Watching

A few themes continue to shape the direction of the RIA industry in 2026:

Platform acquisitions are becoming more strategic. Buyers increasingly seek capabilities instead of simply AUM, such as tax, estate planning, retirement consulting, UHNW services, and family office solutions.

Consolidation is concentrating among repeat buyers. Rather than dozens of equally attractive active buyers, a relatively small group of serial acquirers continues to account for much of announced activity, reflecting which buyers have both available capital and demonstrated integration capabilities.

Capital flexibility is becoming a competitive advantage. Today's sellers have more options than a binary sale-or-stay-independent decision. Many can now consider minority sales, phased exits, internal recapitalizations, or equity rollovers.

What Does This Mean for Your RIA?

For buyers: Competition remains strongest for firms that improve platform capabilities rather than simply adding assets. Buyers that can integrate effectively may find better opportunities among smaller firms where competition is less driven by headline AUM.

For internal succession: External M&A activity continues to influence internal valuations, but firms should resist benchmarking against exceptional platform transactions that may not reflect their own characteristics.

For sellers: The expanding range of buyer structures means sellers increasingly have flexibility to optimize for liquidity, continued ownership, succession, or growth. The best transaction is increasingly the one that aligns with long-term objectives rather than simply maximizing upfront proceeds.

About Mercer Capital

We are a valuation firm organized according to industry specialization. Our Investment Management Team provides valuation, transaction, litigation, and consulting services to a client base consisting of asset managers, wealth managers, independent trust companies, broker-dealers, private equity firms, alternative managers, and related investment consultancies.